Will your current payment systems hold your business back this holiday season? It might be time for you to upgrade your payment processor. Few times are as profitable for retailers as the holiday shopping season. Whether your business already had a great year or whether you’re hoping to make up some losses, the holiday season is the perfect time to boost your sales and revenue.

A strong holiday season also means you can start next year with solid cash flow and, hopefully, some reserves to invest back into the business. In fact, holiday sales make up 20-30% of most retailer’s annual revenue. But to take advantage of the holidays fully, you don’t want anything within your business to hold you back.

For example, ensuring your inventory and suppliers are ready to handle the increased demand. It also means ensuring your promotional strategy is mapped out to attract eager shoppers.

But one thing you may have overlooked is your payment processing. The holiday shopping rush can mean you have new customers in your store. These new customers may want different payment options to be available than you currently offer.

Another thing that can hurt your holiday sales is paying too much in fees for your credit card processing. With high fees, every sale cuts into your profit margins, and it’s essentially money out the window.

These are just two examples, but the right payment processing can help you solve these issues and maximize your profits this holiday shopping season.

Below, we’ll go over how upgrading your payment processor can help you increase profits and decrease costs, all while improving customer service and streamlining your business operations.

Signs That You’ve Outgrown Your Current Payment Processor

Most small businesses obtain a merchant account through a payment processor when launching their business. As you know, you have a million things to worry about when launching a business.

You probably signed up with the first payment processor you could find who seemed reliable. There’s nothing wrong with this, and it’s what most business owners do out of necessity. However, it also means you’ve likely outgrown them and it’s time to upgrade your payment processor.

It may not seem obvious, but it is true that the wrong payment processor can hold your business back with every transaction.

Below are some signs you may have outgrown your payment processor, and a switch before the holidays could mean big savings and increased sales.

Outdated Equipment

Electronic payments have changed in the last few years. Not only has payment technology changed, but so has customer behavior. Customers now demand various digital payment options at every retail establishment they visit. Much of this change has happened in just the last few years, so it’s not uncommon for retailers to be behind this curve.

A perfect example is using digital wallets such as Apple Pay or Google Pay. It’s not unusual for customers to carry no cash or even credit cards when shopping. These customers rely solely on their digital wallets when making secure transactions.

Retail stores without the capability of processing these payments will lose out on these potential sales. If your payment terminals or payment processing can’t take contactless payments, it’s a sign that it’s time to upgrade your merchant services.

It’s also important to note that accepting digital wallets differs from EMV compliance. EMV compliance is related to accepting “chipped” cards. Contactless transactions or NFC payments use Near Field Communication or radio waves to transmit data rather than swiping or dipping cards.

No Point Of Sale (POS) System

A point-of-sale system helps retailers take their business management and sales analytics to the next level. This combination of software and hardware, such as barcode scanners, makes processing your payments faster and speeds up the checkout process. Not only that, but it also helps you manage virtually every aspect of your business easier.

For example, your POS system can handle your inventory management for you and use real-time reporting. This saves time and money from having to perform inventory management manually. A POS system can also help with your sales team and employee management. It can also integrate with HR programs to automate payroll and other tasks.

However, a POS system also needs the right payment processor to maximize its many benefits. If your business has been putting off using a POS system because of difficulties with your payment processor’s capabilities, it’s time to switch or upgrade your payment processor before the holiday season.

Other Benefits Of A POS System

A POS system allows you to easily add a loyalty program to your retail business. Most POS software systems have this ability built in. But you can also choose from third-party providers to add loyalty programs.

These programs help to create a great customer experience that offers them more personalized promotional offers. Loyalty programs also help you drive sales and gain valuable predictive analytics to spot customer trends or pain points.

The advanced analytics that POS systems offer allows you to develop a customer experience strategy based on customer journeys. This helps you increase sales performance by offering your customers personalized and targeted marketing messages.

If you’re looking for ways to improve your customer experience, using a POS system to replace your standard cash register is a great start.

High Processing Fees

High processing fees chip away at your profit margins with every purchase. Processing will always have fees, but finding the lowest fees and best fee structure for your business can save you thousands.

