When a customer swipes their debit or credit card, does the money immediately hit your business bank account? Most existing businesses know that it does not. There is a process to move the funds from the customer’s account or credit line into your checking account, and there are many steps in between. However, one key step is credit card settlement.

What Are Credit Card Settlements?

Authorization and settlement do not happen simultaneously. That said, there is a spectrum of how close together these two activities occur based on the business activity.

In retail, authorization and settlement will occur very close together, in a more automated and almost simultaneous process. This is because the customer has completed a sale and left the premises with their item. Case closed.

However, there is more delay between authorization and settlement in the hospitality sub sector of food and beverage. When customers pay for their meals, they also write down a tip. The waiter or manager most likely needs to manually input the tip amounts at the end of a shift or the close of business day.

Authorization Holds

With hotels and rental cars, there is even more of a delay between authorization and settlement. This is because these businesses typically take security deposits or pre authorizations from which incidentals, damages, or payments are subtracted. An authorization hold is different from merely requesting an authorized payment in that it actually freezes some of the funds. The time between authorization and settlement may last even beyond the car rental or hotel stay by 1 to 3 days.

Many retailers (and other business types) ignore this strategy because it seems unnecessary. It can also create a negative customer experience until the final settlement occurs, especially if the hold amount is greater than the final purchase. However, in some situations, it may be an excellent proactive measure for making sure you get paid.

Although we mentioned that retailers typically like to settle quickly, e commerce merchants may intentionally leave a delay between authorization and settlement. They may place this hold while checking to see that an item is in stock and making shipping arrangements to avoid the potential pitfall of informing a customer that their desired item is out of stock and having to return the payment.

In summary, it’s important for businesses to understand that authorization and settlement of a credit card transaction may not happen simultaneously, especially for some industries. Your involvement in the credit card settlement process may vary. Sometimes, your payment processor has entirely automated the settlement process for you. But if any degree of involvement and proactivity is needed, don’t fall asleep at the wheel, because it could cost you.

Credit Card Settlements: Simultaneous vs. Batched

Again, some businesses set up payment processing so that authorization and settlement are nearly simultaneous, and the merchant doesn’t need to do much. Large payment aggregators like Shopify and PayPal commonly employ this simple model.

However, businesses that have progressed beyond this stage bridge the gap between authorization and settlement with batched requests, usually at the end of a business day. This means they gather up all the transactions that have occurred over that period and submit them to the payment processor to finalize the credit card settlement.

If you’re wondering why a merchant would choose to leverage batch settlements, there are a few reasons. One is that payment processors can offer lower fees for batches of payments instead of handling them one by one. Another is that the manual nature of sending batches allows the merchant to check things over and ensure everything is legitimate.

