An economy is an ever-fluctuating machine driven by supply and demand, market spending, available credit, and external financial forces. Throughout the years, the world has experienced many seasons of prosperity, inflation, and recession. The question in today’s uncertain times is how does a recession affect the economy?

Gaining a better understanding of how recessions affect you and your business ensures you are well-equipped for your financial future.

What is a Recession?

The United States National Bureau of Economic Research (NBER) uses a mix of factors to determine the state of the economy. Such factors may include unemployment, wages, and spending behaviors.

A recession is a significant contraction or negative growth in economic activity. The decline in the gross domestic product (GDP) usually lasts longer than two consecutive quarters.

Supply and demand drive the economy. In short, recessions are when there is a lack of demand and an overage of supply. Resulting in unimpressive consequences that we will outline later on.

The economy is a constant cycle. A chain reaction, a cause-and-effect. The best way to picture the economy is like a yo-yo. It falls, there’s tension, it springs back up, there’s a lack of stability at the top, it falls again, and so forth.

Recessions are natural and happen from time to time. However, it doesn’t make them any less forgiving, let alone desirable. Though the policies put in place that lead to recessions aim at providing relief from inflation rate hikes, cost of living, and employment crisis, the result could be catastrophic.

What Causes a Recession?

A significant decrease in demand and spending initiates a recession. Limited demand results in a drop in business revenue. When businesses become less profitable, they will need to make adjustments to remain afloat.

This may mean that wages and employment are at risk. With an increase in unemployment, households then cut back on spending, prices continue to decrease, and thus, profits moreover. This all contributes to disrupting the market flow further and continues the recession symptoms.

Why Does Demand Decrease?

So what causes demand to decrease in the first place? There are a multitude of factors that may contribute to the decrease in consumer demand. Such factors may include:

Increased interest rates– This is the central bank’s response to fighting inflation. Increased interest rates cool down the market and make money less available to borrow. Less available funds equal less spending. Less spending means less demand. Less demand creates deflationary prices.

Increased unemployment – unemployment can be a result of a recession, but it also prolongs recessionary symptoms. When households have no income, they have no means for efficient spending.

Economic shock– This shock can be any unpredictable event that leads to expansive economic disruption. This may include a natural disaster, terrorist attack, pandemic, and so on.

The Recession Cycle

According to the NBER, the United States has experienced 34 recessions since 1857. These recessions have varied in length from a few months to over five years. The average recession persists for about a year and a half.

The economic cycle provides evidence that recessions and expansions are to be expected. However, looking over the last century, we can conclude that recessions have become a less prevalent economic season compared to expansions and inflations.

Despite the infrequency of recessions, they remain economically damaging. Common economic downturns will shrink output by 2%. Whereas a more severe downturn could set the economy back by 5%. Furthermore, a great recession, like the Great Depression in the early 20th century, deflated the American economy by a monumental 30% over multiple years.

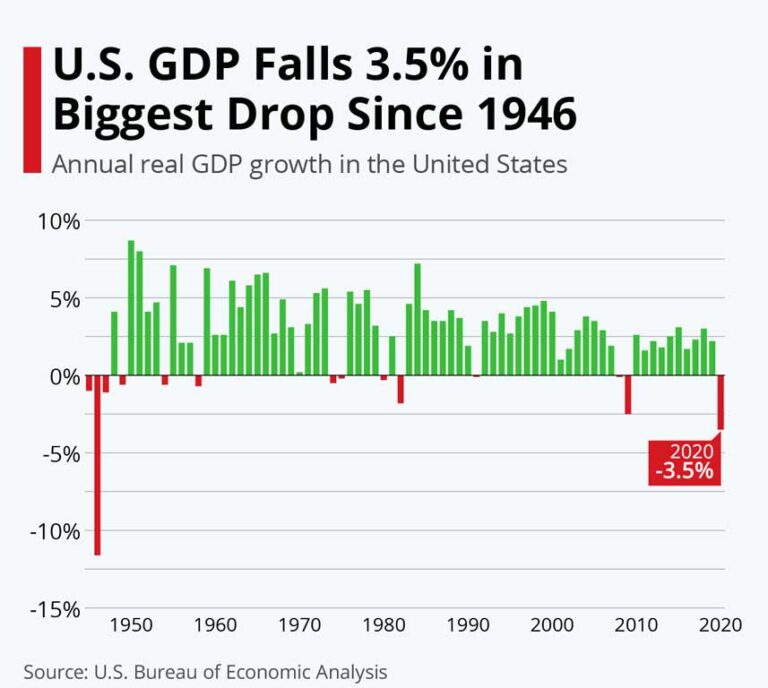

Covid Creates a Supply Chain Crisis

The most recent recession the United States experienced was in 2020 when Covid-19 hit. Extreme pandemic policies created a supply chain crisis which resulted in economic deterioration. Businesses including manufacturers and suppliers were halted, the labor force was told to stay home, and development, improvements, and economic growth were at an ultimate standstill.

