Most business owners don’t wake up wondering about the merchant account vs payment facilitator debate. They just want to accept payments and get paid. That’s understandable. When you’re opening a new store, launching an ecommerce website, or replacing an aging point-of-sale system, payments often become another item to check off a long list.

Then something unexpected happens.

A payout is delayed. A large transaction triggers a review. Customer support becomes difficult to reach. Suddenly, the way your payment processor is structured matters a lot more than it did during signup.

Behind nearly every card transaction is one of two models: a dedicated merchant account or a payment facilitator. While they accomplish the same basic goal of helping businesses accept payments, they operate very differently behind the scenes.

The differences behind a payment facilitator and a merchant account influence a business’s account stability, funding speed, pricing flexibility, customer support, and how well your payment solution grows alongside your business.

Choosing the right model isn’t about finding a winner. It’s about understanding where your business is today and where it’s headed tomorrow.

What Is a Merchant Account?

A merchant account is a payment processing account established specifically for one business. Rather than sharing processing privileges with thousands of unrelated merchants, your company receives its own dedicated account after completing an underwriting process.

Merchant account underwriting often gets a bad reputation because it requires more paperwork and more time. Think of it like buying a house instead of renting an apartment. It takes longer to get approved, but once you’re in, there’s generally more stability.

The processor evaluates your business before you begin accepting payments instead of trying to figure out your risk profile afterward.

How Merchant Accounts Work

The process typically starts with an application that includes information about your company, ownership, expected processing volume, products or services, and banking information.

From there, the payment processor reviews factors such as industry risk, average transaction size, processing history, chargeback exposure, and financial stability. Once approved, your business receives its own merchant account.

Every transaction you process is associated with that account instead of being grouped under someone else’s master account. That distinction becomes increasingly valuable as your business grows.

Common Merchant Account Providers

Merchant accounts are commonly offered through traditional payment processors, banks, independent sales organizations (ISOs), and specialized providers like ECS Payments.

The quality of service varies considerably. Some providers simply process transactions. Others help businesses optimize payment acceptance, reduce processing costs, integrate software platforms, and navigate PCI compliance. Those differences often matter far more than whatever marketing slogan appears on the homepage.

What Is a Payment Facilitator?

Defining a Payment Facilitator

A Payment Facilitator, or PayFac, allows businesses to begin accepting payments under the facilitator’s master merchant account. Instead of receiving a unique merchant account immediately, businesses become sub-merchants operating beneath the larger payment platform.

How Payment Facilitators Work

Payment facilitators are known for their setup speed. The application process is short with automated approvals. Many businesses can begin accepting payments within minutes, rather than days.

The tradeoff is that underwriting happens differently. Rather than conducting an extensive review before processing begins, PayFacs rely heavily on continuous monitoring. Sophisticated algorithms watch transaction activity for unusual behavior, large sales spikes, refund activity, and chargeback trends.

When something falls outside expected patterns, an account review can happen quickly. Sometimes those reviews are justified. Other times, they’re just the result of software doing what software was programmed to do. And these reviews can interrupt a merchant’s business entirely.

Examples of Payment Facilitators

Several of today’s most recognizable payment brands use the payment facilitator model, including:

- Stripe

- Square

- PayPal

- Other aggregated payment platforms

These companies have made online payments dramatically easier for millions of businesses, especially entrepreneurs launching new products or testing business ideas.

Merchant Account Vs Payment Facilitator Comparison

| Merchant Account | Payment Facilitator | |

| Setup speed | Days: Underwriting required upfront | Minutes: Automated approval |

| Account stability | High: Pre-reviewed before processing | Variable: Holds possible with volume spikes |

| Pricing model | Interchange-plus: Customizable as volume grows | Flat rate: Simple but often costs more |

| Customer support | Dedicated: Knows your account history | Shared: Ticket-based, no account context |

| Funding speed | Reliable: Predictable deposit schedule | Varies: Can be delayed during reviews |

| Scalability | Strong: Multi-location, integrations, B2B | Limited: Best for simple, lower-volume use |

| Best For Merchant Account Established businesses, growing volume, complex operations, or anyone who’s been burned by a PayFac freeze. |

| Best For Payment Facilitator Startups, side businesses, seasonal sellers, or anyone who needs to accept payments this weekend. |

Account Structure

A merchant account creates a direct relationship between the business and its payment processor.

