Running a business is often a balancing act between providing a great product and ensuring the money actually hits your bank account without a headache. If you have ever looked at your monthly processing statement and felt like you were reading a foreign language, you are certainly not alone.

Many business owners treat their payment setup like a utility. A bill that has to be paid in order to run their business. Something that just runs in the background until it breaks or becomes too expensive to ignore. However, neglecting the specifics of your merchant services can lead to leaked revenue and frustrated customers. Understanding the infrastructure behind every “beep” of a credit card terminal is the first step toward reclaiming control over your bottom line.

What Are Merchant Services?

At its most basic level, the term “merchant services” refers to the suite of financial services and technology that allows a business to accept and process payments. While most people immediately think of credit card swiping, the category is much broader. It encompasses the hardware in your store, the checkout page on your website, and the invisible security protocols that keep data safe from hackers.

Every business that moves away from a cash-only model enters the world of merchant services. Modern consumers expect a frictionless experience, and digital payment tools are the next step. According to the Federal Reserve, card payments continue to climb, while cash payments for in-person transactions have seen a steady decline over the last decade. Without a reliable way to handle digital currency, a business essentially closes its doors to a massive segment of the population.

How Merchant Services Work

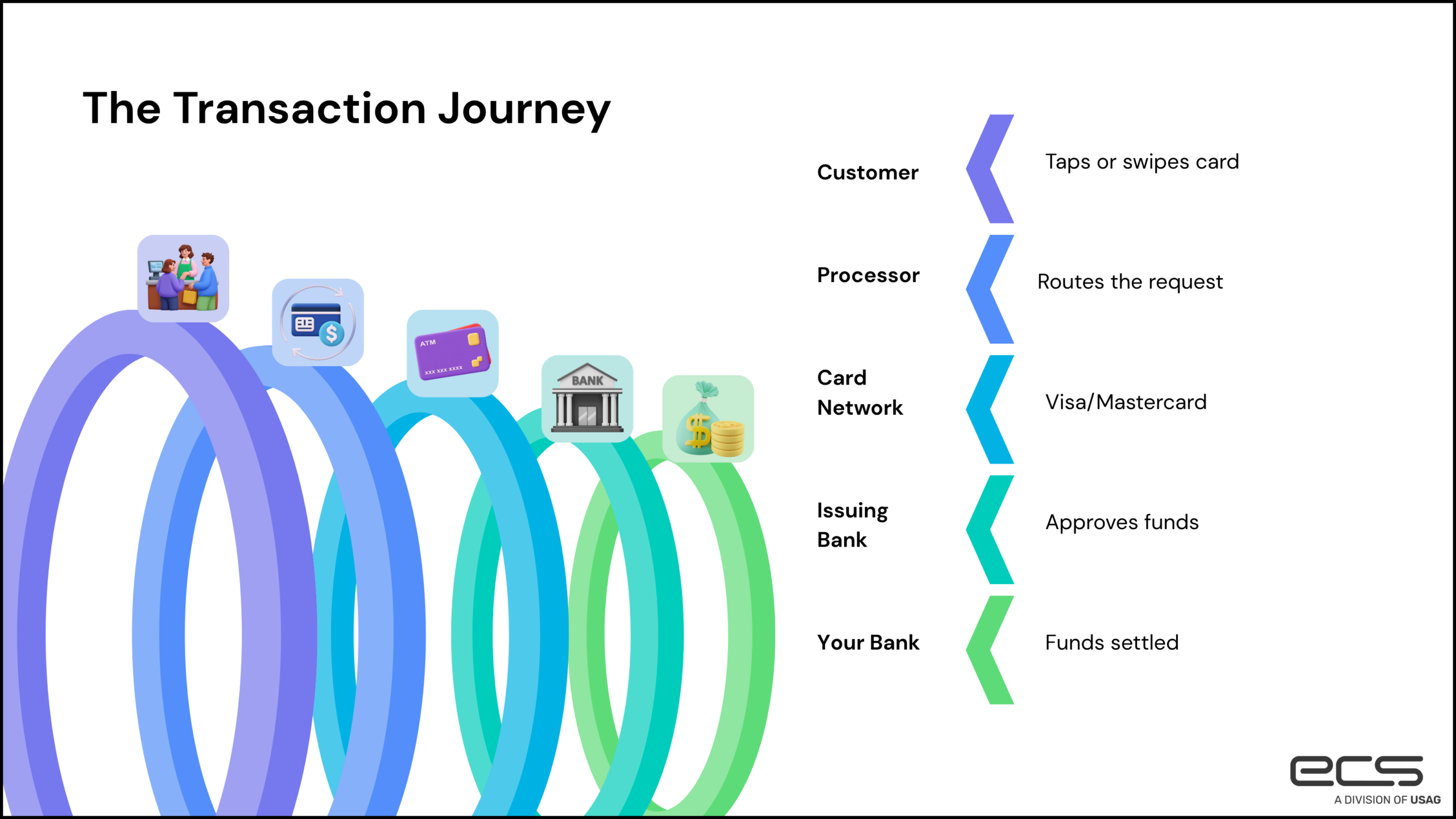

The journey of a single transaction happens in a matter of seconds, but it involves a complex relay race between several different financial entities. When a customer taps their card on your reader, a digital request for authorization begins.

