The moment a customer asks, “Can I pay over the phone?” your business enters a different category of risk. If you aren’t prepared to handle that request securely, you are effectively leaving money on the table or, worse, scribbling credit card numbers on sticky notes that pose a massive security threat. This is where the virtual terminal becomes an essential bridge between traditional retail and the modern, remote economy.

What Is a Virtual Terminal?

To put it simply, a virtual terminal is a web based application that allows a merchant to accept payments without the customer being physically present and without needing to swipe or dip a plastic card. It essentially turns your computer, tablet, or smartphone into a credit card machine. Instead of using hardware to read a chip, you log in to a secure portal provided by your merchant services provider and enter the customer’s payment details manually.

This method is often referred to as keyed in payment processing. It is the backbone of any business that takes orders via telephone, mail, or email. While a physical terminal at a checkout counter relies on a hardware connection to transmit data, an online virtual terminal payments system uses your internet browser to send that information through a secure gateway. This makes it a perfect fit for law firms, freelancers, wholesalers, and any service based business where the “checkout” happens in a home office or a professional suite rather than a storefront.

How to Use a Virtual Terminal

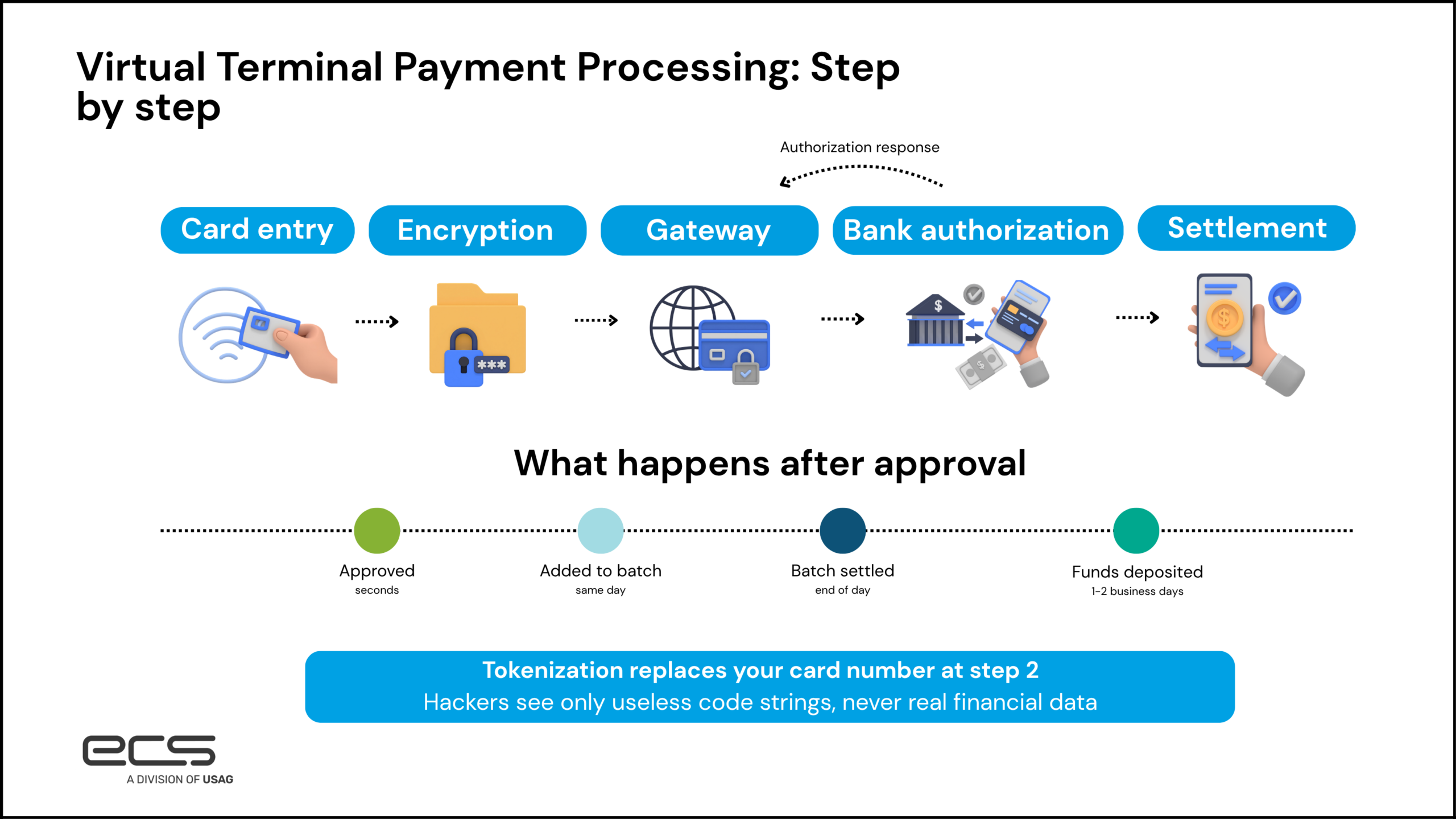

Virtual terminal payment processing is straightforward but involves several layers of digital handshaking to ensure the funds actually move from the buyer to your bank account. When you open your terminal, enter the transaction amount, the customer’s card number, the expiration date, and the security code from the back of the card. Most professional setups will also ask for the billing zip code and street address to perform an Address Verification Service check.

Once you click the submit button, the virtual terminal sends the encrypted data to the payment gateway. The gateway then communicates with the card issuing bank to verify that the account is valid and has sufficient funds. This authorization happens in seconds. If approved, the transaction sits in a “batch” until the end of the day. During the settlement process, your payment processor gathers all the day’s approved transactions and sends them through the networks to initiate the transfer of funds into your merchant account.

