Looking for a new merchant service provider for your business? You’ve got to ask the right questions to find the right payment processor. Think of your search for sale (POS) systems a little bit like dating. You don’t necessarily want to marry someone on the first date, even if Elvis Presley does the honors at a drive-thru chapel in Vegas.

Rather, you want to get to know the person before entering a committed contractual relationship. And in many ways, that’s what you do when looking for business banking services. Before signing a contract, you want to ask all the right questions.

Thankfully, we’ve compiled a list of key features of payment processors and what to ask about.

1. What Are Your Fees and Pricing Models?

A business must ask a potential payment processor about fees and pricing models. Mainly, there are three types of typical pricing models: flat rate, tiered, and interchange plus.

You need to ask this question because, in reality, the true cost of every transaction is different. It depends on the type of card used, the card network, and your business’s MCC (merchant category code).

An MCC is assigned by issuing banks and/or card networks to describe your primary business activity as indicated by sales volume. The MCCs for gambling, online dating, and supplement businesses have some of the highest fees around due to risks associated with the industry. If your business does not fall into any of those categories (for example), why should you pay the same rate per transaction?

Flat Rate Pricing

But that’s essentially what flat rate pricing does. Flat rate pricing is great for startup businesses because it’s so straightforward. But if you’re being charged 2.6% + ten cents for every transaction, you should ask why.

Tiered Pricing

Another pricing scheme that initially seems better is tiered pricing. “Seems” is the operative word. In reality, tiered pricing schemes present a different problem, and that is favoring the payment processor over the merchant (you).

There are often 3 tiers in tiered pricing: qualified, mid qualified, and non qualified. These tiers are often categorized by which cards present more or less “risk.” Debit cards (which are directly linked to bank accounts where funds can be verified immediately) fall into the qualified category. In contrast, high rewards credit cards and business cards may be considered “non-qualified.”

The problem with this pricing model is that all the cards that bring you the biggest orders are penalized the most. For instance, business credit cards will undoubtedly be used for larger purchases—but with tiered pricing, you will be hit with the highest fees for taking them.

Tiered pricing is really about hedging the risk for the payment processor. It’s often used by banks that also offer credit card processing services. Banks are well known for conservative financial strategies that skew towards risk aversion. However, this pricing model does not benefit the merchant.

Interchange Plus Pricing

Ask your potential payment processor if they offer interchange plus pricing. This pricing model is the most transparent, as you’ll be charged the actual true cost of running a transaction (the interchange) plus a markup fee (the plus) for the processor.

Do not be embarrassed to ask for a full and comprehensive schedule of fees from the payment processor. Ask about all their fees. You should review the fee schedule carefully to see if additional transaction fees apply.

However, flat rate and tiered pricing are great ways for payment processors to hide additional costs from you behind a lack of transparency.

2. What Payment Methods Do You Support?

The right merchant service provider for your business should be able to supply all the payment methods you need. Ask what payment methods a payment processor can support. Obviously, you want to accept as many credit cards and debit cards as you can. But these days, there are also different ways to make a credit or debit card payment.

There are EMV chips, contactless cards, and mobile wallets, to name a few. Consumers are increasingly relying on contactless mobile wallets to make payments. If you take payments at a physical POS terminal, not accepting these payments could create a negative customer perception and even cause you to lose business.

You’ll notice we did not mention magnetic strips. These will be disappearing entirely from credit cards within a few years. That said, you do not want to be saddled with antiquated payment hardware (more on that later). Rather, you want a payment processor that is current on the latest payment trends.

One of those payment trends is installment payments or point-of-sale loans. For B2C sales, this means applications like Klarna, Affirm, or Afterpay. This BNPL fintech (buy now, pay later) can boost sales volume by 27% while increasing average order size by 87%.

However, these benefits can come at a big cost to merchants. The aforementioned companies can charge up to 6% per transaction, which is ridiculously steep. When asking if a payment processor can offer BNPL as a payment method, also ask how much they (or their partner lender) charge.

