Estimated reading time: 12 minutes

A surprising number of businesses still run their payments like it’s 2009. Separate terminals. Separate reports. Employees manually matching receipts to POS data at closing time while everybody wants to go home.

The conversation around integrated payment terminals has shifted over the last few years. Payment systems have shifted from checkout tools to operational infrastructure. They directly affect reporting accuracy, labor efficiency, customer experience, PCI exposure, and how quickly a business can actually understand its own cash flow. Businesses and their customers are pushing for faster, more connected financial operations across channels and systems.

In fact, according to McKinsey’s Global Payments Report, digital payments continue to accelerate. In 2023, the global payments industry processed 3.4 trillion transactions. The report also estimates the payments sector could generate an additional $700 billion in revenue by 2028. This would be driven by digital payment adoption, instant payments, and expanding the modernization of payment infrastructure.

Still, plenty of merchants choose their payment setups based almost entirely on the upfront cost of the payment hardware. But 6 months later, when reconciliation starts to slow down, reporting shows gaps, or staff have to create workarounds because the systems don’t communicate properly, that decision can quickly feel inadequate.

A payment terminal setup either reduces friction or creates it all day long.

Before breaking down fully integrated, semi-integrated, and non-integrated payment terminals, watch this quick video on embracing integrated payments to see how connected payment systems can simplify checkout, improve reporting, and reduce manual work for your business.

What Is Payment Terminal Integration?

Payment terminal integration refers to how your payment hardware communicates with your POS system, accounting software, inventory tools, or broader business management platform.

At the simplest level, integration determines whether information flows automatically between systems or whether employees must manually bridge the gap.

With integrated payment processing systems, transaction data moves directly between the payment terminal and the POS software. Sales totals, refunds, taxes, reporting, and reconciliation update automatically.

