Interchange fee vs a flat fee, what’s best? What are other merchants’ choices? Why? These are all common questions when it comes to choosing the best payment processor for your business.

Payment processing is a difficult terrain to navigate. With so many players in the game, moving parts, payment platform options, and providers to choose from, it becomes, well, tricky! As a merchant, you want to be able to accept payments effortlessly, but not drain your bank account, and waste your time and materials to do so.

Payment Processing Pricing Dilemma

One of the most confusing parts is the pricing. There are a few different pricing structures out there. The question is, what is the best pricing model for your business? How do you know if the merchant service provider is offering you the best deal and if they are being transparent with the fees you will pay?

In this article, my goal is to walk you through all the common questions and misconceptions you may experience when selecting your pricing model along with your merchant service provider. I want you to walk away with the knowledge to make better-informed decisions on what is best for you and your company.

What are the Pricing Structures?

There are 3 common pricing structures a payment processing company can offer their merchants.

- Flat Rate

- Tiered

- Interchange Plus

Some providers like ECS offer all 3 payment options. Whereas other providers like Square or Stripe only offer the flat rate option. When more options are provided, merchants can choose which benefits them more.

This could be based on their priorities and individual preference. One pricing structure offers clarity, whereas one is typically less costly. The better option would be dependent on what a merchant values more.

We will now take a deep dive into these 3 structures and what value each can bring. Additionally, we will go over why more merchants are choosing to steer away from flat rate models and integrate interchange plus pricing into their businesses.

What are Interchange Fees?

Interchange is another way of saying exchange. Every time a transaction is made, an exchange of information occurs between merchants, banks, card brands, and the payment processor.

When this exchange occurs, a fee must be paid for the facilitation of this service. Essentially, an interchange rate is a handling fee the merchant will pay to cover the costs associated with the risks and facilitation of processing card transactions.

Who Establishes Interchange Fees?

The card brands such as Visa and Mastercard establish this fee. Then the issuing banks charge this fee to the acquiring bank or processor. As a result, it becomes the merchant’s responsibility to cover the fee for every card payment at their business.

With each transaction, a merchant is paying the cardholder’s issuing banks for the benefits of additional security features and real-time transaction authorization with each electronic purchase.

How Much is an Interchange Fee?

It is a common struggle to understand interchange fees. It simply boils down to the fact that there is no one set fee for interchange. The fee is a percentage of an individual transaction.

Each card brand determines its percentages. In fact, there are hundreds of different interchange fees out there. These rates fluctuate. They are specifically determined based on a multitude of individual factors such as:

- The issuing brand of the card (Visa, Mastercard, American Express, or Discover)

- The type of card level (travel rewards, privilege, gold, platinum, business, etc)

- The merchant’s industry (retail, restaurant, healthcare, etc)

- The transaction process (card-present vs card-not-present)

Interchange fees are listed online for public knowledge. If you are curious about what the listed fees are, each card brand has them posted on their website.

Can Interchange Fees Change?

Though negotiation with interchange fees is unachievable, card brands do change their rate from time to time. Typically, Mastercard and Visa will change their fees twice a year. They will post their announcement of these changes around April and October.

Your merchant service provider may inform you of these changes. In the case they do not, being aware of these possible fluctuations is recommended to avoid any confusion about your rates.

Are Credit and Debit Interchange Fees the Same?

No. Just as credit cards have their interchange fees, so does the debit network. Typically, debit interchange rates are lower than credit card rates.

If the Interchange Fee Changes With Each Transaction, Why Don’t My Rates Fluctuate?

The best way to comprehend interchange rates and how they factor into your statements is to think of them as the base layer. Interchange rates are non-negotiable. Your merchant service provider will charge them to you.

However, your provider will additionally need to charge other fees for their services and for additional costs that may add up when processing electronic payments. Additional fees may be assessed individually or bundled into one flat rate that includes interchange and processor fees.

We will explore these pricing structures and additional fees below.

Additional Payment Processing Fees

In addition to the interchange fee, there are additional fees a merchant will need to pay to cover the cost of their card processing services. The following are the most common fees associated with credit card processing. They may or may not apply to you:

Transaction Fee

This fee is charged for every swipe, dip, tap, or keyed-in transaction. When an authorization message is sent to the bank, regardless of the card’s approval or decline, the fee will still apply.