3. Is the Payment Processing System Secure?

Next, it’s time to ask about security. The right merchant service provider for your business should make you and your customers feel that every transaction is secure. What policies and procedures does your potential payment processor have to foil fraud? Ask about specific security certifications, like the PCI DSS data security standard.

Payment Card Industry Data Security Standards (PCI DSS) are a set of 12 guiding principles established by Visa and MasterCard. The core objective of PCI DSS is to minimize the risk of compromising sensitive cardholder information, such as stored credit card numbers.

This is particularly relevant if you have a subscription based business model or allow customers to create accounts to expedite future purchases. You cannot simply store card numbers among your other intangible assets.

Rather, card numbers must be encrypted and/or tokenized. In simple terms, this means scrambling the numbers with a cipher that can only be decrypted by the payment processor. While they probably can’t explain all the details to you, the payment processor should be able to explain, in broad strokes, how they adhere to PCI rules, such as encrypting cardholder data.

They should also offer disaster recovery and business continuity plans for your review. These show that a payment processor responsibly anticipates worst case scenarios and has a plan to quickly get things back on track.

Ask about what robust and proactive security measures they use while accepting credit card payments, such as the latest developments in machine learning fraud prevention.

Routine maintenance of security systems can also disrupt business continuity. Ask what their guaranteed system uptime is; the percentage of time all systems are functioning. Ask if there is any compensation for extended periods of system downtime as security issues are dealt with or routine maintenance is conducted on the system.

4. How Are Chargebacks and Disputes Handled?

Chargebacks are disputes that the customer takes to their bank or credit card issuer instead of appealing to you. Since there are several parties involved in processing a payment, reversing that process can create a cascade of fees that ultimately land on the merchant: you.

Unfortunately, chargebacks are becoming an increasingly prevalent problem. Part of this problem is a payment landscape that heavily favors consumer protections; a sort of rebound from the predatory lending climate that existed before 2008.

As consumers see how easy it is to file a dispute, the cost of “friendly fraud” is rising. Some studies suggest as much as 40%. Certain industries like eCommerce are particularly susceptible to friendly fraud.

Therefore, another important consideration you should ask to find the right merchant service provider for your business is how they will handle chargebacks and disputes. How proactive will they be about reaching out to you to get your side of the story? What type of documentation will they require?

Usually, chargebacks are “prosecuted” by the customer’s bank. Overall, you want to assess if the payment processor will “go to bat” for you or if they will just do their bare minimum.

5. What is the Contract Length and Cancellation Policy?

Make sure you understand the contract length and cancellation policy of the merchant service provider for your business. Are there any penalties or fees for ending the arrangement early? Will you automatically be enrolled in a new contract? Take note of the date that happens so you can approach the payment processor to negotiate better terms in the coming year.

Along with early termination fees, this is also the space to discuss other contractual fees, such as setup fees for hardware or software. It never hurts to have a retainer relationship with a lawyer who can examine your business contracts and raise any red flags.

6. What Hardware and Software Do You Provide?

Let’s return to the hardware that we mentioned above. Will the payment processor include free hardware as part of the contract? Will they require you to purchase hardware? Do they offer lease agreements?

Payment technology is rapidly changing and accelerating. For these reasons, a lease agreement might be the most beneficial. It will allow you to have the hardware you need and not be stuck with it when payment technology changes. Alternatively, you can ask if the processor has some sort of trade in program if you purchase the hardware outright and it becomes obsolete.

Servicing and maintenance are also big concerns. What type of service contracts does the payment processor offer? What are the terms and limitations of these service calls? How quickly can they respond to problems with your hardware by sending out a tech or engineer?

Thinking forward, it is also ideal to work with a payment processor who is ahead of the curve. Exciting developments are underway and payment processing, such as biometric payments. MasterCard, Visa, and Amazon have already rolled out facial and hand scan technology for in store payments.

