Enterprise payment processing encompasses everything large corporations need to successfully complete customer transactions. What do they need to maintain their operation, make sales easy, and continue to grow?

This article will go over everything you need to know about enterprise payment processing and beyons. Our hopes is that this article will help your business meet its goals and make more sales.

What’s An Enterprise Business?

There are almost 33 million businesses in the United States, but 99.9% are small. According to the Small Business Administration, a small business has fewer than 500 employees. And according to the SBA, there are only around 21,000 large businesses.

Interestingly, this threshold is markedly different from the European Union, where 50 employees is the cutoff, and Australia, where it’s 15. The difference in these numbers tells you that in America, big business means big business—with a lot of human capital and different parts.

Enterprise however, refers to a large company with divisions, departments, and a board of executives. Enterprise companies have gross receipts totaling millions or billions of dollars. This number is much more significant than the 86% of businesses that make $100,000 or less annually.

An enterprise company needs different solutions than a small or midsize business in almost every area of its operations. And payment processing is no different.

Take Walmart, for example. Walmart runs around 37 million transactions per day. McDonald’s runs 69 million. And Amazon processes around 19 transactions per second.

A Variety of Payment Methods

Enterprise payment solutions need to have some variety. It’s not just because variety is the spice of life (or so they say). It’s because a large organization will need to facilitate B2C and B2B interactions, and perhaps even P2P or C2C interactions (like in the case of a marketplace).

Enterprise payments technology should encompass all payment types: debit cards, credit cards, ACH, digital wallets, mobile payment apps, and even cash (if it has brick-and-mortar locations). Think of your own experience shopping at enterprise businesses. It would be frustrating to be told this location only accepts Mastercard or only accepts Visa—especially if you only have the other one in your wallet.

An enterprise merchant needs to be able to accept different payment types. One reason variety is significant is that enterprise businesses will cater to various people. Niche businesses may only interact with specific demographics. But companies like Target and Amazon cater to all different types of people.

Credit cards are most popular with consumers 65 and older, and debit cards are their least favorite payment method. By contrast, members of GenZ are more inclined to use debit over credit—perhaps due to aversion to credit or because they are too young to get it. Consumers aged 18-34 show substantially more interest in paying with a digital wallet, while those aged 35-49 are more interested in using PayPal.

In conclusion, an enterprise payments platform must accept payments in its various incarnations. Without that capacity, the enterprise will risk losing substantial chunks of business.

Online Payment Experience is Important

Niche customers are a dedicated lot. Suppose there is only one place to get their niche gear. In that case, there is a greater likelihood they will tolerate a poor user experience. They understand that the business they’re shopping at (online or in-person) may be a low-tech family affair. In fact, that may even add to the charm or appeal of the experience.

Consumers feel differently about shopping with a Fortune 500 business. If they order groceries online and the payment page glitches, they’ll go to a different site. If they walk into Target and someone tells them that all the POS machines are down and it’s cash only, they may walk out and go to Walmart.

Though such a portrayal of consumer impatience may seem hyperbolic, captured data confirms it. The global average for online retail cart abandonment is almost 73%. And the same number of consumers will leave a store website for one with a better user experience.

In summary, in addition to offering a variety of payment methods, which we just spoke about, an enterprise payment gateway must be fast and functional. These attributes create an overall positive customer experience at checkout, which will not only lower the cart abandonment rate but also create repeat customers.

In-Store Payment Experience is Important

But let’s not forget about brick-and-mortar footprints. The point of sale inside a brick-and-mortar store can also make or break a customer experience. Slow, dysfunctional, and limiting systems will create a backup in the store, which will drive customers away.

Research has found that 96% of consumers have left a (physical) store at least once empty-handed. The most common reasons were that they couldn’t find the product they wanted (67%), or the store didn’t even have the general item in any brand (66%), the lines were too long (55%), and customer service was poor (39%).

As you can see from these findings, one out of two customers will walk away if the lines are too long. And that’s saying something in an era when consumers typically don’t mind standing in place and mindlessly scrolling through Instagram.