Because this fee even applies to declined transactions, it can also be referred to as an authorization fee. This fee can range between 10¢ – 30¢ and would all be dependent on your account provider.

Chargeback & Retrieval Fees

All cardholders have the right to dispute any transaction with their bank. If there is a dispute the processor will send a fax, email, or letter to inform the merchant. A merchant has the opportunity to send a rebuttal for the dispute to prove the authenticity of the transaction with receipts and a written response.

Whether a merchant decides to fight the dispute or not, the banks still charge fees to the merchant to handle the cardholder’s dispute. This fee can range from $15 – $25 per dispute.

Additionally, if the merchant were to win the chargeback and the cardholder is unwilling to accept this, they may file a second chargeback for the same transaction. In this case, it would be elevated to a pre-arbitration.

Certain networks will allow the merchant to rebuttal a second time. Some will call it an automatic loss on the merchant’s end. In either case, the pre-arbitration fees can vary between $50 to $150.

This may be more than the original transaction amount. The merchant would then need to decide if it is financially worth it to them to move forward with the pre-arbitration or not when considering the hefty fee.

Voice Authorization Fee

A voice authorization fee is rare. This would only apply in instances when a terminal is down and cannot process transactions. However, they can call the processors toll free phone number and enter their customer’s card information to receive authorization for the transaction. This fee will range between 65¢ – 95¢.

Debit Fees

The debit network does tack on an additional 20¢ fee to process PIN-based transactions. Additionally, merchants may need to pay $5 – $10 every month to access the debit network.

Wireless Fees

An ever-increasing terminal option is wireless. This gives merchants the flexibility to process in-person transactions from anywhere. Wireless terminals must be connected to a cellular or wireless (Wi-Fi) network through a company such as Verizon, AT&T, etc. Monthly fees associated with wireless terminal connection will range from $10 – $25.

Additionally, wireless fees may apply per transaction. These can be anywhere from 5¢ – 15¢. And finally, merchant service providers sometimes require a $40 – $60 setup fee.

Terminal Lease Fees

Many processors offer terminal leases to their merchants. So rather than purchasing a terminal in full upfront, merchants can choose to lease their equipment and pay in smaller increments over a longer period of time. If you decide to lease your payment equipment, you will see additional charges to your merchant account. Additionally, it would be best if you can find leases with interest-free installments.

Application Subscriptions

If a merchant opts to use a POS system like Clover, they may choose to use some of their applications to help with business workflow. When utilizing these additional services, merchants will have an additional subscription payment tacked onto their statement fees. Having proper subscription management and knowing what applications are used will limit paying unnecessary fees each month.

Monthly Fee

In many cases, merchants will need to pay a monthly statement fee. This fee is between $10-$15 each month. Regardless of whether a merchant processes or not, this fee would still apply. Your merchant service provider charges this fee to maintain your account, supply you with detailed statements and offer customer support.

Monthly Minimum

A monthly minimum fee is an additional charge a merchant may have to pay if they did not process their set minimum. Some account representatives may set a merchant account up with a minimum to meet a standard to afford to provide their services.

For example, if a merchant account has a minimum fee of $20 and the merchant only processed enough to charge $15, an additional monthly minimum fee of $5 applies.

Batch Fee

Though rare, some processors may charge a batch or ACH fee, ranging from 5¢ – 25¢. This occurs every time the acquiring bank settles funds into the merchant’s account.

Card Brand and Network Association Fees

Merchants who process debit and credit cards must pay association fees to the card brands and debit networks to remain eligible. These fees are annual participation fees or card brand fees. They vary by the network but may show up on a merchant’s month-end statement.

Discount Rate

Payment processors/acquiring banks charge merchants a discount rate per transaction. It includes the majority of their fees including their interchange rate, and additional transaction fees which may include any of the above-mentioned fees.

Discount rates will vary based on the level of risk associated with each merchant. The higher risk they are, the higher the discount rate will be, and vice versa.

