With every card transaction, a small percentage of each sale vanishes within seconds. If you have spent any time reviewing your monthly merchant statement, you have likely felt frustrated by the sheer number of line items and acronyms cluttering the page. There are so many fees on a merchant statement, but interchange fees represent the single largest component of your processing costs. Without a clear grasp of how they work, you are effectively flying your business blind through a storm of hidden expenses.

What Are Interchange Fees?

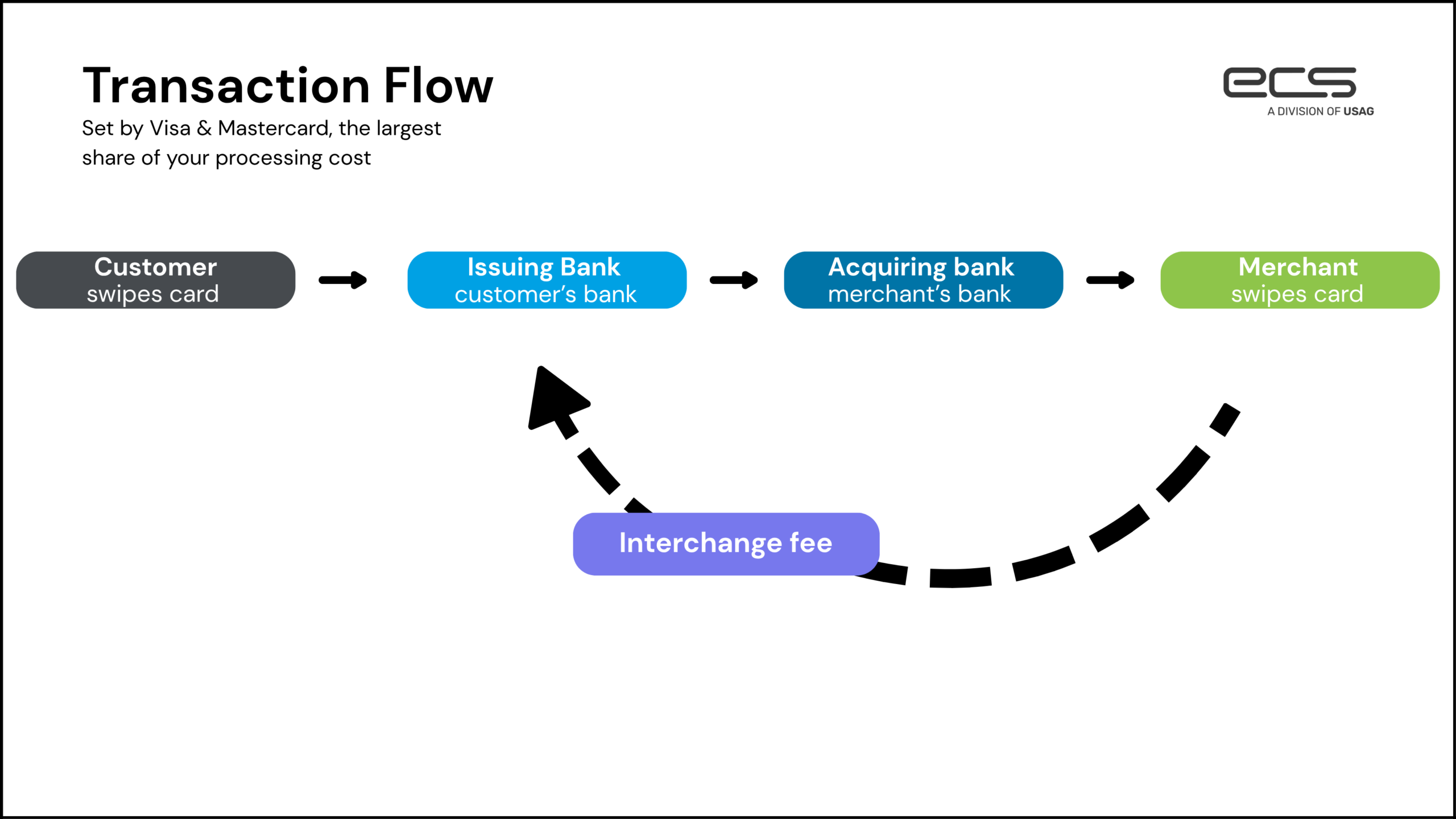

At its simplest, an interchange fee is the cost an acquiring bank pays to the card-issuing bank for each transaction. When a customer uses a Visa or Mastercard at your shop, your bank has to compensate the customer’s bank for the risk and the labor involved in moving that money. While people often blame their payment processor for high costs, the processor actually has very little control over the interchange rate itself. These rates are set by the card networks like Visa and Mastercard, and are usually updated twice a year. You can check out the 2026 fees below:

The revenue generated from these fees covers the costs of managing cards and everything that comes with them: fraud prevention, the interest-free grace period provided to cardholders, and the massive infrastructure required to maintain global payment networks.