Risks of Delayed Credit Card Settlements

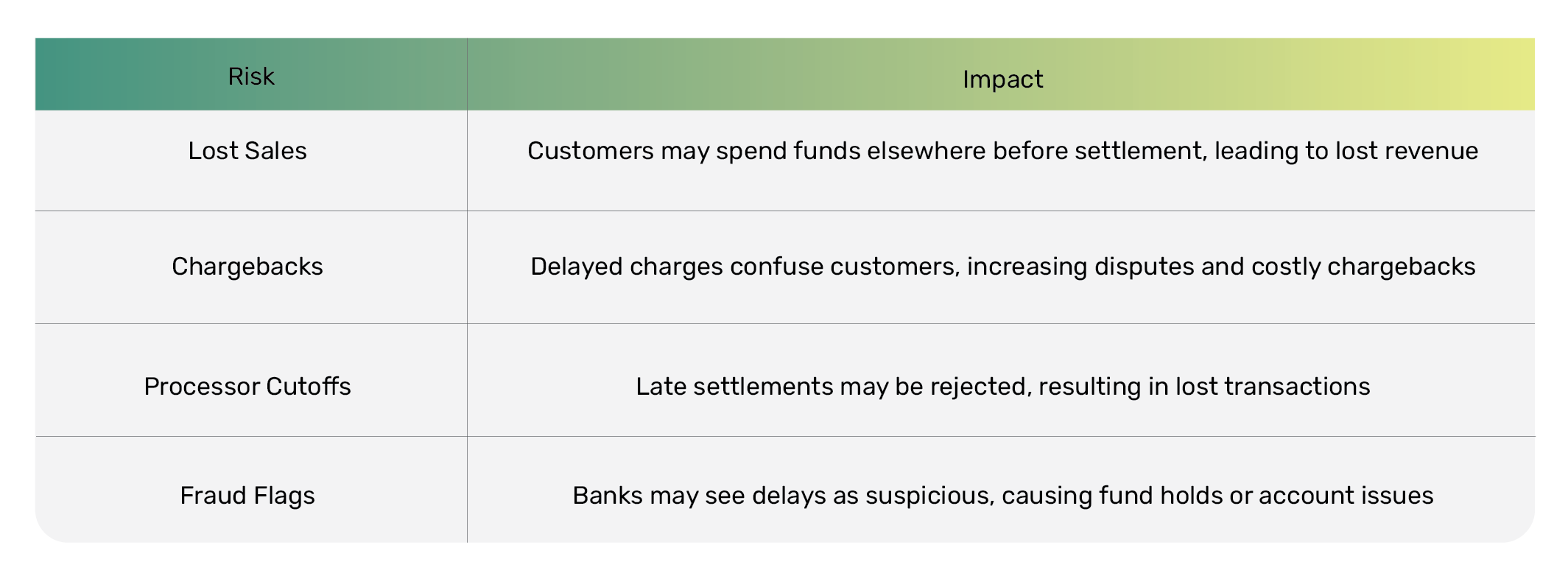

If a merchant is lax about sending credit card payment batches in a timely way, they can pile up. Beyond creating more work for themselves later, this can also expose them to lost sales and chargebacks.

Lost Sales

Let’s start with lost sales. When a payment is authorized, the merchant’s acquiring bank checks to see if the customer has funds or credit in their account. That doesn’t necessarily mean a hold on those funds is automatically applied. If a hold is not applied, and the charge is not settled later in the day, the customer may end up spending those funds somewhere else. Which, of course, costs the merchant their sale.

Additionally, card networks and payment processors may have cutoff times for letting unsettled charges linger. If you submit charges too late, they may reject them. However, unsettled or late transition settlements can also lead to disputes and chargebacks.

Disputes and Chargebacks

Even if the processor does accept and facilitate the settlement, a delayed settlement can cause customer confusion. If the customer does not recognize the charge on their credit card company app (I don’t remember shopping there yesterday), or even on their next month’s credit card bill, they might call their bank and report their own transaction as suspicious or fraudulent.

As mentioned, settlement is when funds are moved from the customer’s account to yours with the help of the card networks and the payment processor. If that transaction is ultimately disputed, the funds will return to the cardholder’s bank through a chargeback.

Because so many parties are involved in moving funds from the customer’s bank to yours, reversing that transaction is very complicated and expensive. It creates a cascade of fees that all parties will pass on to the merchant, not the customer. The average cost of a chargeback hovers around $200 just in fees alone, and that doesn’t even include the lost sale!

Difficulty in Fighting Chargebacks

Delaying settlements can also make it harder to fight a dispute if it comes up. As mentioned, a customer already has a greater chance to initiate a chargeback if you delay settlement. The more time goes by, the harder it becomes to gather relevant documentation and communicate effectively with the customer’s credit card issuer.

Delayed settlements can also trigger a red flag on the part of the payment processor, card network, or bank. They may view a delayed settlement as suspicious or fraudulent. As such, they may pause the settlement to examine the transaction, leading to a delay in funds.

Unfortunately, chargebacks are becoming an increasing problem for businesses. Part of this issue is a regulatory climate that has heavily favored consumer protections since the subprime lending crisis of 2008. Customers know it’s easy to call their bank and say that a charge was fraudulent. Sometimes, they even report their transactions to get a refund.

Other times, chargebacks are prevalent because a merchant is not working with a good payment processor. The processor will often communicate with the merchant on behalf of the customer’s bank, gathering documentation. A large, faceless aggregator like Shopify or PayPal is not going to “go to bat” for you, and a smaller company with an actual account manager you can speak to is not going to.

For all these reasons, it’s extremely important to settle your transactions in a timely manner. Most large businesses settle batches several times a day. While this might be burdensome for SMBs, you should certainly settle them by the end of the day.

Best Practices for Handling Credit Card Settlements

Let’s discuss more strategies for settling funds and avoiding disputes and chargebacks. One simple best practice is taking your credit card authorizations more seriously. Typically, merchants ignore the codes sent back to them by the card network on their card terminal. There are at least 50 different codes, so it’s easy to ignore everything other than 00 (approved) or 26 (insufficient funds).

Understanding Transaction Codes

It pays to be versed in all 50 codes. Many POS terminals do not spell out the entire code. Instead, they just provide the two digits. If you don’t know what those digits are, or your cashiers don’t, it doesn’t hurt to put a laminated list by the register or computer where you’re processing payments.

These codes are vital because they tell you what is going on with the customer’s card. They may suggest verifying the customer (01) or calling their bank (05). They may tell you it’s a fake card (21) or incorrect PIN (25). The customer may have exceeded their withdrawal frequency limit (34) or that they are suspected of fraud (59).

Some of these numbers will accompany a full stop on the transaction, such as an NSF code (insufficient funds). But others will allow you to continue with the transaction if you choose.

Consequences of Ignoring Authorization Codes

Let’s examine how ignoring some of these codes could work. Suppose you receive code 25 (incorrect PIN). You inform the customer and watch them try to guess the PIN again and again. Finally, irritated at the growing line behind them, you tell them just to hit credit. The transaction goes through, and they walk away.

Later, when you process your batches, this transaction does make it through. However, there was a reason that the customer did not know “their” PIN. It wasn’t their card! The actual cardholder will now file a dispute with their bank, creating a chargeback that you will ultimately pay for as the cascade of fees lands on you (not to mention the sale).