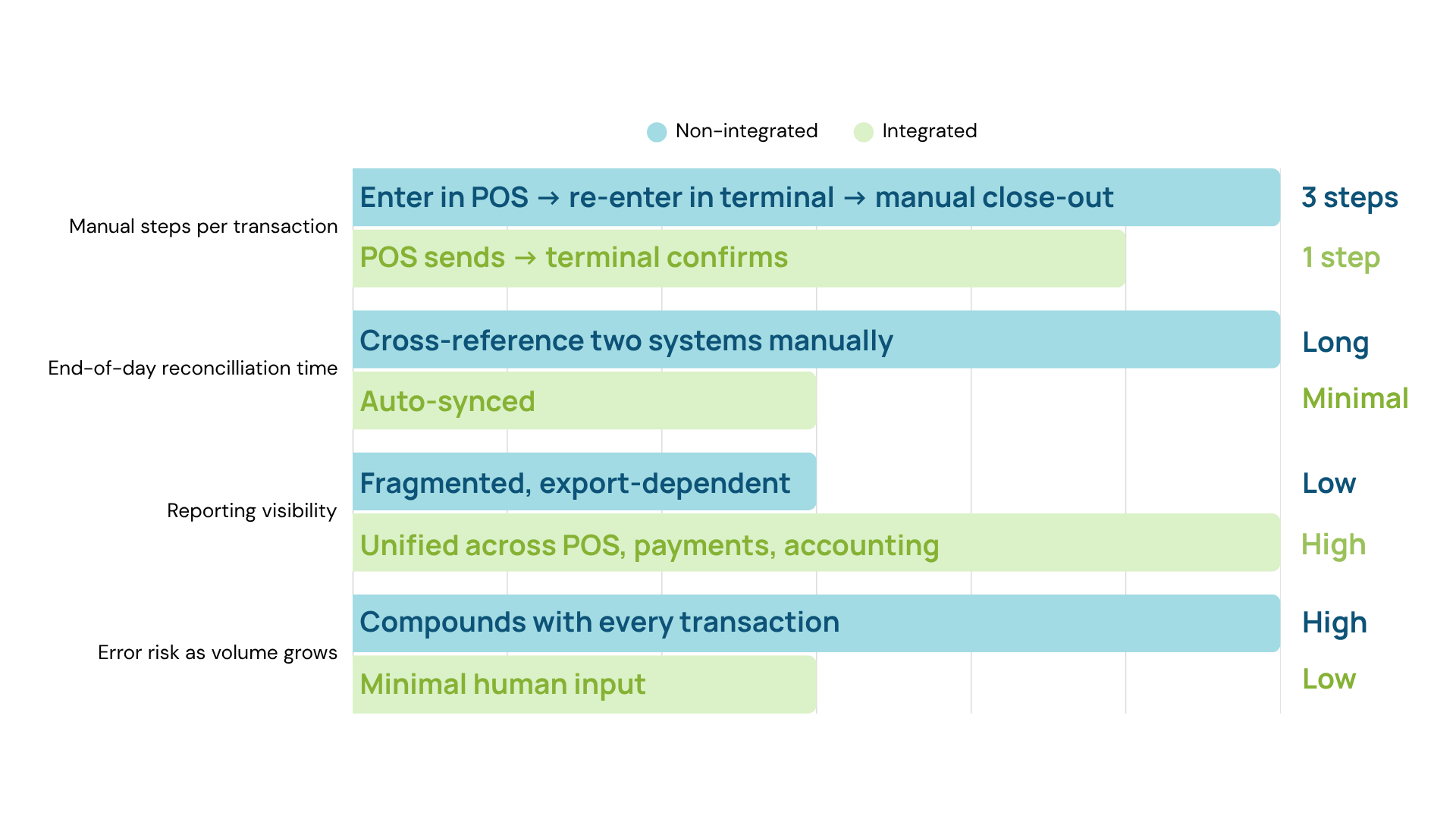

With non-integrated systems, the terminal and POS operate as separate islands. Someone enters the transaction into one system, then confirms it in another system. When transaction volume increases or staffing gets stretched thin, this becomes unnecessarily unmanageable.

POS payment integration is a great conversation to have for your business at all times but is even more necessary during labor shortages. Repetitive administrative tasks eat hours and payroll budget every week, and staff are paid to re-enter information that machines already have. Not a great use of time or money.

What Is a Fully Integrated Payment Terminal?