Key Features of a Modern Virtual Terminal

Security is the primary feature of any legitimate payment virtual terminal. Because you are handling sensitive data, the software must be PCI compliant. Modern solutions use tokenization, which is a process that replaces the actual card number with a unique digital identifier. This means that if your system were ever compromised, hackers would find useless strings of code rather than actual financial data. This technology is vital for protecting both your reputation and your customers’ bank accounts.

Beyond basic security, you should look for the ability to create customer profiles. If you have a client who pays you every month, typing in their sixteen digit card number every single time is an inefficient use of your workday.

A quality system enables you to store those payment methods for future use securely. Additionally, robust reporting tools are necessary to view your transaction history in real time. You want a system that integrates with your existing invoicing or CRM software so that when a payment is made in the terminal, your accounting records update automatically.

Benefits of Using a Virtual Terminal

The most immediate advantage of using a merchant services virtual terminal is the total elimination of expensive hardware. You don’t need to lease a countertop machine or buy a mobile card reader that might break or lose its Bluetooth connection. As long as you have a device with a web browser and a stable internet connection, you can accept a payment. This flexibility is a game changer for remote teams or businesses that operate across multiple locations but want to centralize their finances.

Traditional card-swiping is fading as over 50% of the population embraces digital and remote payment methods. The charge is led by Gen Z (78%) and Millennials (75%), who overwhelmingly prefer these digital-first solutions.

Having a virtual terminal for businesses ensures you can meet these customers where they are. It also simplifies your management process. Instead of checking three different machines for your daily totals, you can log into one dashboard and see everything at a glance.