The average interchange fee for debit cards can vary significantly depending on whether specific federal regulations cover the issuer. This distinction alone highlights why your monthly statement can look so inconsistent. It is not a flat tax, but rather a shifting landscape of variables that change based on the specific plastic your customer carries in their wallet.

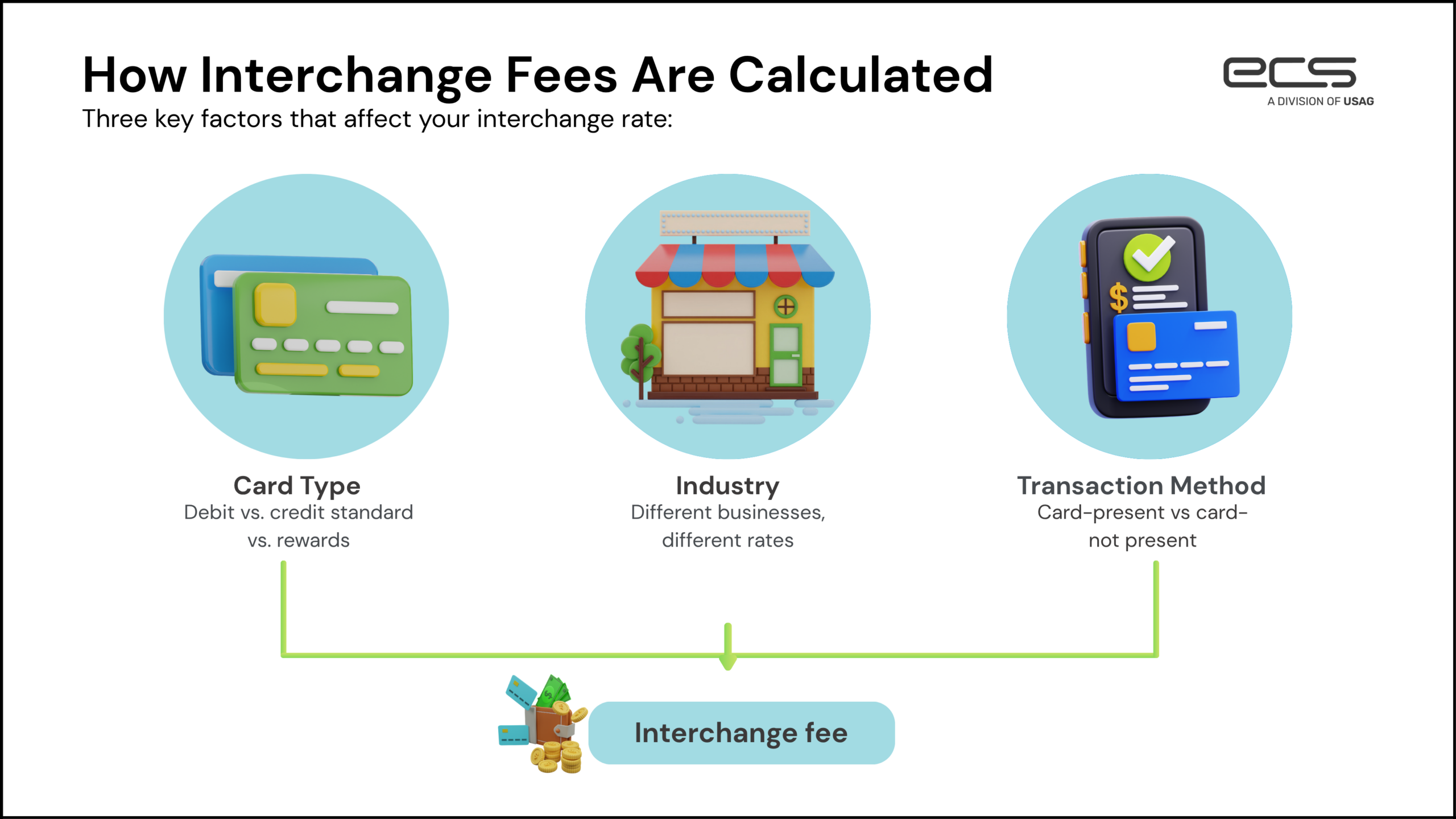

How Interchange Fees Are Calculated

Trying to pinpoint a single rate for your business is nearly impossible because there are hundreds of different interchange levels. The card networks use several data points to determine which bucket your transaction falls into. If you do not meet the strict criteria for a lower rate, the transaction “downgrades,” and you end up paying a much higher price for that same sale.