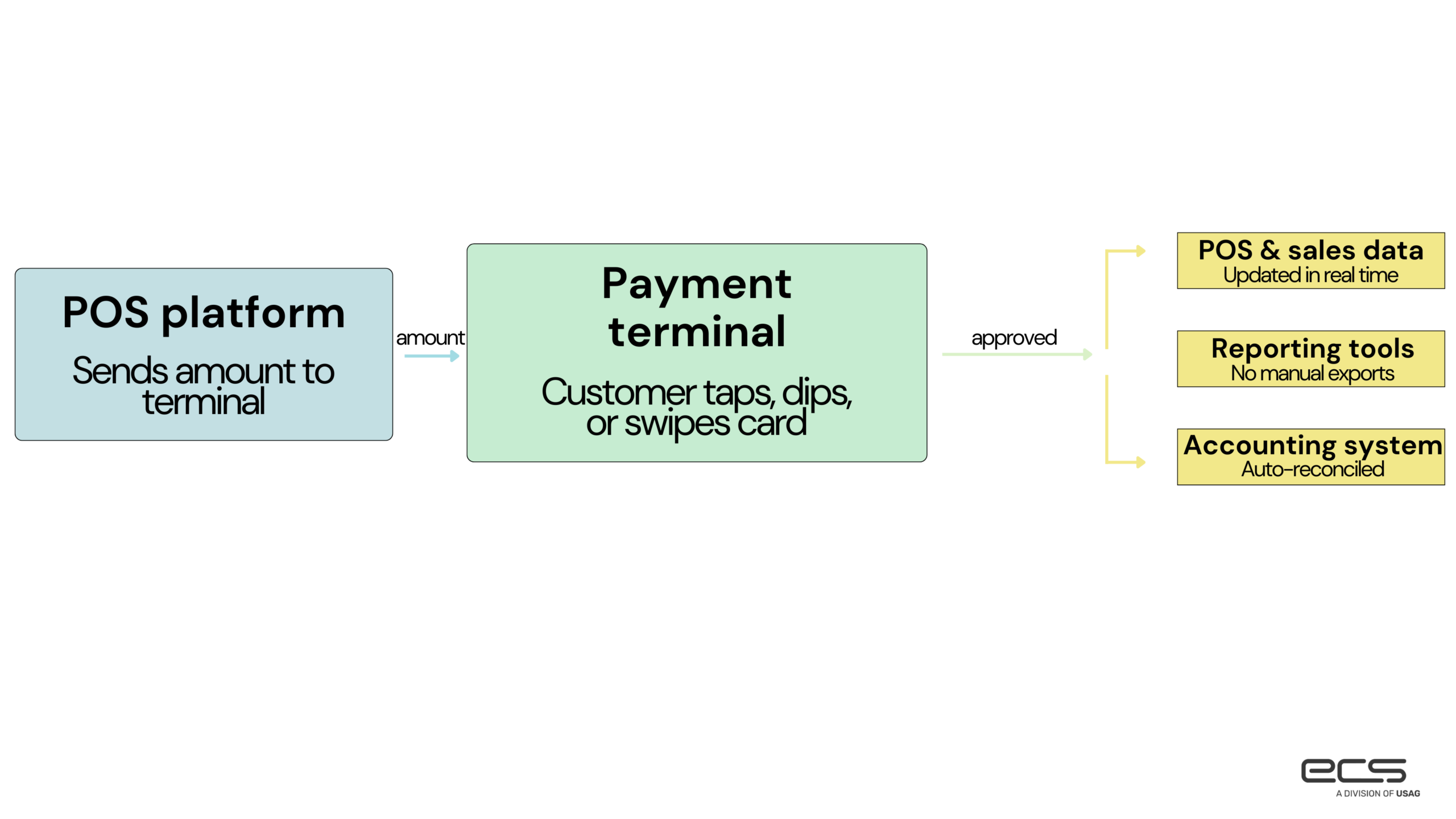

A fully integrated payment terminal integrations connects directly to the POS platform and automatically shares transaction data in real time.

When a customer checks out, the POS sends the payment amount directly to the terminal. Once the card is approved, the payment information flows back to the POS, reporting tools, and, often, accounting systems without manual intervention. It is a seamless process.

Restaurants, retail chains, medical offices, service businesses, and multi-location operations often lean toward fully integrated payment terminals. In these types of businesses, the complexity of their operations can compound quickly as transaction volume grows.

A busy restaurant is a good example. Servers close tabs, split payments, adjust tips, and move tables constantly. If the payment system operates separately from the POS, somebody eventually spends part of the night cleaning up mismatched tickets and incorrect totals. Usually management.

Integrated systems reduce a lot of that friction before it starts.

Benefits of Fully Integrated Payment Systems

Efficiency & Cost Savings

The biggest advantage of fully integrated payment systems is efficiency in your business workflow. Your employees will spend less time manually keying information. Your reporting becomes more accurate. And end-of-day reconciliation speeds up because systems now already share the same data. The savings alone, after calculating productivity vs. payroll hours over an entire year, are incredibly significant.

Performance Visibility

Integrated payment terminals help owners to gain better visibility into their business’s overall performance. Transaction data updates faster. Tracking and reporting no longer have to feel like an archaeological dig through spreadsheets, especially for multi-location operations.

Consistency & Connectivity

Businesses with integrated payment processing systems tend to have fewer “tribal knowledge” problems where only one longtime employee understands how closing procedures actually work. When turnover hits, this is a huge problem. But if everything is already synced, there’s less to worry about.

Security

Security concerns also push many businesses toward integrated payment environments. IBM’s 2025 Cost of a Data Breach Report found that the average cost of a data breach reached $4.4 million globally, which helps explain why businesses continue to prioritize and invest in automation and security improvements to reduce operational risk. Integrated systems reduce some exposure simply because fewer people manually handle payment data throughout the transaction process.