The first stop is the payment processor. This is the company that acts as the technical messenger. They take the card data and send it to the card networks, such as Visa or Mastercard. These networks act as the bridge to the cardholder’s bank to verify that the funds are available and the card is legitimate.

Once the bank approves the sale, the message travels back through the network to your acquiring bank. This is the bank that holds your business account and ultimately receives the funds. While this seems like a lot of moving parts, a high-quality merchant services provider ensures that this entire loop completes instantly, so your customer is not left standing at the counter waiting for a dial-up connection to respond.

What Is Included in Merchant Services?

A comprehensive package usually includes several key components tailored to how you do business. It is rarely a one-size-fits-all situation.

Payment Processing

This is the core engine. It is the actual handling of the data transmission from the point of sale to the final settlement of funds in your bank account.

POS Systems

Point of Sale systems are the physical or digital hubs where the transaction occurs. Modern POS systems do much more than just take money. They often handle inventory tracking, employee timesheets, and even basic customer relationship management.

Payment Gateways

If you sell products online, you need a payment gateway. Think of this as a virtual terminal that encrypts sensitive credit card information and passes it from the customer’s browser to the processor. It is the digital equivalent of a physical card reader.

Fraud Tools

Security is a massive part of the value provided by a processor. This includes Address Verification Services (AVS), Card Verification Value (CVV) checks, and encryption standards like PCI compliance. Protecting your business from chargebacks is just as important as the sale itself.

Types of Merchant Services

Every business model has different requirements for how they interact with their customers. A brick-and-mortar boutique has very different needs than a subscription-based software company.

- In-store Processing: This relies on physical hardware like countertop terminals or mobile tablets. It emphasizes speed and physical security features like EMV chip technology.

- Online Processing: This focuses on website integration. It allows you to accept payments via an e-commerce storefront or through digital invoices sent via email.

- Mobile Solutions: For contractors, food trucks, or professionals on the move, mobile processing allows them to accept payments anywhere using a smartphone or tablet equipped with a small card reader.

- Recurring Billing: This is essential for gyms, subscription boxes, or utility companies. It automates the collection of payments on a set schedule, reducing the need to manually invoice clients every month.

What Is a Merchant Account?

