A funny thing happened over the last few years. Customers stopped caring where the checkout counter was. They’ll pay at a food truck window, their driveway, at a trade show booth, beside a landscaping trailer, or from a server carrying a handheld terminal between restaurant tables. The expectation is simple: if they’re ready to buy, you should be ready to accept payment. Over the last few years, wireless credit card processing has become one of the most important shifts in payment technology for small and midsize businesses.

For many merchants, the question is no longer whether wireless payment processing makes sense. The question is how it works, what equipment is required, and whether it actually improves operations enough to justify the change. In many industries, it absolutely does.

What Is Wireless Credit Card Processing?

With wireless credit card processing options, businesses can accept card payments without being physically connected to a stationary wired payment terminal that relies on a dedicated phone line or fixed internet connection. Wireless transactions travel through Wi-Fi, cellular networks, or mobile devices.

The difference allows for location flexibility for businesses and payment flexibility for customers. The technology moves the point of payment closer to the customer.

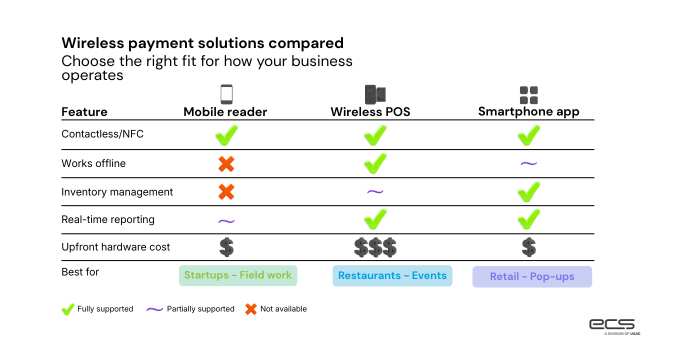

Types of Wireless Payment Solutions For Mobile Businesses

Businesses can take advantage of wireless payment solutions in a few different forms. The right choice just depends on how your business operates.

Mobile Card Readers: compact devices that connect to smartphones or tablets. Popular among startups, service providers, and businesses that need portability without significant hardware investment.

Wireless POS Terminals: Standalone credit card machines that do not need to be wired into the wall and communicate with the network via cellular or Bluetooth connectivity.

Smartphone and Tablet-Based Processing: Certain processors can connect your payment platform to an app right on your cell phone or tablet. The app also includes inventory management, customer data, and reporting.

Key Features of Wireless Credit Card Processing

Modern mobile payment terminals offer much more than mobility. Most business owners start looking at wireless credit card processing because they want the freedom to accept payments outside of a traditional checkout counter. What often surprises them is how much the technology improves day-to-day operations beyond simply taking payments on the go.

From connectivity and reporting to security and customer convenience, wireless payment systems are designed to keep transactions moving wherever business happens.

Connectivity Flexibility

Connectivity flexibility is one of the biggest reasons wireless payment processing has become so popular across industries. Traditional payment terminals are tied to a specific location. Wireless terminals are designed to move with the transaction. That sounds simple until you start thinking about how many businesses no longer operate from a single checkout counter.

- Contractors collect payment after completing service calls.

- Restaurant servers take payments tableside during busy dinner rushes.

- Retailers are running sidewalk sales.

- Food trucks serving hundreds of customers at a weekend festival.

Nothing gets a line of customers frustrated faster than when a payment system goes down. That’s why businesses prefer wireless terminals that support both Wi-Fi and cellular networks. If you’re struggling with a temporary internet outage, you can continue processing transactions through a cellular connection. And if you’re working in a location with poor cell reception, you can rely on Wi-Fi instead.

Contactless Payment Acceptance

Watch customers at a checkout line, and you’ll notice something interesting. Many already have their phone, smartwatch, or tap-enabled card ready before it’s their turn to pay. The Federal Reserve’s consumer payment research even shows ongoing growth in electronic and mobile payment behaviors.