Card Type

The merchants essentially fund the rewards programs that customers love. A basic “vanilla” debit card carries much lower risk and no reward overhead, so it features some of the lowest rates available. Conversely, a high-tier rewards credit card or a corporate purchasing card will trigger much higher credit card interchange fees. When your customer gets 2% cash back or airline miles on their purchase, you are the one paying the higher interchange rate.

Industry

The type of business you run plays a massive role in your pricing. Card networks assign Merchant Category Codes to every business. A grocery store or a gas station typically operates on thin margins and sees high volume, so they often qualify for specialized, lower rates. On the other hand, a high-end jewelry store or a digital consulting firm might see higher base rates because the perceived risk of chargebacks or fraud in those sectors is statistically higher.

Transaction Method

How the card data enters your system is perhaps the most controllable variable in this equation. A “card-present” transaction, where the chip is dipped or the phone is tapped, is considered very secure. Because the physical card was there, the risk of fraud is low. If you take that same card number over the phone or through an online portal, it becomes a “card-not-present” transaction. The lack of a physical security check means the interchange rate jumps significantly to compensate for that added risk.

Interchange Categories Explained

To make sense of interchange rates, you have to look at the categories. The networks group transactions into buckets such as Retail, Restaurant, E-commerce, and Public Sector. Each of these has its own rules regarding how much data must accompany the transaction.

For instance, business-to-business transactions often require “Level 2” or “Level 3” data. This includes details like tax amounts and invoice numbers. If you provide this extra information, the card networks reward you with a lower interchange rate. If you leave those fields blank, the transaction defaults to a more expensive category. It is a system designed to reward transparency and security, but it often punishes businesses that use outdated hardware or software that cannot transmit this extra data.

How Interchange Impacts Your Costs

Interchange is the “wholesale” cost of credit card processing. Everything else you pay, such as the processor’s markup and the network assessment fees, sits on top. This is why many savvy business owners prefer an “Interchange Plus” pricing model. In this setup, the processor passes the raw interchange cost directly to you and adds a small, transparent fee.

If you are on a “Flat Rate” or “Tiered” plan, you usually pay a single high price to cover all card types. While this feels simpler, you are overpaying for low-cost debit transactions and possibly saving money on corporate or elite rewards credit card transactions. The total processing costs usually range between 1.5% and 4% per transaction. When you realize that the majority of that percentage is the interchange fee, you can see why even a fractional change in your rate can save thousands of dollars for the year.

Hear more from our Referral Partner Manager, Abe Berg, on the difference between an interchange fee and a flat rate:

How to Optimize for Lower Interchange Rates

While you cannot call up Visa and negotiate a better rate, you can change your behavior to qualify for the best existing rates. The first step is ensuring you are using the most secure technology available. Using EMV chip readers for every face-to-face transaction is the bare minimum. If you are keying transactions manually, consider using a secure “Card on File” vault or a pay-by-link system that lets customers enter their own data securely.

For those in the B2B space, data is your best friend. Implementing a system that automatically populates Level 2 and Level 3 data can slash your corporate card transaction costs by a significant margin. Additionally, you should keep an eye on your settlement timing. Most interchange categories require you to settle your “batch” within 24 to 48 hours. If you wait too long to close out your daily sales, the transactions can expire from their lower-cost categories and settle at a much higher “Standard” rate.

Common Misconceptions

One of the most frequent mistakes business owners make is thinking that all processors have different interchange rates. In reality, the interchange schedule is public and identical across all processors. If a salesperson tells you they have a “special deal” with Mastercard to get a lower interchange, they are not being honest with you. The difference between processors lies in how they pass those costs to you and whether they help you optimize your setup to avoid unnecessary downgrades.

Another misconception is that debit cards always cost the same. Following the Durbin Amendment, interchange for debit cards issued by large banks is capped. However, cards from smaller “non-exempt” banks can still carry higher rates.

These fees continue to evolve as consumer behavior shifts toward mobile wallets and contactless payments. It is a moving target, which is why having a partner who understands these nuances is vital.

Partnering with ECS Payments

At ECS Payments, we believe that transparency is the only way to build a lasting business relationship. Our approach is rooted in education and optimization for our merchants. We work to identify where transactions are downgrading and why. Whether that means upgrading your point-of-sale hardware to support the latest security protocols or configuring your gateway to pass Level 3 data for your corporate clients, we focus on the details that affect your bottom line. We also offer the tools and the personal support needed to ensure your processing setup is as efficient and cost-effective as possible.

By choosing a partner that prioritizes your understanding of the industry, you move from being a passive payer of fees to an active manager of your business expenses.

If you are ready for a deeper look at your statement, reach out to ECS Payments today for a comprehensive review of your current rates. Let us help you find a clearer path to savings. We can help you break down your costs and implement the strategies needed to keep more of your hard-earned revenue.