A payment facilitator creates a relationship between the business and the platform, with the platform maintaining the primary merchant account.

Approval Process

Merchant accounts require more documentation upfront, whereas payment facilitators prioritize immediate activation with lighter onboarding requirements.

Neither approach is inherently better. They’re simply solving different business problems. If you’re opening a pop-up shop this weekend, waiting several days for underwriting may not be practical. If you’re processing several million dollars annually, investing additional time before launch is usually worthwhile.

Business Control

Businesses operating under dedicated merchant accounts typically have greater visibility into their payment environment and more opportunities for customization.

Payment facilitators, on the other hand, generally maintain tighter control over risk policies, onboarding standards, and operational decisions because every sub-merchant affects the larger platform.

It’s similar to living in a condominium with an HOA. You gain convenience, but someone else writes many of the rules.

Why Many Businesses Start With a Payment Facilitator

Fast Setup

Speed is the biggest selling point. Many entrepreneurs need to take payment immediately. They aren’t interested in lengthy applications while trying to launch a business. Well, no one is, for that matter, but the lengthy process, with sufficient underwriting, can save you in the end and lessen your chances of account suspension and review in the middle of a busy day.

Easy Online Payments

Integrating online checkout has become incredibly simple through platforms like Stripe and Square. Small business owners love a checkout page that works without hiring an IT department.

The simplicity of integrating online payments has helped accelerate ecommerce growth over the past decade. E-commerce now accounts for nearly 17% of all U.S. retail sales, a share that has steadily climbed as online purchasing has become a normal part of everyday shopping.

Low Barrier to Entry

Businesses with little or no processing history often find payment facilitators easier to access. When you’re selling handmade candles out of your garage or testing a subscription idea on weekends, the PayFac model removes much of the traditional friction associated with merchant underwriting. Once you’ve got some processing history under your belt, a true merchant account is a great way to go. But merchant accounts still work great for brand new businesses.

Common Challenges With the Payment Facilitator Model

Account Holds and Reviews

Imagine an online retailer that normally processes $8,000 per month. One weekend, a TikTok video goes viral, and sales jump to $80,000.

Great news.

Unless your automated risk system thinks someone may have stolen your account, large changes in transaction patterns frequently trigger reviews. While these measures exist to reduce fraud, they can also temporarily interrupt legitimate businesses.

Funding Delays

Of course, cash flow is oxygen for small businesses. A temporary delay in funding might be manageable for some, but it’s a different story for most. Processors aren’t trying to make life difficult. They’re simply protecting themselves from financial exposure. Unfortunately, merchants often feel the consequences first.

Limited Personalized Support

Large payment platforms serve millions of businesses. Though it’s quite efficient on their end, it doesn’t always create the best relationships. Many merchants eventually find out there’s a meaningful difference between submitting an online support ticket and having a dedicated payments specialist who already understands your account history.

Less Flexibility for Complex Businesses

Companies with recurring billing, B2B invoicing, ERP integrations, Level II or Level III processing, or specialized payment workflows often outgrow the standardized approach offered by many payment facilitators.

Advantages of a Dedicated Merchant Account

Greater Account Stability

With a dedicated merchant account, underwriting plays a huge role. An account application undergoes extensive underwriting before processing begins. That doesn’t eliminate risk reviews altogether, but it generally creates a more predictable operating environment because your processor already understands your business model, which means less or no unforeseen account holds.

Dedicated Support

Whether it’s a terminal issue during the holiday shopping rush or an unexpected authorization problem on Monday morning, speaking with someone familiar with your account saves time and frustration. At ECS Payments, we are known for our personalized and easy to reach customer service.

Customized Pricing Opportunities

Flat-rate pricing is simple. But it’s not always the least expensive.

As transaction volume increases, many businesses become eligible for interchange-plus pricing or customized pricing structures that better reflect their processing profile. That’s one reason companies frequently revisit their payment strategy after experiencing sustained growth. You cannot do that with payment facilitators. These companies make their profit through flat-rate pricing structures.

Better Scalability

Growth changes everything. What works for ten transactions a day may create the biggest headaches at a thousand. Dedicated merchant accounts generally provide:

- Greater flexibility for multi-location businesses

- omnichannel commerce

- recurring billing

- commercial card acceptance

- integrated software solutions

- and industry-specific payment requirements.

According to the 2024 Global eCommerce Payments & Fraud Report, 82% of merchants added at least one new payment method over the previous year, highlighting how payment operations become more complex as businesses grow.