Though recessions are typically categorized when the GDP slumps for more than two quarters, 2020 was a special case. Though only a few short months of economic decline ensued before inflation took over, the NBER nevertheless defined that season as a recession.

This was due wholly to the expansive and deep-rooted prevalence of the economic collapse. The United States experienced a 3.5% GDP collapse in 2020. Though it lasted only a few months, it surpassed all other economic declines since 1946.

How Does a Recession Affect the Economy?

The United State’s central bank is responsible for maintaining economic balance in the American markets. They aim for a stable cost of living and low unemployment. To attempt this balance, they can leverage interest rates, which alter the way financial institutions and Americans borrow money.

As interest rates rise to combat high inflation, borrowing is more expensive. When interest rates are low, to combat recessions, borrowing becomes more affordable.

With more expensive borrowing, there is less demand for it. Resulting in less available money for consumers to spend. With less available funds comes less spending. Less spending creates less demand. Less demand creates a recession.

Conversely, the reverse occurs to combat recessions. There is a decrease in interest rates, money becomes more available, spending picks back up, and there is an increase in demand. It really is a full-scale cycle. Naturally recurring and continually persistent.

Although federal policymakers are responsible for leveraging interest rates, they cannot do any one thing to prevent or end an economic recession or inflation. The length of these economic seasons would all be dependent on how businesses and consumers choose to proceed in these times.

How Does a Recession Affect Businesses

Recessions stem from an overcorrection of an imbalanced economy. They abruptly interrupt inflationary seasons. In response to federal intercession, recessions force businesses large and small, to make the appropriate adjustments to a decrease in demand.

However, recessions can have varying effects on different companies. These trials and adjustment decisions may be predictable based on the size and industry of a business.

For example, a small private practice may have a decline in cash flow as clients are unable to make payments on their bills or delay their appointments. Whereas a public sector Fortune 500 corporation may be able to bypass financial burdens by issuing layoffs, furloughs, or finding lower rates on resources with alternative suppliers.

The areas affected by a Recession may include:

- Unemployment rates

- Interest rates

- Business Sales

- Business profits

- Federal Finances

- The stock market

- Financial institutions

- Living standards

Below we will take a further look into each one of these areas.

Increased Unemployment

Increased and dangerously high unemployment is a staple of a recession. They go hand in hand. A recession is evidence of decreased economic activity. Because labor is a key economic input factor, it’s sensible that as output drops, employment rates would suffer.

Businesses cut costs in response to decreased sales. The biggest way to cut costs is in labor expenditures. Unfortunately, layoffs further shrink demand and thus, extend the economic downturn.

With reduced demand for goods and services, fewer employees are needed. Though demand is lowered, workloads may increase for the remaining employees. As a result, company morale may suffer.

Additionally, raises diminish and pay cuts begin amongst the risk of further job losses. Even though layoffs are the alternative, employees, of course, are reluctant to accept a cut in pay for the same workload, if not more.

Wage rate-to-workload ratios become yet another burden on the American worker, further fueling the turmoil surrounding daily life in a recession.

What’s more, employees who are laid off during a recession find it more difficult to re-enter the workforce and are more likely to become unemployed long-term.

Interest Rate Fluctuations

Because the economy is like a yo-yo, fluctuating based on supply and demand and balanced by the central bank’s Fed rate, credit availability is either tightened or loosened. It all depends on where the economy is in the cycle.

Rising interest rates – To combat peaked inflation, the central bank will jack up interest rates. In response, borrowing money becomes more expensive. The tightened credit availability will then cause a chain reaction toward demand, sales, profits, and employment. With the lack of available funds, demand lessens, and deflation replaces inflation. This aggressive approach to fighting inflation is aimed at providing relief to consumers’ wallets.

Decreased interest rates– Once the central bank has crushed demanding inflation and spending slows, the market may eventually come to a standstill. At a minimum, it may reach an unhealthy pace. This decrease in economic activity is when a recession hits.

From here, the vicious cycle continues. To combat the new symptoms of recession such as a decrease in demand, profit losses, and increased unemployment, the central bank once again has to make the appropriate adjustments to boost the market once more.

The Fed rate is decreased to stimulate borrowing and economic activity once more.

Decreased Sales

Decreased demand equals decreased sales. When funds are less accessible due to high-interest rates, consumer demand for goods and services dwindles. Consumers will take a look at their personal finances and begin to consider saving more and spending less. Non-essential items will have to wait and the market begins to slow.

Certain industries see the effects of dwindling sales more immediately than others. Some of these markets include retail, energy, manufacturing, and technology. Because of bloated inventories and overstocked retailers, manufacturers are forced to slow output.