When you first applied for a merchant account, it’s possible that you had no business history. This means it was impossible to accurately measure your sales volumes or average ticket prices.

Your original processing fees were likely higher to account for any extra risk you might have posed early in your business’s life cycle. But now that you have a history, you can likely find a processor with lower fees and better service.

This can be especially true if you’re on a flat rate fee structure. Unless you are selling low-ticket items, a flat fee structure will cost you more than other fee structures. Higher fees mean you make less money during the holiday shopping rush.

Look at your most recent statement from your current payment processor and see what you’re paying in fees. You can likely get a better deal, and what better time than right before the holiday rush? But when does the holiday shopping really begin? Well, a recent study indicated that 37% of shoppers start in November.

Long Contracts

Some retailers may not even know they have long contracts with their payment processors. If you do, this is generally a bad sign, and you want to leave that processor and look for alternatives.

Many times, new businesses end up signing contracts with an evergreen clause. This means the contract automatically renews on a date well before expiration. This locks the retail merchant into another long contract.

These contracts are usually not good for the merchant and heavily favor the processing company. If you’re in one of these, inspect the contract carefully to see when you need to inform them that you don’t want to renew for an extension. Giving yourself an out will allow you to shop for an upgraded payment processor that really cares about your needs.

Poor Customer Support

Bad customer service is a problem for any business service provider. But if your payment processor has bad customer service, you could lose money and customers.

Any issue with your payment reliability during a busy period can impact your earnings. No business wants that. If you have a problem with your payment system, you need it resolved quickly.

If your payment processor takes too long to respond to your questions, you should consider switching. Worse yet, if your payment processor only uses email for support, you have to wait 24 hours or more to get a response.

This type of slow support just isn’t sufficient if you run a serious business. You need a payment processor with responsive, in-house representatives.

You’re Using An Aggregate Payment Provider

Many merchants may not be aware of what an aggregate payment provider is. An aggregate payment provider is a company that pools all of their merchant’s into a single account.

A common example of this is a provider such as Stripe or Square. These companies don’t offer individual merchant accounts. Instead, they offer merchants the ability to process through the provider’s merchant account.

The advantage of using these providers is that signing up for processing is usually fast, and approval is almost instant in some cases. This is because they pool the risk of all their merchants together.

However, the downside of this is that you pay much higher fees. So, during a busy time like the holiday shopping season, you lose money with every transaction.

The aggregate providers also don’t offer personalized customer service. So, if you have a problem, you must use their website or chat feature to reach someone. Unfortunately, many times, the person you reach is an outsourced employee.

On the other hand, a merchant account provider like ECS Payments gives merchants their own merchant account. These have lower overall fees and more customization options than an aggregate payment solution.

One of the best ways to boost your revenue this holiday season is by switching from an aggregate provider and applying for your own merchant account. You’ll start saving money with every transaction, and switching is very easy.

How To Upgrade Your Retail Payment Processor

Switching to a new payment processor is easy. With a little research, you can quickly upgrade with zero downtime and start saving money and reducing your costs almost immediately.

There are a few things you want to look for when upgrading your payment processor. This list will help you find the perfect upgraded payment processor for your business.

Choose A Fully Integrated Payment Solution

You need a fully integrated payment system to take full advantage of all the tools that modern payment processors offer. Integration means that your payment system communicates with your other business software.

These integrations streamline your business operations to save money on labor costs and reduce redundancies. In many retail settings, these integrations also allow you to use advanced analytics to gain insight into your customers.

By combining sales data with a CRM solution, a retail business can segment its customers and send each group personalized marketing messages. This type of personalization based on buying history can raise revenue, repeat business, and average ticket size.

Mobile Payment Solutions

Depending on the type of goods or services you offer, mobile payment solutions may help you reach more customers and increase sales. 48% of holiday shopping is completed on mobile devices.

For retail stores, mobile payment processing allows customers to complete payments on their smart devices.