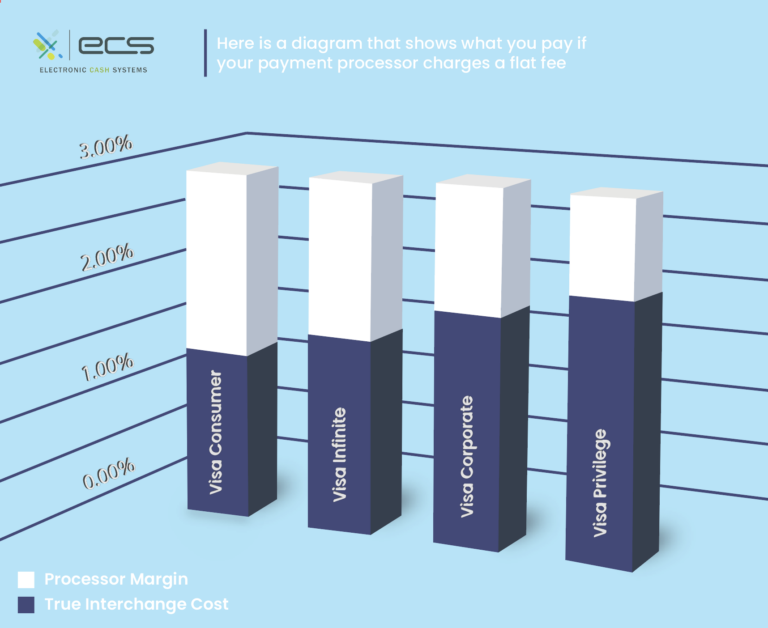

What is Flat Rate Pricing?

Flat rate pricing is a newly popular card processing price structure in recent years due to its cloyingly simplistic approach.

Unlike interchange plus pricing, which we will discuss later, transaction rates are not dependent on card-specific interchange rates. Conversely, flat rate pricing means that the payment processor charges one flat rate for all credit card transactions, regardless of the fluctuating interchange rate. This means, the type of card used for payment (gold, travel rewards, business, bottom level), won’t impact the cost to process the transaction.

Payment providers add interchange fees, the card brand fee, and the processor’s margin fee to determine one single rate that will be applied to all transactions that a business processes.

However, card-present and card-not-present transactions can have different flat rates. Consequently, this means a card-not-present transaction (keyed into a payment gateway or POS system) has a higher flat rate than present cards (tapped, dipped, swiped). The reason is, non-present transactions carry a higher risk for fraud.

What is the Flat Rate Fee?

The typical cost of flat rate pricing is around 2 to 3% of each transaction plus a few cents. This transaction fee usually hovers around 10¢.

What are the Flat Rate Pricing Benefits?

Merchants find it appealing to know exactly what to expect for their processing fees. Because the cost is always the same, merchants find this pricing structure the easiest one to handle when it comes to accounting purposes and predictability in monthly expenditures.

What are the Flat Rate Pricing Downfalls?

However simplistic the design of flat rate pricing is, there is a downfall to it. The lure of simplicity can distract merchants from realizing there are alternative pricing structures that may offer lower transaction costs. With flat rate pricing, a merchant will not know what their payment processor’s markup is on top of the set interchange fee. This means merchants remain in the dark about the actual fees that they are paying.

Additionally, flat rate pricing does not offer the benefit of lower interchange fees for cards that qualify for lower rates. So though the cards used to process transactions change and thus the card brand interchange rate will fluctuate higher and lower, the merchant does not reap the benefit.

Because the payment model the merchant has opted for remains the same regardless of the card used.

What Type of Merchants Benefit From Flat Fee Processing?

Flat rate pricing with its set percent plus transaction fee (For example 3% + 20¢), can best benefit merchants who are face-to-face with their customers and sell a low volume of tickets. However, when a business grows and begins processing more tickets or processes a lot of online or over-the-phone transactions, a flat rate begins to cost a merchant more in processing fees. The more transactions that occur, the more transaction fees you will pay.

Conversely, online businesses, in-person businesses that use online payment systems, or businesses with high ticket volume would not reap the same benefits. These types of merchants could be any eCommerce merchants or merchants who offer subscription payment services through web credit card processing.