Potential Challenges with Integration

Full integration, as helpful as it is, does, however, require more upfront planning. Some businesses underestimate the true complexity of implementation. It can be especially cumbersome if they already use older POS systems, niche software, or custom workflows built over years of patchworking.

And honestly, some merchants discover their existing technology stack resembles a garage shelf full of incompatible chargers.

Integration projects work best when businesses first evaluate long-term operational goals rather than focusing solely on terminal hardware.

Because the hardware itself usually is not the real issue.

What Is a Semi-Integrated Payment Terminal?

Semi-integrated payment terminals sit somewhere between fully integrated systems and standalone terminals. The POS system communicates with the terminal to initiate payments, while sensitive cardholder data remains isolated within the payment device.

Semi-integration structure became increasingly popular because it balances operational efficiency with payment security requirements.

Especially for mid-sized merchants, semi-integrated payment terminals offer a more practical middle ground. The checkout experience still feels connected, but the security architecture reduces some of the PCI compliance complexity that a fully integrated system would have to address.

Benefits of Semi-Integrated Systems

Less PCI Burden

Of course, proper handling of sensitive data is of the utmost importance. But one major advantage is reduced PCI scope.

Since the payment terminal handles sensitive payment data separately, businesses may face fewer compliance burdens than in fully integrated environments, where payment data flows deeper into internal systems.

Simplification

Semi-integration can help businesses gain the benefits of POS terminals without rebuilding their entire infrastructure. For slowly growing companies or those operating with limited internal IT resources, this flexibility and simplification are beyond helpful.

Customer Experience

Lastly, semi-integrated systems improve your customer experience. Customers notice delays more than you may think. Compared to non-integrated environments, with semi-integrated ones, transactions move faster, employees spend less time toggling between systems, and checkout becomes more predictable.

Potential Limitations

Semi-integrated systems can still leave some gaps when it comes to reporting and automation. The systems communicate with each other to a point, but not everything updates as completely as it would with a fully integrated setup. Depending on the POS system and payment provider, some features may also feel limited.

As businesses grow and transaction volume increases, those limitations usually become more noticeable. Reporting gets more important, operations get busier, and businesses often realize their payment setup is no longer keeping up with how they actually operate. That happens pretty often. Businesses tend to grow faster than the systems they started with.

What Is a Non-Integrated Payment Terminal?

A non-integrated payment terminal works separately from the POS system. Employees enter the sale into the register or POS first, then type the payment amount into the card terminal manually as a separate step. Once the payment goes through, the two systems still do not share information automatically.

These environments still exist across smaller retailers, legacy businesses, seasonal operations, and some service industries. Usually, because “the current setup still works.” Which can be true right up until scaling becomes difficult.

Benefits of Non-Integrated Systems

The biggest advantage is simplicity. Standalone terminals generally require less setup, fewer integrations, and lower upfront implementation complexity. For very small businesses with low transaction volume, a non-integrated setup may remain operationally acceptable for a while. Especially if reporting needs are minimal.

Drawbacks of Non-Integrated Systems

Manual processes usually start creating problems little by little. Employees have to enter the same information more than once, closing out reports takes longer, and accuracy depends heavily on staff catching mistakes. The more manual work involved, the easier it becomes for errors to happen.

Non-integrated payment terminals also create weaker visibility across business operations. Pulling accurate sales insights often becomes harder because systems do not communicate directly.

Electronic payment activity continues to climb steadily among businesses and consumers in the United States. As transaction volume rises, disconnected systems become harder to justify operationally.

Integrated vs Semi-Integrated vs Non-Integrated: Key Differences

The biggest differences usually come down to automation, security, reporting visibility, and how well the system can grow with the business.

Fully integrated payment terminals offer the most automation because the payment system and POS work together closely. Reporting updates more smoothly, and employees spend less time handling things manually.

Semi-integrated systems still connect the payment terminal and POS, but with some limitations. They can help simplify PCI compliance while still improving workflow compared to standalone setups.

Non-integrated systems are usually simpler to set up in the beginning, but they often create more manual work over time since the systems do not automatically share information.