Tangentially, we should mention that other significant reasons customers leave a store include messy restrooms. This detail is more impactful in some industries than others.

79% of consumers will not return to a restaurant if the bathroom is dirty, probably because 86% of diners assume the cleanliness of the kitchen matches that of the bathroom. But 55% of consumers would be willing to return to gas stations with messy restrooms, which tells you something interesting about consumer expectations.

In any case, stock up on toilet paper and seat covers. Keep those floors and surfaces clean. And definitely avoid using POS systems that slow down transactions and create long lines.

Long Lines, Contactless Payments, and The Consumer Eyeball

The culprit behind long lines can be understaffing, slow associates, or a cashier trying to get some digits. But merchant services technology can also be the culprit behind longer payment times.

Contactless payments are the fastest way to pay, taking less than a few seconds. EMV chip insertions can take up to 15 seconds. As for magnetic strips, they will be disappearing from cards entirely by the 2030s, but for now, they can also slow things down.

Enterprise payment services must use the latest hardware and software to facilitate rapid payments at the point of sale. In most cases, this is going to mean contactless payments. Enterprise payment systems should handle all types of contactless payments, including cards, phones, and perhaps even hands.

That’s right—the future of contactless payments may lie in biometric payments. Mastercard has already been testing this technology out in foreign markets. With biometric checkout, consumers register their hand or face with Mastercard’s database.

At checkout, they can show their hand or face to a scanner, which will match the image against the registered biometric data. The program was a marketed success in Brazil at a midsize upscale grocery chain.

Incentivizing Certain Types of Payments

Large enterprise payments solutions may eventually rely on biometric data. However, just as enterprises must honor the diversity of their customer base regarding payment preferences, they must honor the gradient of receptivity toward biometric payments.

Not everyone will want to register their bodies with their credit card company. However, if biometrics proves to be of significant impact in enterprise solutions for payment processing, companies may choose to incentive these methods of payments. For instance, customers who pay with a retinal scan could get a 5% discount–as creepy as that sounds.

Incentivization is already a strategy frequently used in enterprise merchant services. In conjunction with financial institutions, big brand retailers frequently offer customers store credit cards.

Studies have shown that 60% of consumers report shopping more often at retailers with which they have a credit card. And store credit cards amount to a significant number of sales. 60% of sales at Kohl’s and 50% at Macy’s are done with their branded cards.

Store credit cards do tend to have higher interest rates. Still, that interest is collected by the financial institution servicing the card (in many cases, Comenity Bank). But store credit cards are still worth their weight in gold for enterprise businesses because they create customer loyalty and allow the store to mine customer data. More on that later—but first, let’s wrap up discussing customer experience.