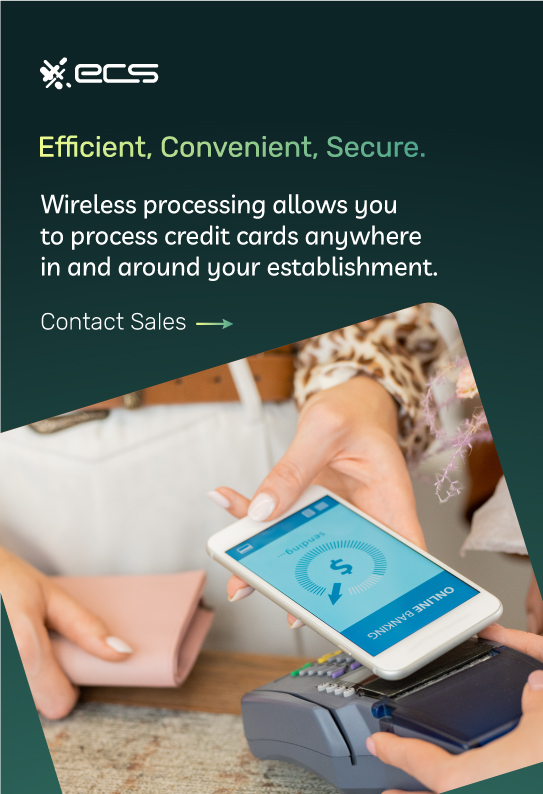

Another feature is wireless card processing. If you operate a restaurant or large retail store, wireless credit card processing allows you to place checkout areas strategically for enhanced customer experience. Or retailers can go to where their customers are. This means attending events or other venues to sell your products and collect payments.

Wireless processing allows you to process credit cards anywhere in and around your establishment. This flexibility opens up new layouts and ways to service your customers faster and more conveniently.

Transparent Pricing

If you find it difficult to understand your current monthly statements from your payment processor, then you already know how important transparent pricing can be.

When you switch payment processors, the new processor should clearly explain all your fees and monthly charges. Look for any “junk fees” or other monthly charges. These are usually the signs of a payment processor offering a lower service level.

Transparent pricing should also extend to your processing fees. If you use interchange-plus pricing, the processor should disclose each type of transaction with its accompanying interchange fee. The payment processor should also disclose its fees on top of this for each transaction.

Most retail businesses will prefer to use interchange-plus pricing. However, some retailers with smaller average ticket prices may prefer flat-rate pricing.

If you’ve been in business for at least a year, you should be able to look at your transactions and determine which processing fee structure will save you the most money.

Full Payment Options

Retail customers today want payment options. These options include credit and debit cards, but they also include new options like digital wallets.

Right now, there are three major digital wallets. Those are Apple Pay, Google Pay, and Samsung Pay. However, that can change quickly as digital wallets are a relatively new technology, and their adoption happened much faster than people realized.

One of the best ways to increase your sales is to offer as many payment options as necessary. Increasing the number of payment options available drives more sales and increases average ticket prices. All of this means higher revenue for your business.

This can be especially true during the holidays, as busy shoppers may stop in for last-minute purchases and not have their physical credit or debit cards with them. Offering other options ensures you can still make the sale.

Other options to consider for some retail environments are ACH payments or eChecks. If you accept paper checks, you must convert them to eCheck for processing. Lower processing fees and faster payments are some of the benefits of using eChecks.

You can increase sales and get paid faster by offering these extended payment options, especially for larger ticket items.

How Complicated Is It To Upgrade Your Payment Processor Before The Holiday Season?

It’s not uncommon for a small retail business to be unhappy with their current payment processor, but they’re afraid to switch. Most of this is due to thinking that switching will be very complicated and upset their business operations.

However, upgrading your payment processor is quite easy, even for large businesses or chains with multiple locations.

Most, if not all, of your other business systems will stay exactly the same as they are now. You will just have to configure them to access your new payment processor.

Below, we’ll go over some different areas of your payment workflow and explain how easy it is to switch.