Additionally, with lowered demand, there is a lack of budget for marketing and advertising. Therefore media and marketing businesses, whether online, print, television, etc, will also see a slump in their sales.

Profit Losses

In parallel with dwindling demand, profits slump to a potentially hazardous number. Businesses rely on steady cash flow for growth. When stores are barren and sales begin to trickle, businesses are looking at a formidable future.

In the previous economic season, before the decline, rates were inflated due to increased demand and lack of supply. With a need for more supply, manufacturers had cranked up their output to meet the market need. As a result, merchants, manufacturers, and suppliers are now overstocked and under-demanded.

Unfortunately, when demand dwindles, the new supply availability is now excessive. In hopes of selling the overstocked goods, merchants will lower their prices to boost sales. These lowered fees can result in hard-to-swallow financial losses.

Public corporation profit will additionally be affected by the stock market. Stock market prices tend to drop in preparation for a coming recession. Investors become less financially risky during times of uncertainty especially when businesses are teetering on the edge of financial tribulation.

Stock Market Decline

During an initial downturn in the economy, you will see the stock market also experience a decline. The best way this is determined is through the Standard and Poor’s 500. The S&P 500, is an index that tracks the stock market performance of the 500 largest public companies in the United States.

Market panic usually occurs in anticipation of a crash. When abrupt and rapid selling of stocks persists, it can further antagonize the market, dropping prices further. This creates a bear market. A bear market is a prolonged decrease in investment prices.

If handled appropriately, a bear market can lead to a silver lining. Lowered stock prices can seem troubling at first as many people become reactionary or play a defensive game with their finances during this time. However, it could be a good idea to buy at these low prices for investors who can hold on for the long run.

This is a different approach from how investors approach a Bull market, which generally takes place when the economy is healthy. As investors see certain company stocks increasing, they buy in anticipation to make a higher return on investment if they can hold onto the share as it rises and sell before it drops.

Many investors who play the stock market correctly have an experienced wealth manager that can help them navigate their financial decisions.

Federal Financial Aid

The federal budget relies on tax collections. As the United States experiences a decrease in sales, high unemployment, and lower incomes, tax revenue suffers as a result.

Although tax collections are at a minimum, there are many federal assistance programs aimed at providing relief to the American public during these times. However, federal legislation interference in the economy can be quite controversial.

This is because a lack of tax income results in an increased budget deficit. This deficit should limit the government’s ability to step in with public financial assistance. However, in hopes of counteracting a recession, the federal government steps in with:

- Unemployment checks

- Stimulus checks

- Food stamps

- Bailouts

- Etc…

These programs are called automatic stabilizers. Regardless of the lack of true available Federal funds, the government hopes that providing quick relief to people who need it the most will result in funds getting spent faster. As a result, it may stimulate the economy toward the boost in activity it needs.

Government Bailouts

One of the most controversial automatic stabilizers is bailouts. Bailouts are targeted relief for designated industries and/or specific companies. Many object to public aid to private or for-profit companies. These objections can be based on principle, the belief that the assistance is fully based on political motives or the idea that these funds are being incompetently misdirected.

As it stands, government bailouts to large companies can be a benefit. It preserves jobs and stimulates the economy. Ultimately reducing the unemployment rate. However, arguments can be made that bailouts encourage irresponsible industry behavior.

Unemployment Insurance and Stimulus Checks

Unemployment insurance and stimulus checks can also lead to controversial conversations. In many experiences, especially during the Covid-19 unemployment spike, stimulus checks and unemployment income were actually higher than income that would have been made through rejoining the workforce.

Employers found it difficult to hire new employees because so many Americans were making sufficient income to survive simply by relying on government aid. Critics would say this financial assistance had backfired on itself.

Rather than encouraging productivity and new job creation with more taxable income, Americans were stuck at home and yet, still reaping a federal financial reward. They had no incentive to look for work. And the government’s deficit continued.

Banking Crises

When stocks decline, public sector corporations are negatively impacted, unemployment increases, debts are unable to be repaid, and a banking crisis ensues. Banking crises are defined as liquidity shortages. This means financial institutions experience a shortage of funds.

When financial institutions lack funds, they are unable to approve as many loans. They are forced to become particularly selective.

Moreover, if the federal reserve tightening has not been lifted yet, borrowers look to avoid high-interest rates. Therefore borrowers then also become scarce. All of these factors add to the inability of banks to make a profit. This increases the liquidity shortage and prolongs the banking crisis.

Additionally, during times of financial uncertainty, investors fear if their assets remain in a financial institution, their value will drop. As a result, they will sell their assets and withdraw their funds from savings accounts.