Other Aspects of Customer Experience

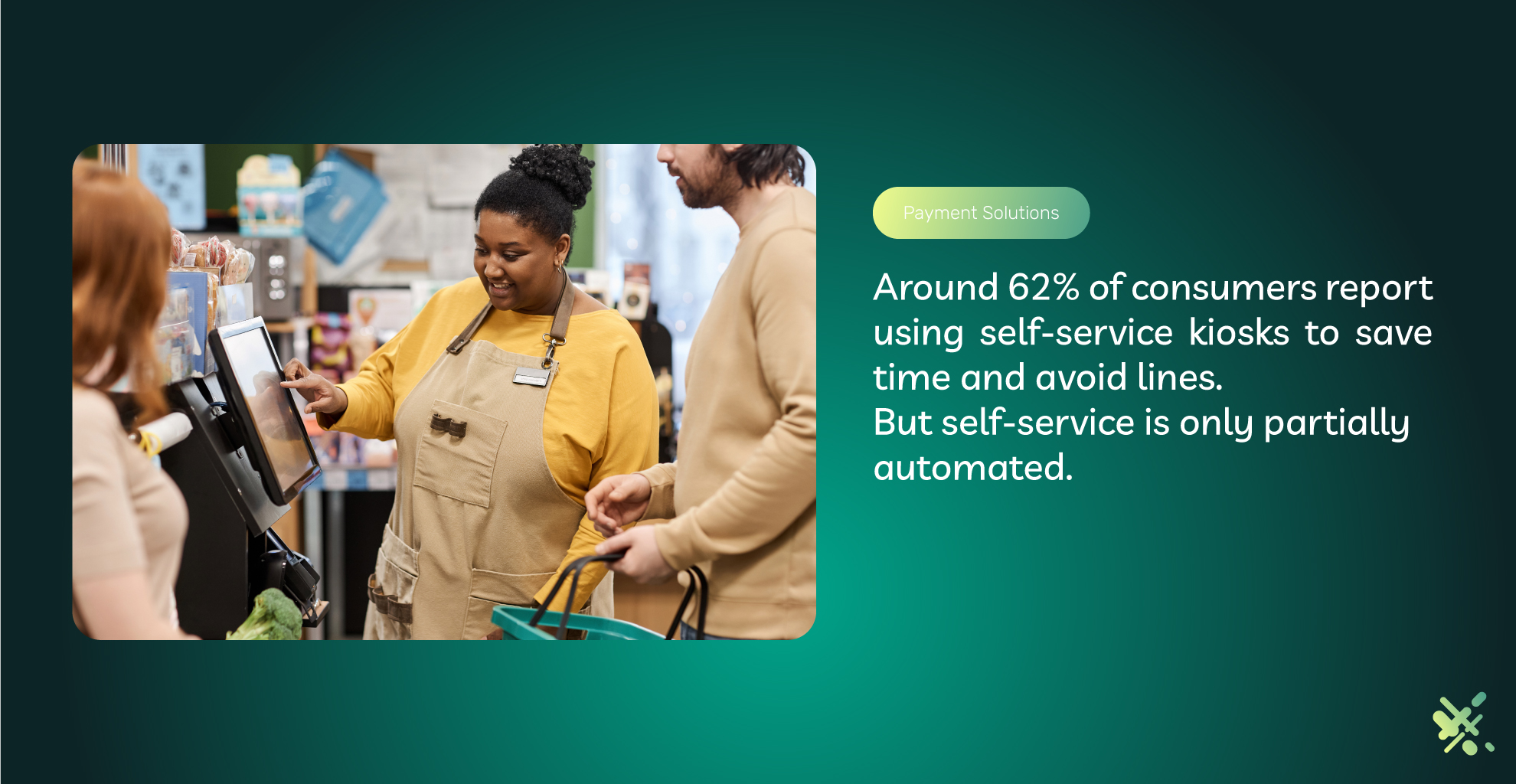

Enterprise payment processing systems need to handle new modalities in B2C interaction. One of those is self-checkout. Around 62% of consumers report using self-service kiosks to save time and avoid lines. But self-service is only partially automated.

For now, a store associate must stand at a central terminal, observe checkouts, and respond to problems. It helps to know PLU codes by heart. Pineapple is 4433 unless it’s a large one (4430) or a small one (4431). Please place your item on the scale. For everything else, there’s Mastercard.

In any case, the monitoring required of a store associate means that the self-checkout stations must have a link to some supervision terminal. This connectivity requires a more complex software solution than individual, unsupervised terminals.

Will Self Checkout Replace Cashiers?

85% of GenZ shoppers prefer self-checkout over interacting with a clerk. Is it because they’ve collectively lost the art of friendly small talk? Maybe. Sociologists are indeed concerned they might be the loneliest generation. But in any case, self-checkout is here to stay.

Women prefer using self-checkout less than men (56% to 61%). Around 14% of shoppers use them every time they shop, avoiding all small talk. The global market for self-checkout has an estimated value of $3.44 billion, at a CAGR of 11.6%.

So yes, self-checkout is here to stay. Amazon has even experimented with cashierless, (nearly) employee-less stores. In these automated venues, shoppers select what they would like, leave the store, and have their accounts charged against the items they selected.

Will self-checkout replace cashiers? It’s a question that goes beyond retail. It ties into more extensive questions about AI, humanity, and perhaps movies starring Arnold Schwarzenegger. In all seriousness, eCommerce sales have cooled in recent years, when it initially had the market believing it would replace brick-and-mortar business.