Recurring payments or card-not-present transactions always carry a higher risk for fraud or chargebacks. Thus, processors and banks will need to charge more to cover themselves and the additional security measures.

If you are using flat rate processing for your business and you begin to see the above situations beginning, it is recommended to do some price comparison shopping on your payment provider to make sure you are getting the best bang for your buck.

Flat Rate Summary

While this pricing model may be the easiest to understand, it doesn’t necessarily mean it saves you the most money. Yes, the rate you pay will not have any fluctuations, but in many cases, because of the lack of variance, it could mean that flat rate pricing costs more than other payment models.

When it comes to your decision of choosing to go with a flat rate, you will need to consider how your business will function. How will you be accepting payments? How many transactions will you process on average per month? What is the average dollar amount for each transaction?

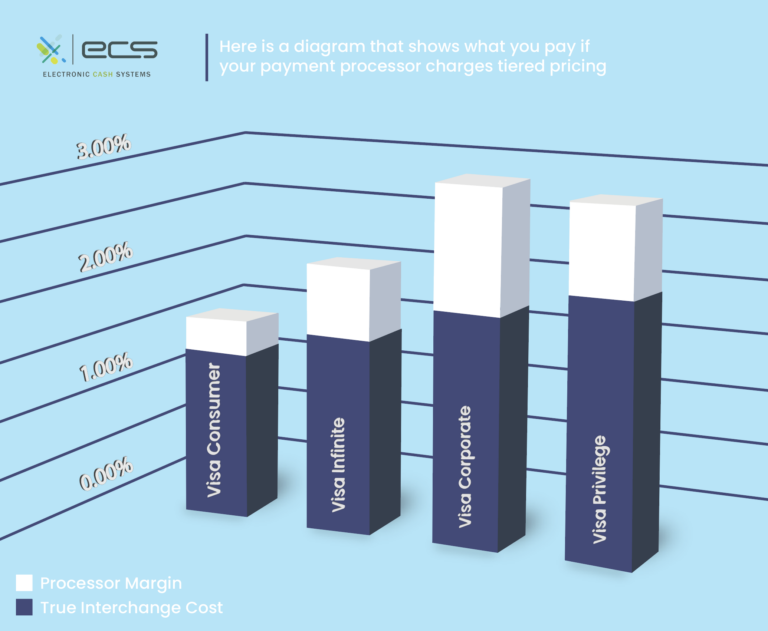

What is Tiered Pricing?

Surprisingly, tiered pricing is the most common pricing structure in the US. Tiered pricing utilizes the interchange rate of the card plus a qualification status as the payment processor’s margin. There are 4 categories in which transactions qualify.

- Qualified

- Rewards

- Mid-Qualified

- Transactions

- Non-Qualified Transactions

The factors that indicate a transaction’s qualification would be dependent on:

- The location of the point-of-sale

- Card-present (swiped, dipped, or tapped using Google Pay or Apple Pay)

- Card-not-present (keyed in)

- The level of the card (rewards, business, international, etc).

- The card network (credit or debit)

- The captured cardholder data (name, address, tax ID, tax amount, unit description, etc)

- The length of time between the card’s authorization and the settlement of the batch. Prolonged batch out can create a higher risk of chargeback liability as a cardholder may not recognize a purchase on a later date.

We will explore the difference between each category below.

Qualified Transactions

Qualified transactions meet all criteria to have the lowest discount rate possible. Qualified transactions carry the least amount of risk. The reason is that every qualified transaction occurs in person, either dipped, swiped, or tapped on a merchant’s card reader.

This, however, does not mean that all card-present transactions will meet the qualifications for the lowest rate. Other determinants like settlement speed and card type play a role in the transaction category.

Rewards

Rewards cards are any credit cards that offer rewards to the cardholder such as airline miles, hotel points, department store savings, cashback, etc. Reward cards used to be in the Mid-Qualified rate category, however, they have recently gained a category of their own right under-qualified. They offer the second lowest transaction rate.

Mid-Qualified Transactions

Transactions fall into the mid-qualified category if a merchant keys in a transaction rather than uses their card-present capabilities if they have been categorized as an in-person business. Additionally, transactions that are not batched out within 24 hours of the sale are mid-qualified transactions.