Is this something your payment process or could potentially keep up with? What about crypto payments? Then there is the software. Will the software integrate with some business systems you already use, such as CRM, ERM, inventory management, and accounting? Integrated payment solutions automate and streamline accounting practices, saving you tons of money and/or payroll hours.

7. How Reliable is Customer Support?

We have already touched upon how important it is for the payment processor to be responsive several times. Large payment aggregators like Stripe and Square have notoriously bad customer service. If something goes wrong, your only way of communicating could be through a chat or email exchange, where responses take 24 hours. And what happens if there’s an adverse event on the weekend?

The right merchant service provider for your business will be available when you need them. Ask your payment processor about the availability of support, and how that support is conducted. The most ideal situation is one in which you are assigned a unique relationship with an account manager. This individual becomes a point person for resolving issues as they come up. In addition to the account manager, what type of ongoing 24/7 support does your payment processor have?

8. What Are the Settlement Times?

How long does it take for funds to settle? Is there any variability based on the type of transaction? Does the payment processor offer same day, next day, or batch settlements? Are there any options to accelerate settlements as needed?

Does transaction volume impact settlement times? This is especially important for seasonal businesses to consider. You should be aware if high transaction volumes can negatively impact settlement times.

Settlement times are also important for businesses with low cash volumes and large ticket sales. Some service based businesses, for example, may only run a few transactions a week or even per month. If funds are delayed, this can cause serious problems with other departments like accounts payable and payroll.

9. Do You Offer Customization for My Business Needs?

Does your business have any unique needs that particular customizations would serve? A business’s unique needs can impact the software and hardware used.

For instance, a fleet based business would greatly benefit from mobile payment solutions. Fintech applications today can turn a mobile phone into a contactless payment terminal. Can your payment processor offer this type of innovative, cloud based solution so that all your contractors can easily take customer payments on the job?

Does your business have any legal or regulatory concerns associated with collecting payments or paying vendors? Are there any tax considerations?

E-commerce is one area where the need for customization is readily apparent. For instance, eCommerce businesses may sell certain items that are prohibited in some states (e.g., shipped wine or CBD products). Such merchants should ask how a payment processor can facilitate transactions within the realms of legality and compliance, such as checking locations or using proxy piercing to ensure that customers are legally placing online orders.