It turns out that people are indeed social creatures and like to get out. They like to feel merchandise in their hands, catch a bite at the food court, and enjoy air conditioning in the summer. Consumers want a human touch. For instance, while 13% of polled consumers were enthusiastic about shopping in an automated store, 70% preferred a hybrid mix providing at least some human interaction.

Automated Payments Experiences: A Cost-Benefit Analysis

And now to the part that really matters: profits. Going (at least) hybrid and having some cashier-less self-checkout stands may reduce staffing needs and, in turn, payroll costs. The connection between self-checkout and increased shrinkage is undeniable. For instance, one survey in the UK found shrinkage in automated stores to be at 4%, while it was just 1.5% in stores with cashiers.

However, the reduced payroll costs make up for losses due to theft. An MIT study suggested that a four-terminal bank of self-checkout stands could cost around $125,000 to set up, compared to just $1,500 for four manned registers. But wait, there’s more. With the average clerk earning a little under $12 per hour, those four manned registers will cost $96,000 per year.

By contrast, the automated registers only need one clerk to operate them, costing $24,000. And can you imagine if a $20 minimum federal wage gets legislated? Now, your four manned POS terminals will cost $192,000 per year versus $48,000.

The bottom line is that in a cost-benefit analysis, automated terminals are a must-have for large enterprise businesses with a brick-and-mortar presence. In fact, consumers expect and (some) even prefer them. Enterprise payment processing will need to provide the hardware and software that facilitates this type of automation.

Enterprise Sales Floor Customer Support

Even before checkout, consumers are desirous of technology integrating with payment processing systems. These technologies facilitate a smoother shopping experience. For instance, 53% of shoppers seek out employees with tablets. 24% of these customers want more product information, and 23% want to know if it’s in stock.

These types of inventory-related solutions are necessary to integrate with a payment gateway. The owner of a small store will know if they’re out of a specific item. But an associate at Walmart will not know if there is more Charmin toilet paper in the back unless the inventory management and the cash registers are linked.

Points and Rewards

Another aspect of enterprise payment processing is loyalty programs. Small businesses are often content handing out punchcards and tracking points with a hole puncher or a stamp. Savier business owners may use a cloud solution like Toast (that one is mainly geared toward restaurant owners).

But these solutions will not work for enterprise customers. An enterprise payments strategy must be integrated with an automated and proprietary points program (meaning, in-house). It needs to be seamlessly blended with the online shopping experience.

Enterprising businesses are even making their loyalty programs integrated with in-store visits. Retailers track consumers within their stores, observe their behaviors, and push coupons and discounts to particular consumers based on their behavior.

These types of advanced solutions require integration with payment processing technology. Businesses can specifically tailor rewards to customers based on their purchasing patterns. And that can only be tracked when the loyalty program and the payment gateway are in sync.

The payoff of loyalty programs is significant. More than 90% of companies have a loyalty program. These companies enjoy an average of 12-18% revenue growth per year per loyalty customer. 84% of consumers indicate they’re more likely to have brand loyalty to a company with a loyalty program.

Loyalty Programs and Consumer Decision Making

Interestingly, brand loyalty is often easier for local businesses, even though enterprise companies have more penetrative and pervasive brand recognition. Brand loyalty is an advantage that the proverbial Main Street family-owned business has over large corporations.

Consumers may feel less sentimental about picking out their goods in a supersize, big-box store or ordering things on Amazon. But corporations have long been aware that consumer decision-making is emotional. How many lifetime customers has McDonald’s generated by handing out toys in a Happy Meal or even naming it a Happy Meal?

Loyalty programs allow enterprise businesses to penetrate consumer decision-making as effectively as local businesses with more natural sentimental value. Offering rewards and discounts uses the power of positive reinforcement to drive repeat business with increased profits.

But loyalty programs—especially with millions of subscribers—cannot come as a punch card. A cloud-based, integrated solution is needed…one that interfaces with payments.