Which Businesses Benefit Most From a Merchant Account?

Merchant accounts can be beneficial for any business, honestly. But here are a few examples of specific merchant types and the needs that a dedicated account can offer:

- B2B Companies with payments that involve invoices, ERP systems, purchase cards, and higher transaction values.

- Healthcare organizations require payment systems that support secure workflows, recurring payments, integrated software, and strict compliance expectations.

- Contractors and Field Service Companies, such as Roofers, HVAC companies, plumbers, and electricians, that regularly process large payments in the field and need different transaction avenues such as mobile terminals, payment links, and reliable funding.

- Growing Ecommerce businesses that need more sophisticated fraud prevention tools, subscription billing requirements, inventory integrations, and international payment considerations.

Which Businesses Benefit Most From a Payment Facilitator?

Payment facilitators can be the right choice for many businesses, such as

- Startups

- Businesses that need payment acceptance immediately.

- New ecommerce businesses with modest sales volume

- Companies testing seasonal products, limited-time services, or entirely new business ideas

- Single-person businesses

Though a payment facilitator can be the right choice for these types of businesses, it’s not always the case. As ECS Payments, we have merchant accounts for multi-location brands and a small business bakery with a single person running the whole show at Saturday farmers’ markets.

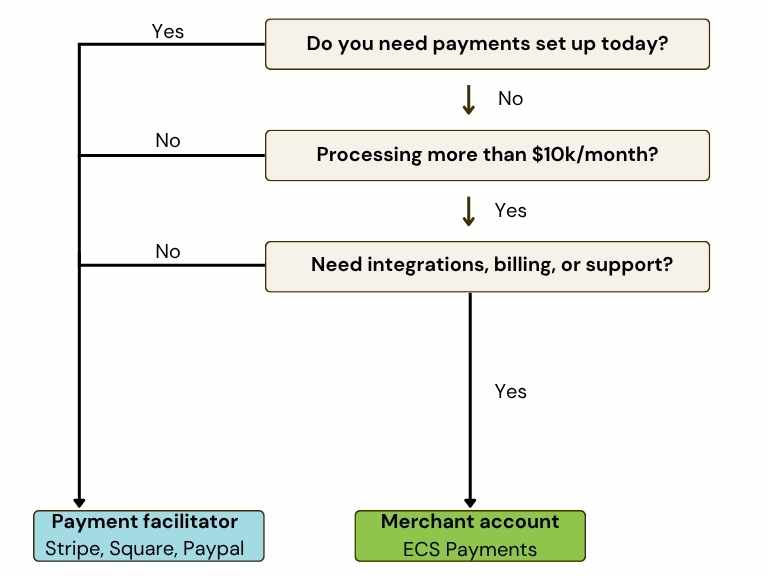

Should I Use A Merchant Account Or Payment Facilitator

Before choosing either model, ask yourself a few practical questions.

- How quickly do you need to begin accepting payments?

- What transaction volume do you realistically expect within the next year?

- Will you benefit from dedicated customer support?

- Do you require software integrations beyond basic checkout functionality?

- Most importantly, how important is long-term account stability to your business?

Those answers usually point toward the right solution more effectively than comparing marketing brochures.

Why Businesses Move From Payment Facilitators to Merchant Accounts

Many businesses replace payment facilitators because they’ve grown. It’s not always the case that something went wrong. However, unavailable merchant support and account freezes are known to be a common hindrance.

But the fact is, higher processing volume often creates opportunities for better pricing. And with more transactions, you’re looking at more complex operations, the need for additional reporting, and more integrations with multiple sales channels. The business complexity has grown, and so the need for direct relationships with people who understand their business, instead of waiting in online support queues, is huge. It’s a natural progression for successful companies to move from a payfac to a merchant account.

How ECS Payments Supports Growing Businesses

At ECS Payments, businesses receive dedicated merchant accounts designed to support long-term growth rather than temporary payment acceptance. Transparent pricing helps merchants understand exactly how processing costs are calculated. Integrated payment solutions support ecommerce, retail, mobile payments, recurring billing, virtual terminals, payment links, and industry-specific software integrations. And, perhaps most importantly, ECS Payments Merchant Services pairs technology with experienced payment professionals who understand that every business operates differently.

One-size-fits-all payment processing rarely stays one size forever. Scalable infrastructure gives businesses room to expand without constantly changing processors every few years.