Non-Qualified Transactions

Non-qualified transactions carry the most expensive fees. This is because they also carry the highest level of risk involved. Such transactions would include:

- Keyed transactions that don’t use the AVS (Address Verification System).

- Corporate cards- as they demand more detailed reporting.

- Foreign cards -as they have additional Interchange fees for their need to convert currency..

- Transactions batched out after 48 hours of the sale

What are the Tiered Pricing Benefits and Drawbacks?

Although tired pricing is not a flat rate, it does offer the same sense of straightforward pricing. When a merchant opts to use a tired pricing payment structure they will have the benefit of lower interchange rates, but depending on other factors like settlement time and card-present vs not-present, the transaction may become more costly to the merchant.

Tiered pricing draws many merchants in because of the qualified low rates. However, a majority of a merchant’s transactions will end up in higher categories such as rewards, mid and non-qualified.

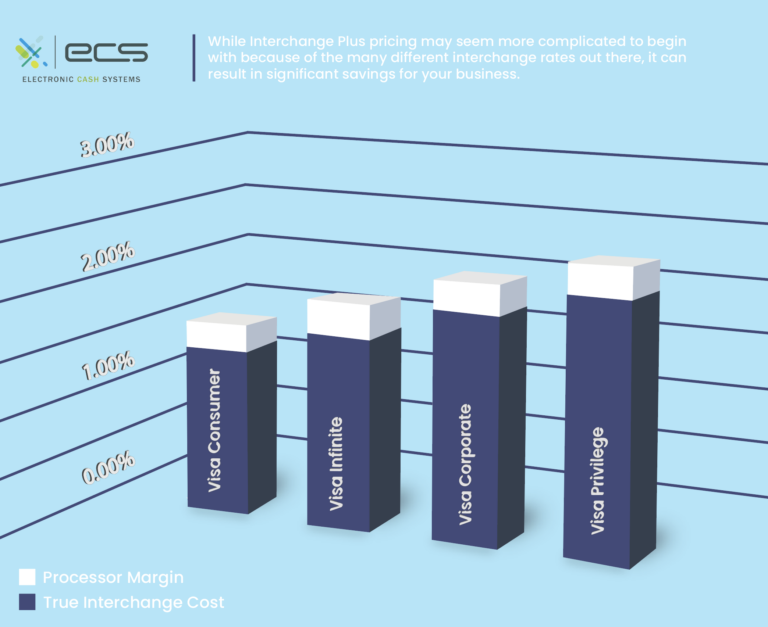

What is Interchange Plus Pricing?

As opposed to flat rate and tiered pricing, interchange plus (interchange passthrough) pricing can be a bit more taxing to comprehend. Though it will be more difficult to predict processing fees for the month, it is most likely that a merchant would be saving money.

With interchange plus pricing, a merchant gets to take advantage of the fluctuating interchange rates and lower fees on certain cards. The processor simply “passes through” the exact rate from the issuer to the merchant.

Then, the processor sets an exact discount rate where they have estimated the merchant’s costs associated with risk plus a singular set transaction fee.

With this design, the processor’s margin from the transaction remains the same every time. Meanwhile, the interchange fluctuates, giving the merchant the best deal depending on the card used by their customer.

Additionally, month-end statements will provide very detailed reporting on each fee a merchant is paying. As a result, the interchange plus pricing model easily creates the most honest and transparent relationship between a processor and their merchant.

Interchange Fee Flexibility: Flat Rate Vs Interchange Passthrough

With Interchange Pass through, though the processor’s margin remains the same, the interchange rate will fluctuate for every transaction. Because of this, it makes it difficult for merchants to know the exact processing fees they will be paying for the month.

Although interchange is more intricate and therefore more difficult to comprehend, it is likely the most cost-efficient option. Compared to flat rate pricing, merchants save on interchange plus when transactions are eligible for lower rates based on a less expensive card to process.

Conversely, if a cardholder were to pay with a more expensive card that has a higher interchange rate, the merchant may be paying more interchange fees than they might with a flat rate model. However, this does not necessarily mean that the total transaction cost would be higher than a flat rate.