As a result, modern wireless payment terminals typically include built-in NFC technology, allowing businesses to accept:

- Contactless credit and debit cards

- Apple Pay

- Google Pay

- Samsung Wallet

- Other digital wallet platforms

Transaction speed can affect revenue in particular settings. Think about a busy food truck with a line stretching down the block. Or a vendor at a sporting event who is trying to serve customers during a short intermission. Every extra second at checkout affects how many customers can be served before the rush ends. And that is where wireless terminals and tap-to-pay transactions help reduce any friction.

Real-Time Reporting and Transaction Management

Years ago, many business owners didn’t see sales numbers until they closed out the register at the end of the day. However, most modern systems provide access to transaction activity as it happens. Owners can review sales volume, transaction counts, refunds, and settlement activity from virtually anywhere.

That visibility becomes particularly valuable for businesses operating outside of a traditional storefront.

In having access to more data in real-time, business owners, operators, and staff can use that information while there’s still time to do something with it. Waiting until tomorrow to find out something went wrong rarely helps today’s revenue.

Security Features

Wired payment devices are stationary and connected through a controlled network. But wireless payments are mobile. As a result, payment data travels through Wi-Fi, cellular networks, or cloud-based systems.

{kind=link}

That mobility creates tremendous flexibility, but it also requires strong security protections behind the scenes. Most modern wireless payment solutions include:

- End-to-end encryption: which protects payment information while it moves between the payment terminal, processor, and banking networks.

- Tokenization: which replaces sensitive card information with unique digital identifiers that have no value if intercepted.

- PCI-compliant processing environments: which help ensure payment data is handled according to industry security standards.

- Secure cloud-based transaction storage: which allows businesses to access transaction information without storing sensitive cardholder data directly on local devices.

- EMV compliance: which replaced risky magstripe transactions with secure technology that creates unique transaction data that cannot be duplicated.

Benefits of Wireless Payment Processing

A wireless terminal can connect through cellular networks, accept tap-to-pay transactions, provide real-time reporting, and secure payment data through multiple layers of encryption. Those capabilities are important, but business owners don’t invest in payment technology because it has an impressive feature list. They invest because of what those features allow them to do.

Faster Customer Checkout Experiences

Wireless payment processing reduces long checkout lines, customers waiting for the bill, and back-and-forth communication prior to payment for service.

Consider a restaurant during a busy Friday evening. Traditionally, a server would deliver the check, walk away, wait for the customer to provide their card in the folder, collect the card, walk to a payment station, process the transaction, return with a receipt, and then wait for the customer to sign. That process repeats itself hundreds of times every week.

With a wireless payment terminal, the transaction can happen directly at the table. Customers pay when they’re ready, servers spend less time traveling across the restaurant, and tables become available more quickly for the next guests.

The same principle applies anywhere customers form lines, or service businesses come to the customer. Faster transactions create a smoother customer experience while allowing businesses to serve more people during peak periods.

Improved Payment Collection Flow

Wireless payment processing improves payment collection. For many service businesses, the work and the payment don’t always happen at the same time. Each additional step creates an opportunity for delay. When a technician can collect payment immediately using a mobile payment terminal, the transaction is completed while the service experience is still fresh in the customer’s mind.

There’s no invoice sitting unopened in an email inbox, no follow-up call next week, no wondering whether payment will arrive before month-end. The job is complete, and the payment is complete. For many businesses, that improvement alone can have a noticeable impact on cash flow.

Greater Flexibility for Employees

Wireless payment solutions also change how employees work. Traditional payment systems often force staff to return to a specific location every time a transaction needs to be processed. For example, a server making dozens of trips to a payment station every shift, or a sales associate leaving customers on the showroom floor to process a transaction, or an event vendor directing customers to a separate checkout area.

But wireless terminals allow employees to process transactions right where customer interactions are already happening.

Improved Cash Flow and Faster Access to Revenue

Wireless payment processing also helps accelerate the revenue cycle. It minimized the time between providing the service and collecting the payment. Instead of generating invoices and waiting days or weeks for payment, businesses can process transactions immediately upon completion.

Consistency makes financial planning easier. Payroll, inventory purchases, vendor payments, and operating expenses become more predictable when revenue is arriving on a regular schedule.

