Ever notice how most business owners can tell you exactly what they pay in rent, payroll, or inventory down to the penny, but if you ask them what happens to a credit card transaction after a customer taps their phone…they’re not so sure.

The thing is, merchant services are the invisible engine behind every sale, refund, and subscription. When it’s firing on all cylinders, nobody gives it a second thought (other than the merchant who knows a portion of that credit card sale will be paid back to the service that made that transaction possible). But if there’s any type of glitch in your payment processing system, your cash flow may stall, your accounting could become a nightmare, and worst of all, your customers experience an awkward friction that leaves a bad taste in their mouths.

It’s imperative to choose the right merchant services provider for your business. Adequate tools built into your services beyond transactions will give you:

- an integrated workflow

- quicker access to your money

- crystal-clear insights into your business

- reliable customer support

- and more.

Choose the wrong one, and you’ll find yourself nickel-and-dimed by hidden fees and trapped by rigid technology.

Let’s pull back the curtain on what merchant services actually are, how they work, and how to pick a partner that will actually help you grow.

What Exactly Are Merchant Services?

Simply put, merchant services is a catch-all term for the financial tools and tech that allow your business to accept and handle electronic payments.

People often mix up “merchant services” and “payment processing.” While they’re closely related, they aren’t quite the same thing:

- Payment processing is just the plumbing. It’s the literal movement of data and money between your customer, the banks, and the card networks.

- Merchant services are the whole house. It includes processing, but also covers your hardware terminals, online shopping carts (gateways), security software, data reporting, and recurring billing tools.

At its core, the whole system exists to do one job: get money out of your customer’s pocket and securely into your business bank account.

Why Merchant Services Matters More Than Ever

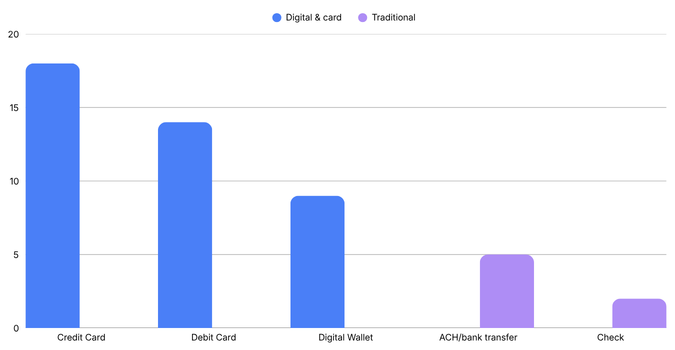

Let’s face it: cash is no longer king. According to the Federal Reserve Bank of Atlanta, credit card usage is climbing every year, with the average consumer making about 48 payments a month, many driven by increased credit card and mobile phone payments. If you aren’t set up to take plastic or digital wallets seamlessly, you’re leaving money on the table

The Main Ingredients of Merchant Services (What’s included)

If you sign up for a merchant services package, here is the toolkit you’re getting:

- Merchant Account: Think of this as a secure, temporary holding zone for your money after a customer pays. Once the transaction clears, the processor will send the funds to your actual business bank account. You’ll never really “see” this account, but it’s doing heavy lifting behind the scenes.

- Credit Card Processing: This is the tech that lets you accept debit, credit, EMV chips, and digital wallets like Apple Pay and Google Pay.

- Payment Gateways: If you sell online, you can’t plug a card reader into a website. Instead, you use a gateway. It acts as a secure digital bridge that encrypts your customer’s card info and protects you from fraud.

- Point-of-Sale (POS) Systems: Modern POS systems do way more than just ring up sales. They often act as the brain of your business. They track inventory, manage employee shifts, and keep tabs on customer data.

- Mobile Payment Solutions: If you’re a contractor, food truck owner, or mobile service provider, you need to get paid on the go. Mobile solutions turn your smartphone or a tiny wireless terminal into a fully functioning register.

How Merchant Services Works

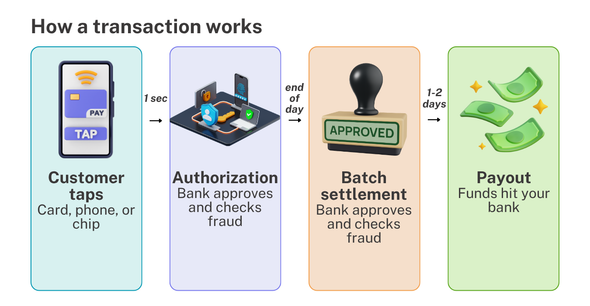

A transaction takes only a couple of seconds. But your money goes on a wild little journey:

- The Tap/Swipe: The customer dips or taps their chip card, taps their phone, or types their card details online.

- Authorization: The payment processor asks the customer’s bank, “Hey, does this person have the funds, and is this transaction legit?” The bank runs a quick fraud check and “clicks” “Approve.”