This would all depend on where the processor’s margin sits. And because merchants are provided with a detailed month-end statement, they can see exactly what the processor is charging them and why. Unlike flat rate pricing, where a merchant would never know what the fees covered. Clearly outlined statements, as a result, produce breezy reconciliation and accounting.

What are the Benefits of Interchange Plus Pricing?

As listed above, there are quite a few benefits to interchange pass-through pricing. We have re-outlined them below for a sufficient understanding of the benefits of this pricing structure.

No Overpaying for Lower Priced Transactions

Because interchange rates fluctuate, there are opportunities to save more with less expensive interchange rates on certain card transactions. The flat rate pricing structure never allows you to see these fluctuations or reap the benefits of lower interchange rates. Conversely, with interchange pass-through, you will pay exactly what the rate is per the card brand.

Interchange Passthrough is Transparent

Interchange passthrough provides merchants with physical or online payment statements that break down every transaction and cost associated to process that card. Additionally, a merchant’s application contains a line item with the exact cost for every applicable fee. So there are no hidden fees.

Additional Savings with More Processing

Many credit card processors who offer interchange plus pricing, offer volume discounts. This means that as businesses grow and process more payments, there are higher discounts. So the higher the volume of tickets, the lower the merchant fees will be.

Automatic Benefits from Card Brands Interchange Rate Changes

Every so often the card brands will update their interchange rates. When these rates lower from time to time, merchants on interchange plus plans will automatically reap the rewards of lowered rates.

What are the Downfalls of Interchange Plus Pricing?

In all honesty, the only downside to interchange plus pricing would be the lack of consistency. Because of this, merchants will have a difficult time knowing exactly what fees will be taken out for each transaction. But if not knowing what you will pay, even though what you are paying will most likely be less than you would with a flat rate, I’d say it’s a pretty good trade-off.

Why Merchants Are Choosing Interchange Plus Over Flat Rate

Even though tiered pricing is currently the most popular and flat rate has been a shiny new payment model, many merchants are starting to choose interchange plus over these other systems.

Though it may still seem like a tricky choice, there is a silver lining that may push merchants all the way towards interchange plus. And that would be because the majority of cards processed qualify for a low interchange fee.

What this means is most consumers are not making purchases with a privilege, business rewards, or an Amex black card. Most consumers carry plain Jane, low-limit credit or debit cards.

In the flat rate pricing model, a merchant’s rates never change. However, because the interchange rate does, the processor’s margin of profit will fluctuate up and down. But the merchant’s fees will remain constant. So this design benefits the credit card processor in making more money off a merchant’s less costly transactions.

Interchange plus models are the opposite. The credit card processor’s margin will remain constant. Never changing based on the interchange rate.

However, a merchant’s rate will. This means they have the advantage of lower fees with lower rate cards, but also they have higher fees with higher rate credit cards.

The advantage of this model is even though they will pay higher rates on occasion, is it more uncommon than the lower rates. Additionally, all fees are clearly outlined for the merchant to see what they are paying.

Interchange Fee vs Flat Fee Conclusion

The reality is unfortunately that credit card processing will never be simple. However, that doesn’t mean business owners need to be in the dark about where their choices lie and where they can potentially save money with their payment platform.

Sadly, to keep profits up, some credit card processors rely on confusion to keep merchants overpaying. What you need to know is that essentially, there are three components that when combined, comprise your total fee. This includes:

- Interchange Rate: The fee charged by issuing banks to process the transaction. This varies by card brand, type, and payment method.

- Card Brand Fee: A fee charged by the card brand used (Visa, Mastercard, Amex, Discover) for each transaction.

- Payment Processor Margin: The fee the payment processor charges for providing their services to be able to accept card payments.

With any payment model you choose, you will still be paying for all three fees. It is really a matter of the combination and arrangement that will make a difference between how much you pay or save and how much the payment processor makes on your account.

Interested in reading more?

Check out our article about services you can offer to help drive more traffic, increase sales, and offset your merchant expenses:

Buy now pay later payment methods

To contact sales, click HERE. And to learn more about ECS Payment Processing visit Credit & Debit.