Businesses sometimes frame this discussion in terms of technology. It is really about operational design.

- How many repetitive tasks should employees perform manually every day?

- How much visibility does management need?

- How fast does the business expect to grow?

Those answers usually point toward the right system architecture pretty quickly.

How Payment Terminal Integration Supports Operational Efficiency

Payment terminal integration explained in plain language comes down to reducing unnecessary friction. Integrated systems reduce duplicate entry. They improve transaction accuracy. They shorten reconciliation time. And they create better reporting consistency across locations and departments. This all directly affects labor efficiency.

If a manager spends 30 fewer minutes fixing reports and balancing transactions every night, that adds up to a lot of saved time over the course of a year. And if a cashier can get customers through checkout even a few seconds faster during busy hours, lines move quicker, and the overall customer experience improves.

Small frictions compound. But, so do small efficiencies.

Integrated payment terminals also enhance the customer experience by making checkout smoother and more predictable. Customers rarely compliment payment infrastructure when it works well. They absolutely notice when it doesn’t.

Which Payment Terminal Setup Is Right for Your Business?

The right setup depends more on how your business runs than how big it is. A small shop with lighter sales volume might be fine with a standalone terminal for a while. A busy restaurant or multi-location business usually needs something more connected because there’s more reporting, more transactions, and less room for manual mistakes.

It helps to think about:

- how many payments you process

- how much reporting you rely on

- the software you already use

- whether the business is growing

- how much time employees spend fixing manual issues

A lot of businesses pick the cheapest setup upfront, then end up dealing with slower reporting, extra manual work, and operational headaches later.

Key Features to Look for in Integrated Payment Solutions

Compatibility

Your payment system should work smoothly with your POS and business software without employees needing extra steps or workarounds.

Real-Time Reporting

Faster access to sales and transaction data makes daily operations easier. Managers can spot issues more quickly and spend less time sorting through reports at the end of the day.

Security

Features like encryption and tokenization help protect payment data and reduce risk as fraud continues getting more sophisticated.

Omnichannel Flexibility

Businesses today often accept payments in-store, online, through mobile devices, and with contactless options. A good system keeps all of that connected in one place instead of scattering reporting across multiple platforms.

This is where ECS Payments fits naturally for a lot of businesses. Most companies looking at payment terminal integration are trying to simplify operations, improve visibility, and cut down on manual work. Reliable support and flexible integration options usually matter a lot more long-term than saving a little money upfront on hardware.

Common Mistakes Businesses Make When Choosing Payment Terminals

These mistakes may be common, but as you prepare, we hope you won’t fall into any of them on your efficiency journey.

Cost-Only Focus

The most common mistake is focusing exclusively on upfront costs.

A cheaper standalone terminal seems great on the surface. But it can create years of additional manual work, slower reporting, reconciliation headaches, and avoidable operational inefficiencies and unnecessary costs.

Underestimating Scalability

Another mistake is underestimating your business’s scalability needs. Don’t choose systems based on current transaction volume. Focus, instead, on your expected growth.

Infrastructure Over Compatibility

And some merchants choose payment infrastructure before fully evaluating compatibility with existing POS software. That creates integration limitations later that become expensive to unwind.

Final Thoughts

Choosing the right payment terminal integration strategy depends on how your business operates and whether a fully integrated, semi-integrated, or non-integrated setup best supports your workflow.

Some businesses need tighter reporting, faster workflows, and fewer manual tasks because they have high transaction volumes and operate quickly.

Others may care more about an easier setup or simpler systems for now. A smaller business with lower transaction volume can sometimes get away with a standalone setup for longer without major problems emerging immediately.

Still, payment systems affect a lot more than just the checkout process. They actually influence how accurate sales data stays, and if accuracy is an issue, how long employees spend reconciling transactions and fixing reports.

Lastly, your payment system also affects how smooth the customer experience feels, especially during busy periods. Those operational headaches usually start small. Then growth puts pressure on them. Businesses that invest in better payment workflows earlier spend less time working around their systems later.

Contact ECS Payments to start integrating the right payment tools for your business.