Enterprise Analytics

Enterprise analytics is another area where it becomes evident that enterprise-sized solutions are needed in customer data. For millennia, businesses had little recourse to understand their consumers aside from their own two eyes.

If a particular item was flying off the shelves, intuition would tell you to order more. Centuries of trial and era gave rise to maxims like “stack it high, watch ’em fly”—that is, eye-level stacks of goods are more likely to sell than low-lying merchandise.

That all changed in the 20th century with the advent of payment technology. The point of sale has become a gateway for observing customer trends to a level of unforeseen nuance. If you’d like to see it at work, note how online vendors like Amazon pair items together and make suggestions to upsell: customers also bought this! And this!

Enterprise companies have millions of customers and, consequently, billions, if not trillions, of data points to analyze. Far from useless information, this so-called “big data” is a treasure trove of potential profit. For instance, 35% of Amazon’s revenue comes from its recommendations based on big data.

Big Enterprise companies are harnessing the power of big data to make real-time decisions. Walmart even built a dedicated Data Cafe at its Arkansas HQ. This state-of-the-art facility can translate raw data into actionable insights within minutes.

The informational gateway for collecting this data is the point of sale, which means that enterprise payment processing solutions need to integrate with analytic software. This step is exceptionally vital for enterprise businesses because every competitor is doing it. Enterprises that do not leverage big data will fall behind and lose market share.

A Lot To Lose: Fraud and Safety

Yet another consideration for enterprise payment processing is fraud prevention and safety. In some aspects, small businesses are targeted more often than large businesses regarding fraud. It’s easy to see why—they don’t have the same resources to allocate to cyber defense as large corporations.

But enterprise companies have more to lose. That has been shown repeatedly over the last two decades, most infamously in significant data breaches. The 2013 Target Data Breach impacted 70 million customers.

International companies with a large footprint may be holding millions of names, addresses, credit cards, and other potentially exploitable pieces of information. Enterprise payment processing systems need to be at the forefront of data security. This is especially true for businesses that retain customer financials for recurring billing or accounts to facilitate faster checkout.

Enterprise Payment Processing Wrap Up

In summation, enterprises need payment processing solutions that differ from small and midsize businesses. This article was by no means exhaustive, and there are other details to discuss, such as volume pricing, invoicing, and accounting. There are areas where payment processing and merchant services could overlap with HR, for instance, in terms of payroll.

Visa estimates that there are 1,300 payment processing companies worldwide, but most simply won’t work for an enterprise account. And ironically enough, large payment processing companies like Venmo, PayPal, and Square won’t work either. These companies are good for helping small businesses with low sales volumes collect payments.

If you have any questions about enterprise-level payment processing technology, call or contact us via the form below to learn more.

Frequently Asked Questions About Enterprise Payment Processing

Enterprise businesses should consider various payment methods to cater to different customers. It depends on your product and service offerings and how your business is set up. Enterprises may need mobile, virtual, or stationary terminals to process credit, debit, or ACH. To learn more about implementing a diverse range of payment solutions, including contactless payments and more, contact ECS Payments.

Enhancing the online payment experience for enterprise customers can significantly boost customer satisfaction, decrease cart abandonment rates, and ultimately drive higher sales. For further insights and expert guidance on creating a positive online payment experience and reducing cart abandonment, contact ECS Payments.

Key strategies include streamlining the checkout process to make it concise and user-friendly, optimizing the system for mobile devices, offering multiple payment methods, emphasizing security measures with trust badges and SSL certificates, implementing real-time validation of payment information, ensuring transparent and informative error handling, and delivering clear payment confirmations. For further insights and expert guidance on creating a positive online payment experience and reducing cart abandonment. Contact ECS Payments for a streamlined payment gateway experience.

Analyzing customer data is essential to improve your business. ECS payments offers easy integrations with your current APIs, accounting software, and payment solutions. We also have designed a dedicated merchant portal that provides you with all your payment data to easily analyze your sales. To explore how payment processing systems can integrate with analytics software and help your business make real-time decisions, reach out to ECS Payments.