Common Limitations of Basic Virtual Terminals

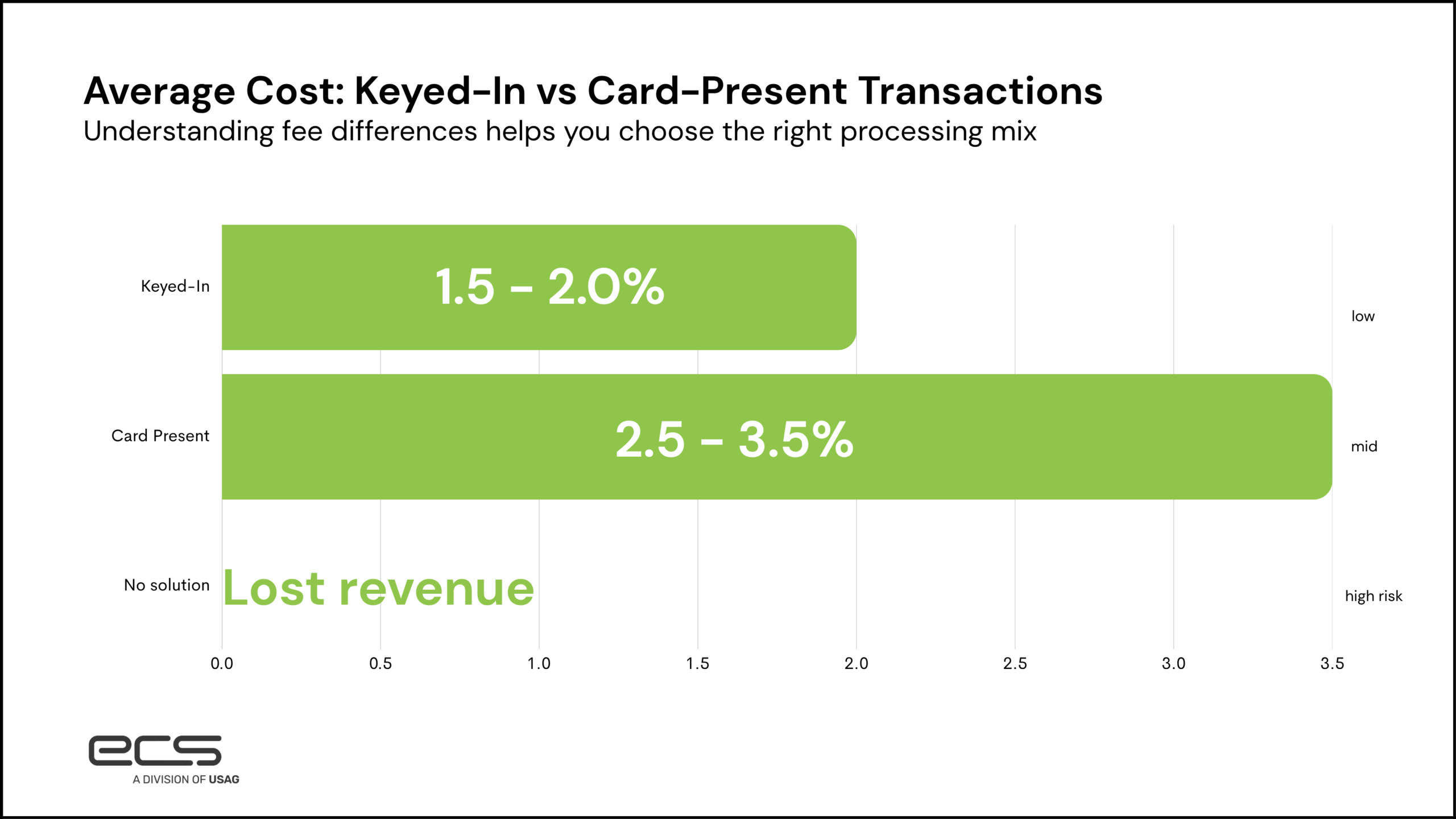

While the convenience is high, there are some trade offs to consider. The most notable limitation is the pricing structure. Keyed transactions generally incur higher processing fees than “card present” transactions. This is because the risk of fraud is statistically higher when a card isn’t physically scanned. Banks charge higher fees to offset the potential costs of unauthorized transactions.

There is also the human element to consider. Manual data entry is prone to typos. A single incorrect digit in a credit card number or a mistyped billing address can result in a declined transaction or a future chargeback. If your business processes hundreds of orders a day, relying solely on a virtual terminal can become a bottleneck because entering every detail takes time.

How to Improve Virtual Terminal Payment Workflows

To get the most out of your setup, you should lean heavily on tokenization and saved profiles. By reducing the number of times your staff has to enter a card number manually, you reduce the margin for error. You should also make it a habit to collect as much data as possible during the entry process. Including the CVV code and the full billing address is important for security, but it can also help you qualify for lower interchange rates–depending on your processor’s specific rules.

Integrating your terminal with digital invoicing is another way to optimize your workflow. Instead of you typing in the details, you can send an invoice with a link that allows the customer to enter their own information. This shifts the data entry task to the customer, reducing your liability. When you do have to use the virtual terminal yourself, ensure your team is trained to verify the information back to the customer before hitting the submit button.

When to Consider Alternative Payment Solutions

If you find that your team is spending hours every day tied to the computer typing in card numbers, you might have outgrown a standard virtual terminal. High volume businesses often reach a point where manual entry becomes a liability rather than an asset. If your chargeback rate is creeping up or you are struggling to keep up with recurring billing cycles, it is time to consider more automated systems.