Loan Delinquencies, Defaults, and Bankruptcies

Eventually, if a recession dips low enough, the Federal Reserve will lower the Federal funds rate in response to the downturn. Larger businesses could look into refinancing any outstanding loans at a lower rate.

However, most businesses find the refinancing fees unaffordable. As their sales deplete and their profits drop, they cannot afford to make appropriate loan payments. This causes many businesses to file for bankruptcy during a recession.

Additionally, when businesses become overly indebted, they may default on their debt during times of recession. This then drives the borrowing costs up for other businesses. It may even be cause for financial institutions to deny loan approval for similar businesses to protect themselves from the financial risk involved.

Falling Living Standards

During a recession, real per capita income falls due to deficient economic output and high unemployment. As a result, many households are unable to maintain their previous standard of living.

With many employees losing their jobs, they also lose their health insurance coverage that may have been an included benefit provided by their previous employer. This can add to a household’s financial burden if they have any medical bills or chronic conditions that require medical attention.

Additionally, with a lack of financial resources, nonessentials are a no-go. Families cannot afford to go on vacation, let alone afford a nice night out to dinner. Eventually, even groceries become hard to afford for many.

The stress of financial hardship can then cause an increase in divorce rates, malnutrition, and even homelessness.

How a Recession Impacts Small Businesses

Though both large and small businesses face a decline in sales and profits, the mere scale of small businesses makes it more difficult to pivot to avoid the risk of failure. Small businesses’ vulnerability calls for differing adjustments.

Small businesses are companies that have under 500 employees. This includes micro-merchants and solopreneurs. These companies surprisingly have contributed to just under half of the U.S. GDP.

Although great players in the game, these tiny businesses have little cushion to soften an economic blow. A recession is more likely to impact small businesses than large ones because they are more likely to suffer from a drop in sales.

Their lack of scale leaves a vast majority of small businesses with little power within their industry to weather the trying times a recession will bring.

Because lenders know that small businesses have fewer assets to serve as collateral, they are less likely to entertain loans to these types of merchants as credit becomes less available. When this happens, small businesses must get creative to keep afloat.

Small businesses are private entities. So unlike large public corporations, they cannot access additional funds through the selling of stock, issuing of bonds, or lobbying for government aid. As a result, small businesses are especially susceptible to failure during the tribulations a recession is sure to bring.

One exception to this was when relief acts were provided to businesses large and small during the Covid-19 outbreak. The U.S. government attempted to avert a massive wave of disastrous bankruptcies.

Can a Recession Hurt Big Business?

The short answer is yes. They are surely not immune. During the 2020 Covid pandemic, 244 big businesses in the energy, retail, and consumer services industries sought bankruptcies.

Even so, the impact is typically far less damaging compared to small businesses. This is simply because large corporations bring in far more profit. This profit provides a much-needed cushion during times of uncertainty.

With deeper financial stability, big businesses can afford more opportunities for cutting costs, rather than conceding to failure. Though not an easy decision to come to terms with, some advantages big businesses maintain to cut costs or increase cash flow to combat recessions are:

- Reducing or eliminating

- shareholder dividends

- Selling stocks

- Issuing bonds

- Lobbying for government aid

- Reduced hiring

- Issuing temporary furloughs

- Suspending pay raises

- Reducing pay

- Decreasing capital spending

- Looking for cheaper suppliers

- Decreasing marketing

- Reducing research and development

- Halting new product rollouts

- Resorting to layoffs

A positive takeaway is if a business can find a way to avoid issuing layoffs using alternative ways to save with long-term strategies in place, studies have found that they will be better off after a recession.

Are Recessions Bad?

Here’s the bottom line. While painful, unpleasant, alarming, and riddled with uncertainty, recessions are a natural and recurring feature of the economic landscape. However, they are not all bad.

Yes, there are many negatives that recessions bring. However, they do lead to some positive economic features that can be of benefit.

Do Experts Think a Recession is a Healthy Correction?

A small, short-term recession aimed at cooling off an overextended economy will likely do little damage. In fact, some experts argue that a recession may be a healthy correction to rectify an unhealthy and imbalanced economy. Making a new path for economic growth.

Some positive features a recession can induce are:

- Popped inflationary bubbles- Prices for goods and services decrease to a more affordable price.

- Lowered interest rates– Lower rates make borrowing and real estate more attractive. Potential homeowners find it common to wait for a market crash so they can afford to buy property.

- Deceased stock market prices–This can create investment opportunities for those who are willing to wait out their return on investment.

Though recessions are an unavoidable stage of the economic cycle and do have some value, their silver linings aren’t as attractive as wanting to soak in their storm-like effects for any longer than minimally necessary.

How Do We Know When a Recession Is Over?

A recession ends when the economy begins to grow again. Not when it returns to its original position before the recession.

To contact sales, click HERE. And to learn more about ECS Payment Processing visit Credit & Debit.