Better Customer Convenience

Wireless payment processing supports convenience and customer expectations by allowing businesses to accept payments where it is most convenient for the customer rather than where it is most convenient for the equipment. Sometimes that means paying at a restaurant table or completing a transaction at their front door. Sometimes it means checking out at a pop-up retail booth without standing in a long line.

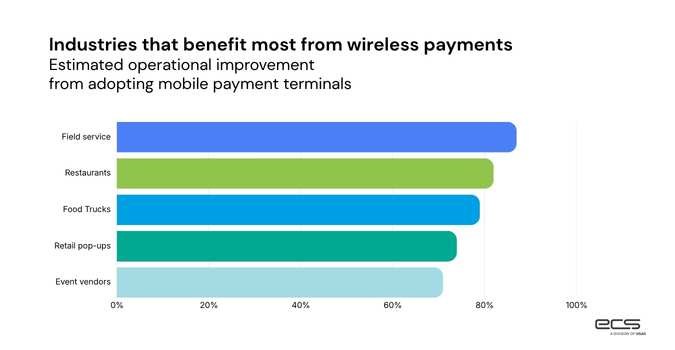

Industries That Benefit Most from Wireless Payment Solutions

Wireless credit card processing can improve operations for almost any business. However, the impact tends to be most noticeable in specific industries. Ones where employees, customers, or transactions are constantly moving.

Restaurants and Food Trucks

In many traditional restaurant environments, servers must walk back and forth between customer tables and a stationary terminal every time a guest is ready to pay. Those extra steps may seem minor, but they add up quickly during a busy lunch or dinner rush.

Wireless payment terminals bring payment directly to the table. Guests can insert, tap, or swipe their card without handing over their card and watching it leave their sight. So not only is the payment fast, but it also gives the diner more peace of mind that their sensitive payment details are not mishandled.

Retail Stores and Pop-Up Shops

Retail isn’t stuck inside storefronts. Wireless payment processing allows retail shops to have flexible checkout locations rather than a singular checkout counter. They can be extremely beneficial during seasonal rushes, outdoor sales events, and temporary checkout expansions, providing the same professional experience customers expect from larger retail operations.

Field Service Businesses

Ask any service business owner what they would rather do: collect payment at the end of a job or spend the next few weeks tracking down invoices. Wireless payment terminals allow field service technicians to complete the payment collection during their visit without creating additional accounts receivable.

Common Challenges With Wireless Payments (and How to Avoid Them)

Wireless credit card processing offers tremendous flexibility, but like any business technology, it comes with practical considerations. Most merchants rarely encounter major issues once a system is properly configured, but understanding potential challenges ahead of time can help prevent disruptions and protect the customer experience.

The good news is that most wireless payment processing problems are predictable, which means they’re usually preventable as well.

Connectivity Issues and Network Reliability

One of the most common concerns with wireless payment solutions is connectivity. Unlike traditional terminals that remain connected to a dedicated network, wireless credit card machines rely on Wi-Fi, cellular networks, or a combination of both.

In most cases, this works. However, businesses that function in remote locations, outdoor venues, rural communities, or heavily congested event spaces with thousands of mobile devices using the same cellular towers may occasionally encounter connectivity challenges.

You can reduce these risks by:

- Choosing terminals that support Wi-Fi and cellular connectivity

- Working with providers that offer multiple carrier options

- Maintaining backup payment procedures for rare outages

- Choosing select terminals that still process payments even when they are not connected to the network.

- For example, some Dejavoo devices process payments offline using a feature called Store and Forward (SnF) (or Offline Mode). Rather than verifying the transaction with the bank in real-time, the terminal locally caches encrypted card data and transaction details, then automatically pushes them for approval once the connection is restored.

Battery Management and Device Readiness

Because countertop terminals are plugged in all day, you never have to worry about a dead battery. But this isn’t the case with portable payment processing devices. Though there’s freedom in being disconnected, that freedom creates the additional responsibility of keeping equipment charged and ready for use. Charging stations, vehicle chargers, backup batteries, and spare terminals can help ensure transactions continue uninterrupted throughout the day.