Merchants across the country remain on high alert as card-not-present (CNP) fraud continues to evolve. Criminals are finding increasingly sophisticated ways to harvest personal data, with massive data breaches serving as a primary catalyst. A prime example is the “Mother of All Breaches,” that occurred in 2024. This breach leaked 12 terabytes of data; 26 billion records from major platforms like LinkedIn, Adobe, and Canva.

Beyond digital hacks, physical card skimming is seeing a dangerous resurgence. In 2024 alone, card compromise events in the U.S. rose by 8%, affecting over 3,300 financial institutions. This method is particularly devastating in the American market, where the FBI estimates that skimming costs banks and consumers approximately $1 billion every year.

If your business model involves a high volume of these transactions, relying on a basic, non-integrated terminal might be costing you more than you realize in both time and security risks.

Alternative Payment Solutions to Consider

One of the most effective alternatives to virtual terminal payments is a dedicated online payment portal. This allows your customers to log into a secure area on your website to manage their own payments. It provides a better user experience and keeps your staff focused on other tasks. For businesses that operate on a subscription model, a recurring billing system is superior because it automates the entire process and sends out notifications when a card is about to expire.

Mobile payment processing is another strong contender if you ever meet clients in person. Using a small card reader attached to a phone or tablet lets you take advantage of lower “card present” rates while still maintaining the portability of a virtual terminal. Finally, integrated payment solutions built into your industry specific software can bridge the gap between sales and accounting.

How Virtual Terminals Fit into a Broader Payment Strategy

A virtual terminal shouldn’t be your only way to take payments, but it is an essential part of a larger merchant services strategy. It acts as your safety net. If your physical terminal breaks, or if a customer forgets their wallet but has their card number saved on their phone, the virtual terminal saves the sale. It works best when paired with other methods, such as a standard POS system or an eCommerce storefront.

By creating a unified payment ecosystem, you ensure that no matter how a customer wants to pay, you have a secure way to accommodate them. This level of flexibility is what separates professional operations from amateur ones. It allows you to maintain a consistent cash flow even when your primary sales channel is interrupted.

How to Choose the Right Virtual Terminal Solution

When you are evaluating providers, look closely at their security credentials. They should be at the forefront of PCI compliance and offer clear documentation on how they protect your data. Ease of use is the next priority. The interface should be intuitive enough that a new employee can learn it in minutes. If the layout is cluttered or confusing, the likelihood of data entry errors increases significantly.

You also need to consider how the terminal will grow with you. Does the provider offer integration with the software you already use? What is their pricing structure for keyed in transactions? Transparency is key. You want a partner who explains fees clearly, not one who hides them in complex contracts.

ECS Payments: A Reliable Partner in Merchant Services

At ECS Payments, we understand that a virtual terminal is a vital tool for business continuity and customer service. We focus on providing a secure, streamlined experience that lets business owners focus on their growth rather than on processing hurdles. Our technology is designed to be both powerful and accessible, providing you with the reporting and security features often reserved for much larger corporations.

Hear from our Technical Support Manager, Sebastian Perry, on what the setup process looks like when switching to ECS terminals.

Our approach centers on building a relationship with our merchants. We provide the tools you need to handle keyed in payments safely while also offering the scalability to move into more advanced payment integrations as your business evolves. Whether you are taking your first phone order or managing a complex remote billing cycle, we ensure that your payment infrastructure is the strongest part of your business.

Next Steps

A virtual terminal is a powerful tool for handling remote transactions. But it is important to evaluate it as part of your total financial picture. If you find yourself relying on manual entry for the majority of your sales, it may be worth investigating how more automated solutions can save you money on processing fees and reduce your administrative burden.

Take a moment to look at your current payment workflows. Are your employees spending too much time on the phone taking card details? Is your sensitive customer data truly secure? If you feel like your current setup is falling behind, it might be time to upgrade your virtual terminal. One that is a more robust, integrated solution. Assessing these needs now will prevent headaches as your volume increases. Reach out to a professional who can help you map out a complete payment strategy that protects your revenue and provides the convenience your customers expect.

Maintaining healthy cash flow is one of the most critical factors in business longevity. Choosing the right payment tools is the most direct way to ensure that your cash flow remains uninterrupted and secure.