Hardware and Card Readers

If you plan on keeping your current terminals and card readers, that isn’t a problem. However, if they are outdated, you would be wise to upgrade them when you upgrade your payment processor. You will save both time and money by doing it both at the same time.

If you already have updated card readers, you will configure them to access your new payment provider. If they are standalone terminals, you can either connect them to a computer or configure them via their controls.

If your POS system is connected to the card readers, then you change the payment gateway information within the POS system. You can complete this process in just a few minutes without technical knowledge.

If you choose to upgrade your card readers simultaneously, they will already be fully compatible with your new payment processor. Whether you decide to keep your current terminals and readers or upgrade, switching is very easy and will only take a few minutes in most cases.

POS Systems

If you currently use a POS system, upgrading your payment processor should be very easy, and you will only need to change a few settings.

Before switching, make sure your payment processor knows which POS system you are using. This will help them decide which payment gateways they offer that are compatible with your POS system. However, most POS systems are compatible with various payment gateways and processors, so compatibility is usually not a problem.

There are settings within your POS system that you can easily access via the menus. You will change your payment processor and payment gateway conditionals in the settings menu.

If you operate a retail store chain and utilize a cloud-based POS system, you can push some changes to all of your stores. In some cases, you may need to change the payment gateway manually. Ask your new payment processor or POS vendor if you run multiple locations and need to change these settings.

Other Business Software and Integrations

You can configure any other business software that integrates with your payment processor the same way you changed your POS settings. Each software vendor will be slightly different, but you essentially change the payment gateway credentials in each one.

You will need to export and then import any customer data stored with your old payment processor or payment gateway. This is an easy process, and every payment gateway has an import and export function for this purpose.

However, this is only for data stored with your payment gateway or processor. Any data you store locally or on cloud-based business systems like a CRM is unaffected by a change in payment processors.

Since most businesses use cloud-based business software, data migration is generally unnecessary when upgrading your payment processor.

How Soon After I Upgrade Payment Processors Can I Start Accepting Transactions?

Some businesses know they should switch payment processors, but they are worried about any downtime or disruption to their sales.

But a switch only takes a small amount of time, and once the switch is complete, you can immediately start accepting payment again.

After switching your hardware and software, you’ll want to run a few test transactions. Your payment processor can supply dummy card information for this purpose. After testing, you are ready to start accepting payments as usual. Ultimately, knowing you are saving money with your upgraded payment processing.

More Help With Upgrading Your Payment Processor

As the holiday shopping season approaches, there’s no better time to consider upgrading your payment processing. By offering enhanced services, you can boost sales and average ticket amounts. With lower fees, you’ll be saving money on every transaction.

When you’re ready to upgrade, contact ECS Payments. Our experts can walk you through the upgrade process and show you how much money you’ll save each month after you upgrade.

Don’t go another season with an expensive payment processor. Start boosting your sales and profits by upgrading with ECS Payments and make this holiday season your most profitable ever.

Frequently Asked Questions About Upgrading Your Payment Processor

The right payment processor can enhance customer service, streamline business operations, and save you money on processing fees. Additionally, when you offer a variety of payment options, including mobile payments, ACH, wireless, and virtual terminals, you’re offering more ways for customers to pay, which increases your reach and boosts sales. If that sounds like something you want to take advantage of, contact ECS Payments today to optimize your payment solutions and maximize your profits this holiday season.

Signs that you’ve outgrown your current payment processor include outdated equipment, or the absence of a Point of Sale (POS) system, high processing fees, and poor customer support. If your business is experiencing any of these issues, it’s time to consider upgrading your payment processor. Contact ECS Payments for lower fees, customized solutions, and a dedicated in-house customer support team.

When upgrading your payment processor, consider a fully integrated payment solution that communicates with all your other business software for a streamlined operation. Additionally, transparent pricing and offering various payment options are essential. Contact ECS Payments to explore how we can set you up with these capabilities and lower your processing fees.

Upgrading your payment processor is not complicated and can be done with minimal downtime, if any. ECS Payments can help ensure a smooth transition and data migration, if applicable, should you decide we are in fact, the best option for your business.