Security and Compliance Responsibilities

Wireless payment processing permits the freedom to transact anywhere. But payment mobility should never come at the expense of security. Modern wireless payment solutions should include extensive protections such as encryption, tokenization, EMV chip support, and PCI-compliant processing environments. However, businesses still play an important role in maintaining a secure payment ecosystem.

- Install software updates promptly.

- Manage employee access carefully.

- Report lost or stolen devices immediately.

- Work with payment providers that prioritize ongoing compliance and security monitoring

How Wireless Payment Processing Supports Cost Efficiency

While processing rates matter, they don’t tell the complete cost story. Many of the biggest financial benefits of mobile credit card processing come from saved time, reduced administrative work, improved cash flow, and more overall efficiency.

Wireless Credit Card Processing vs Traditional Terminals

Traditional credit card terminals can be a reliable option for many businesses. Retail stores with fixed checkout counters, grocery stores, and other high-volume environments often use them successfully every day. The question for you is whether these are the best fit for how your specific business serves its customers.

Fixed Payment Locations Vs Mobile Payment Acceptance

The most obvious difference between traditional terminals and wireless payment solutions is mobility. A traditional terminal remains where it’s installed. Customers must come to the device when it’s time to pay. Wireless credit card processing reverses that relationship. The payment device travels to the customer instead.

That distinction becomes particularly important for businesses operating:

- In customers’ homes

- At outdoor events

- Across large facilities

- In restaurants

- At temporary retail locations

- On service routes

For these businesses, mobility creates opportunities that fixed terminals simply cannot provide.

Customer Experience Considerations

Customer expectations have evolved. They want fast payments, convenience, and they want to be able to use their mobile wallet. According to the Federal Reserve’s 2025 Diary of Consumer Payment Choice, credit card usage and mobile payment activity continue to rise as consumers increasingly embrace digital payment methods.

Wireless payment terminals support these expectations by allowing businesses to accept payments wherever interactions are taking place.

Scalability For Growing Businesses

As businesses grow, they may launch pop-up shops, add locations, expand their areas of service, and attend more events. Wireless payment processing helps with this scale without requiring merchants to rebuild their payment infrastructure each time the business evolves.

How to Choose the Right Wireless Payment Solution

Not all wireless payment solutions are equal. The right system depends heavily on how, where, and when your business accepts payments. Understanding your operational needs before evaluating equipment can help narrow the options significantly.

Evaluate Connectivity Options

Indoor businesses mostly rely on Wi-Fi, and mobile businesses, cellular connectivity. But, for greater reliability overall, the ideal setup would include both options.

Consider Software and System Integrations

Payment processing should not operate in isolation. The best wireless payment solutions integrate with existing business tools, including:

- Point-of-sale systems

- Accounting software

- Inventory management platforms

- Customer management systems

- Reporting tools

Prioritize Ease of Use

Cool features are great, and they can play a role in your business, but employees aren’t interested in learning a complicated payment system. They want to ring up a sale, collect a payment, and move on to the next customer. The more steps involved, the more opportunities there are for mistakes, delays, and frustrated customers.

Understand the Full Cost Structure

Beyond the cost of the hardware, evaluate the processing pricing structure, including:

- Processing rates (fee structure)

- Monthly fees

- Additional equipment costs

- Contract terms

- Equipment replacement policies

- Support availability (not related to fees, but included in what you pay for with your platform)

A lower upfront cost doesn’t always translate into lower long-term costs. Understanding the complete pricing structure helps businesses make more informed decisions.

Verify Security and Compliance Standards

Security is a priority regardless of your business’s size. Protect customers, reduce risk, and support the stability of your business long-term with payment solutions that support EMV technology, encryption, tokenization, and PCI compliance standards.

Final Thoughts

Checkout counters aren’t disappearing, but they no longer have to be the center of every transaction. For many businesses, wireless credit card processing is now the most practical way to take payments.

If you’re exploring wireless payment solutions, mobile payment terminals, or portable payment processing for your business, ECS Payments can help you find a solution that fits how you actually operate.