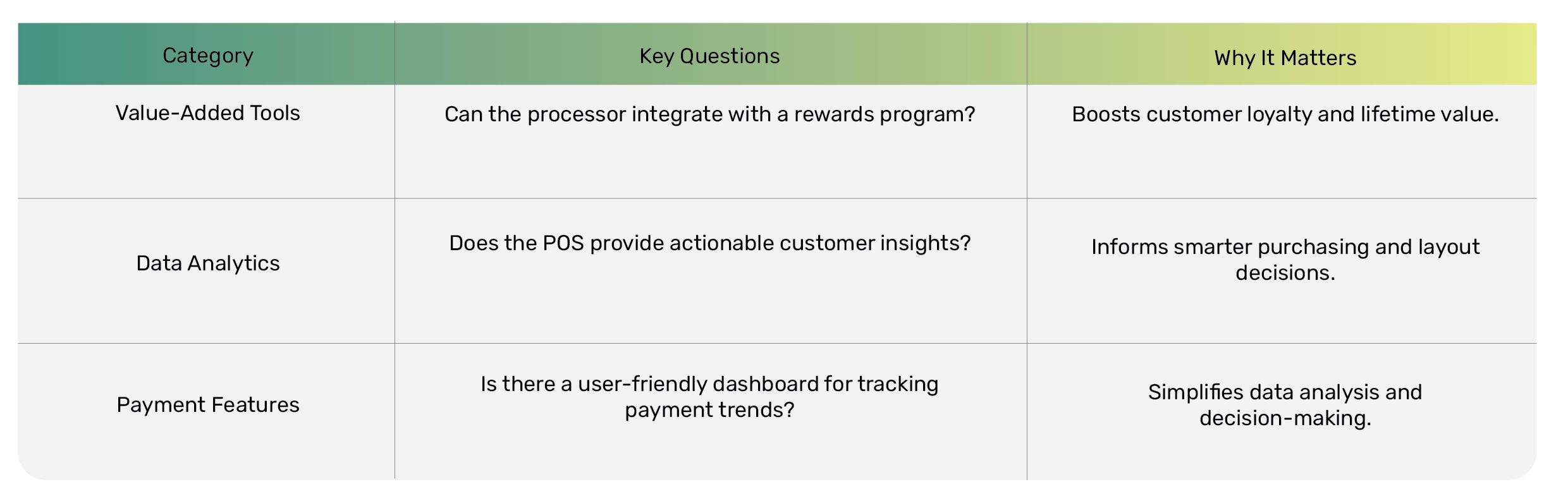

10. Are There Any Additional Features or Tools?

Ask what value added tools your payment processor can offer and integrate with industry specific tools you need. These bells and whistles are overlooked but important merchant service provider benefits.

Can they facilitate or integrate with a customer rewards program? If you don’t have one already, studies have shown that loyalty rewards programs are excellent for reducing churn and increasing customer lifetime value.

What about analytics? The point of sale is an incredible “observation post” for gathering significant quantities of customer data. You can see what items people are buying, when, and what they are buying together. This data can, in turn, be used to inform purchasing decisions or even determine the layout of a store or website.

As mentioned, the key to unlocking these huge troves of data is the online payment gateway or in store POS terminal. Does your payment processor offer a robust but easy to read dashboard for deciphering the ongoing stream of customer payments? Can it offer any specific customization to access data that is particularly relevant to your industry?

11. What Do Current Customers Say About Your Services?

What are current customers saying about the payment processing company? You can always go to sites like Google, TrustPilot, or the Better Business Bureau. If a payment processor is not BBB certified, find out why; are they just trying to avoid the fee, or did they receive too many complaints?

Speaking of complaints, see how the company responds to negative reviews on the aforementioned sites and others such as Facebook. You can also check LinkedIn for endorsements from business owners and C-level executives.

Companies that are serious about their marketing efforts will also compile testimonials and appealingly package them. These stories create an engaging narrative showcasing the payment processor’s capabilities for meeting expectations in all the areas outlined above. Ask the payment processor for success stories to see if they are serious about creating a good impression.

Also, ask if they can point to specific metrics, such as how implementing their solution increases sales, revenue, or profitability. Since they have significant amounts of data at their disposal, there is a good chance they are willing to showcase these metrics when they are trending positively.

12. Why Should I Choose Your Company Over Competitors?

This question, in many ways, summarizes all the questions we’ve asked above. What sets this payment processor apart from the others? According to some estimates, there are over 3,500 ISOs (Independence Day sales organizations) offering payment processing services. Your payment processor should have a compelling answer as to why you should choose them over the other 3,499 options.

Conclusion

Conducting a merchant service provider evaluation depends on asking the right questions. Questions for merchant services should include fees for debit and credit card transactions and the types of payments the processing solution can accept: card, mobile, crypto, and perhaps even biometric.

Evaluating payment processing companies must include how they handle disputes and their chargeback fees. You’ll need to know what type of hardware they offer, the point of sale (POS) terminals, and what software. Can the software integrate with the ones you currently use for business operations like CRM and ERP?

Beyond the cost of merchant services, a payment processor comparison must also assess merchant service contract terms and the reliability of payment processors. Do they offer strong security in payment processing? Do they have responsive customer service?

Finding the best merchant services for your business also depends on customization, compliance, and scalability. A good merchant service provider for small businesses will be familiar with its clients’ industries and unique business process needs.

When choosing a payment processor, don’t be afraid to go down your merchant account provider checklist and ensure you receive satisfactory answers. This relationship will be at the core of your cash flow and needs to feel right.