- The Batch (Settlement): At the end of the workday, your system bundles all your approved sales together and sends them off for payment.

- The Payout: The funds land in your bank account. Depending on your provider and setup, this usually takes anywhere from a few hours to a couple of days.

What Type of Businesses Need Merchant Services? (Spoiler: Almost Everyone)

Depending on what you sell, your merchant service needs will look a little different.

- Retailers: You need ultra-reliable counter terminals and a system that automatically connects your brick-and-mortar sales with your online store.

- Service Providers: If you’re a consultant or contractor, your bread and butter will be professional digital invoicing and mobile card readers.

- E-Commerce Shops: You live or die by your payment gateway. With online shopping hitting a staggering $326.7 billion in the first quarter of 2026 alone, having a smooth, secure checkout is a must.

- B2B Companies: Business-to-business sales usually mean massive invoices, commercial cards, or ACH (bank-to-bank) transfers, which require specialized processing to keep costs down.

- Healthcare & Pros: Doctors and lawyers need systems that aren’t just easy to use, but strictly compliant with privacy and industry regulations.

Demystifying Merchant Service Fees

As mentioned before, even when your payment system is working perfectly fine, you still notice your fees. So, it’s time to talk about the elephant in the room: cost. One of the biggest mistakes you can make is falling for a flashy, ultra-low headline rate without reading the fine print. Here is what you’re actually paying for:

- Transaction Fees: Every time a customer uses a card, a small cut goes to the card brand (Visa, Mastercard), a cut goes to the bank that issued the card (called interchange), and a cut goes to your processor.

- Monthly Service Fees: Some providers add flat monthly fees for platform access, reporting, or account maintenance.

- Equipment Costs: You can purchase your credit card terminals outright, or you can lease them. Word of advice: leasing often looks cheap upfront, but it usually ends up costing you way more in the long run.

- The Hidden “Gotchas”: Watch out for surprise PCI compliance fees, chargeback fees (when a customer disputes a charge), or nasty early termination penalties if you try to switch providers.

How to Choose a Merchant Services Partner

When shopping around for a provider, keep these five pillars in mind:

1. Demand Transparency

If a provider’s pricing structure looks like a riddle wrapped in a mystery, walk away. Confusion never works out in the merchant’s favor. Conversely, oversimplified pricing structures may seem nice, but the simplicity usually comes at a cost. In many cases, you will be overpaying for each transaction with a flat-rate structure.

2. Look for Software Integrations

One thing is for sure. Your payment system shouldn’t live on an island. It needs to talk to or integrate seamlessly with your accounting software (like QuickBooks), your CRM, and your inventory tools. Manually copying data from one system to another is a recipe for human error.

3. Test the Customer Support

When your payment system goes down on a busy Saturday afternoon, waiting until Monday morning for an email reply isn’t going to cut it. Make sure you can get a real human on the phone when things go sideways.

4. Don’t Skimp on Security

Data breaches are devastatingly expensive. The average global cost concerning business disruption, lost revenue, investigation costs, customer notification efforts, regulatory penalties, and post-breach recovery activities has skyrocketed to $4.4 million. It’s in your best interest to avoid this by all means possible. Ensure your provider includes top-tier encryption, tokenization, and PCI compliance tools right out of the box.

5. Plan for the Future

Pick a merchant services partner that can scale with you. Thinking about opening a second location, launching a subscription model, or selling online in the future? Your payment system should make that pivot easy.

Merchant Services Features That Deliver Long-Term Value

If you want to get real, long-term value out of your provider, look for these features:

- Automated Recurring Billing: Perfect for subscription models or retainer clients. It collects payments automatically so you don’t have to chase invoices.

- Smart Analytics: Good data tells a story. Your transaction reporting dashboard could show you your busiest sales hours, customer buying trends, and preferred payment methods.

- Omnichannel Flow: This lets customers buy online and return in-store seamlessly, keeping their experience consistent.

Why Modern Businesses Partner With ECS Payments

At the end of the day, business owners need to remove any unnecessary operational headaches. That’s what we at ECS Payments do best. We have designed our merchant services around what actually matters to business owners: completely transparent pricing, robust integrations, and support that actually picks up the phone.

Whether you need to link payments into your ERP system, set up automated recurring invoices, or outfit a mobile team with card readers, we focus on stripping away the friction so you can focus on running your business.

Final Thoughts

Merchant services shouldn’t just be an expense line on your P&L statement. When you dig deep, it is the foundation of your customer experience and cash flow.

When you’re ready to evaluate your options, look past the baseline rates. Look at the tech, the support, and how well it fits into your daily workflow. A great payment partner shouldn’t make your life more complicated. It should make your business run better.

Want to build a smoother foundation for your business? Let’s chat about how ECS Payments can tailor a solution for you.