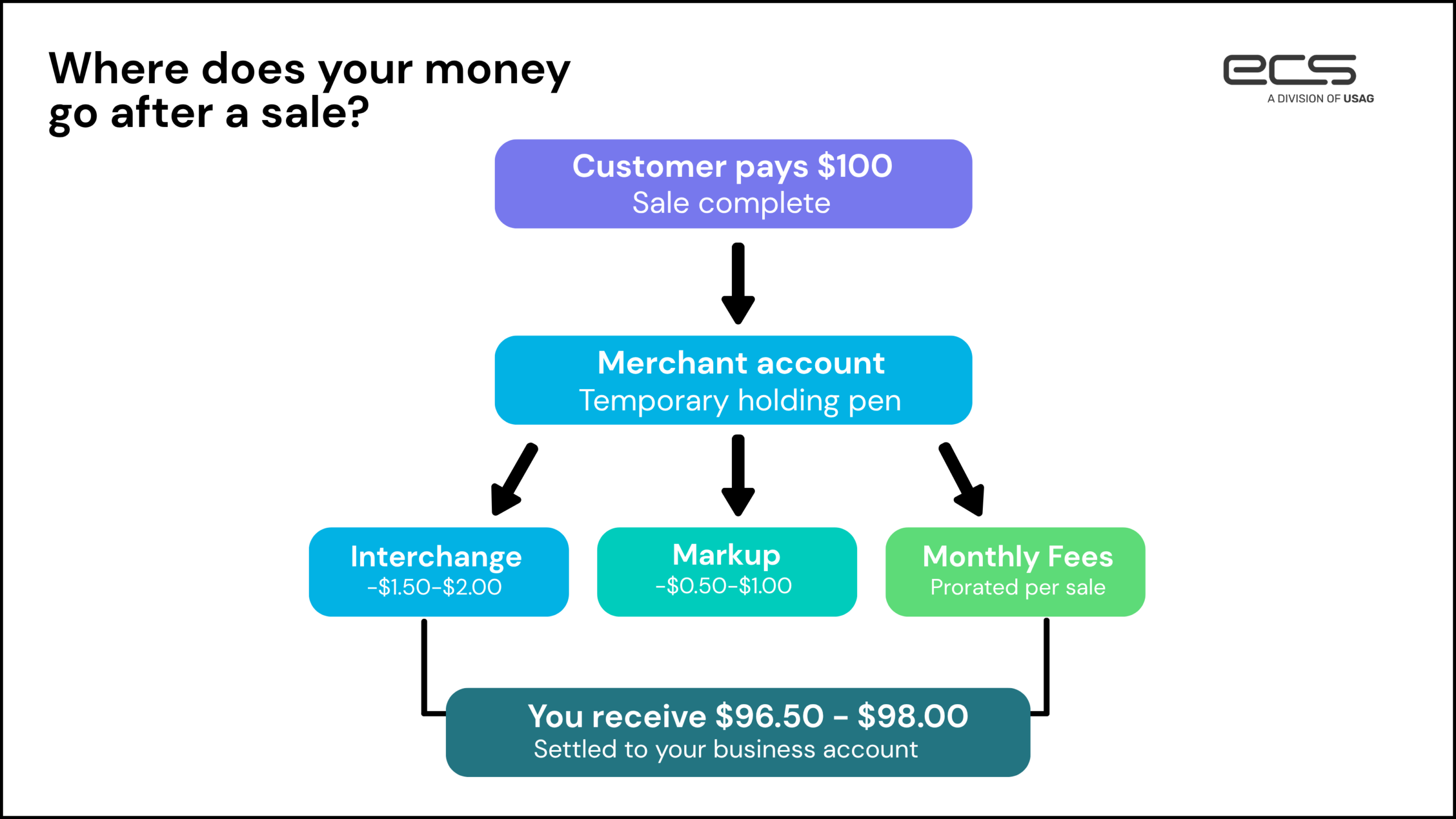

It is common to confuse a merchant account with your standard business checking account, but they serve different purposes. A merchant account is a specific type of bank account that allows you to accept credit and debit card payments. It acts as a temporary holding pen for your funds.

When a customer pays you, the money does not go straight to your business checking account. Instead, it sits in the merchant account while the transaction is cleared and the various fees are deducted. Once the process is finished, the remaining balance is settled into your actual bank account.

Choosing the right merchant account setup is vital for your cash flow. Some providers offer “aggregator” models where you share a large account with thousands of other businesses. This is fast to set up, but it can lead to sudden account freezes or delays. A dedicated merchant account provides more stability and is usually preferred for established businesses that want more control over their funds.

Merchant Services Fees Explained

Transparency in pricing is often the biggest pain point for business owners. To understand your bill, you have to look at the three main layers of costs.

The first layer is interchange. This is a non-negotiable fee set by the card networks like Visa and Mastercard. It goes directly to the bank that issued the customer’s card. These rates vary based on the type of card used and how the transaction was processed. For example, a rewards credit card usually costs more to process than a standard debit card.

The second layer is the markup. This is where your merchant services provider makes their money. This can be structured as a flat percentage per transaction, a monthly subscription, a “cost-plus” model, or a tiered structure.

Finally, there are monthly fees. These might include statement fees, PCI compliance fees, or hardware leases. The average cost of processing credit card transactions ranges from 1.5% to 4% per transaction. Being aware of these benchmarks helps you determine if your current provider is giving you a fair deal.

How to Choose a Merchant Services Provider

Selecting a partner to handle your revenue is a significant decision. You should look for a provider that prioritizes clarity over confusing sales jargon.

Pricing Transparency

A good provider will be happy to explain exactly where every penny is going. If a salesperson avoids discussing interchange-plus pricing or hides behind “tiered” pricing structures that make it impossible to see the actual costs, it might be a sign to look elsewhere.

Reliable Support

When your system goes down on a busy Saturday afternoon, you cannot afford to wait for a ticket response from an automated bot. You need access to human experts who understand the technical side of your specific setup.

Scalability

Your needs today will likely change as you grow. A provider should offer a variety of integrations and hardware options that can scale alongside your transaction volume. At ECS Payments, the focus is on providing that level of stability and expertise. Instead of offering a cookie-cutter solution, the approach is centered on understanding the unique friction points of a business.

Whether it is navigating the complexities of high-volume processing or ensuring that a small local shop has the most efficient POS system, the goal is to act as a long-term partner rather than just a vendor. By focusing on security and personalized service, ECS Payments helps merchants move past the confusion of payment processing so they can focus on their actual work.

Common Mistakes to Avoid

To better understand where businesses commonly go wrong, it helps to hear directly from someone in the field.

Hear from our very own merchant services representative, Trinity Lembeck:

Many business owners fall into traps that can be avoided with a little bit of due diligence. One of the most common issues is entering into long-term contracts with heavy liquidated damages clauses. If a provider is confident in their service, they should not need to lock you into a three-year ironclad agreement with massive exit fees.

Another mistake is ignoring hidden fees. Always ask for a full schedule of fees, including things like “batch header” fees or “annual maintenance” costs. These small charges can add up to hundreds of dollars over the course of a year.

Finally, many merchants fail to keep their security standards up to date. Maintaining PCI compliance is not just a suggestion. It is a requirement that protects you from massive fines in the event of a data breach. The PCI Security Standards Council provides extensive documentation on why these protections are necessary for every merchant, regardless of size.

Managing your payments does not have to be a source of constant stress. By understanding the mechanics of your merchant account and partnering with a payment provider that is transparent, you can turn your payment processing into a streamlined asset that supports your growth.

Professionalism, clarity, and a commitment to security are the hallmarks of a healthy merchant services relationship. Taking the time to evaluate your current setup today can lead to significant savings and a much smoother experience for your customers tomorrow.