Or suppose you receive code 34 (the customer has exceeded their withdrawal limit). This means the customer has been busy with their card, so busy that they’re not even supposed to be using it anymore that day. If you ignore this code and attempt to settle later, you are not going to get paid for that sale. Even if it goes through, the funds might not be there based on the customer’s spending habits.

We could go through all 50 of these codes and discuss their impact on settlement. However, two examples are enough to illustrate that taking these codes seriously can make for smoother sailing later. These codes can provide warnings about transactions to avoid. If you avoid these transactions, your settlements will move faster, and your cash flow won’t be disrupted.

Accounting and Reconciliation Challenges

Another part of authorization may involve inputting the reason for the charge. This is extremely important for customers because it will appear on their billing statements. If they don’t recognize the charge, they’ll… you guessed it, file a dispute.

Understanding the Importance of Accurate Descriptions

Accurate descriptions are also important internally. It can be hard for your controller to reconcile the charges if they don’t know what they are looking at. A payment processing solution that can save line items to pre populate makes it much easier to input the nature and reason for a transaction. This, in turn, makes it easier to examine the charges later during settlement and accounting reconciliations.

Industry Specific Documentation Needs

Some industries, such as the medical insurance industry, need robust documentation more than others. This particular industry is notorious for confusing businesses (e.g., doctors, dentists, and therapists) in a billing quagmire. Healthcare providers must submit accurately labeled insurance paperwork to the insurer. The insurer collects these submissions in batches and then sends reimbursement back in single lump sums.

These lump sums are not broken down into detailed descriptions of each service rendered, which can obviously lead to serious confusion on the practitioner’s end. If the practitioner needs to bill the patient for a copay, failing to input a description for the charge can exacerbate the confusion. This is especially true if the provider needs to chase down a larger copay from the patient because the insurance company has denied a claim.

The best foundational solution for addressing such confusion is robust billing and payment processing software that can easily help with authorizations. For example, as mentioned above, tailored solutions that can pre populate line items to describe the nature of services rendered help.

The Role of Payment Processors in Settlement Management

Cloud based software with robust UX (user design), open source integration, and customizable programming have made payment processing software much easier. For instance, an antiquated POS might spit out a receipt with the aforementioned double digit codes, which a merchant (or their cashier) might choose to ignore.

Today’s POS and payment gateway systems are more robust and visually oriented. A contemporary POS or payment gateway system might be able to take that code and spell out the reason so that the code is not ignored. It may even integrate additional protocols, such as locking the cashier out of the transaction until they verify the card (if the code suggests it, as mentioned above).

Speak to your payment processor about how they can help you easily bridge the gap between authorization and settlement. Can they provide you with the opportunity to place holds? Does their user interface make it easy to authorize transactions and communicate with the card network? How automated can they make the settlement process?

Banks, card networks, and other fintech providers are quickly adopting AI and machine learning to foil fraud. For instance, a robust AI driven security solution may analyze cardholder spending habits and determine that a certain transaction falls outside the scope of that person’s age, location, or spending habits.

The best defense is a good offense, as they say. Robust security solutions at the point of sale can weed out transactions that will slow down your settlements later, leave you without funds because the customer spent them elsewhere, or subject you to chargebacks.

Future Trends in Credit Card Settlements

As mentioned, security measures at the point of sale go a long way toward speeding up the settlement process later. In addition to AI and machine learning, new forms of hardware are emerging that emphasize biometric keys like retinal and hand scans. Mastercard, Visa, and Amazon have all rolled out POS terminals that rely on these biometric keys not only to unlock payments but also to actually process them (e.g., with a hand or eye scan).

Cryptocurrency and blockchain are also providing exciting changes in the settlement of funds. These technologies are largely built on decentralized P2P exchanges that avoid middlemen like banks and card networks. As it turns out, banks and card networks may appropriate this technology to speed up settlement times (an interesting foray beyond the scope of this survey).

Conclusion

Credit card settlement begins the process of transferring funds from the customer’s bank to your bank. It is the second phase after authorization, where the merchant requests the funds. Since authorization and settlement are not simultaneous, the merchant may be required to initiate settlement, usually in batches.

Delaying settlement can lead to several problems, including lost sales, slower settlements, disputes, and chargebacks. If a merchant did not place a hold on customer funds, the cash or credit may not be available when they finally settle the charge. If the settlement has taken too long, the card network might stop the process and examine the transaction or reject it altogether. Finally, if the settlement goes through too late, the customer may not recognize the charge and attempt to reject it.

Accelerating the settlement process requires proactivity at the point of sale. You do not want to sidestep security measures or ignore authorization codes sent to you from the card network. Doing so can let fraudulent transactions slip through the cracks, delaying settlements or leading to chargebacks from the actual cardholder.

In conclusion, you want to keep settlements going as smoothly as possible. If settlements are disrupted, it can (in turn) disrupt your cash flow. A key advocate in making sure settlements go smoothly is your payment processor. They provide the tools to authorize and settle your charges with a minimum of hiccups along the way.

FAQs for Businesses Regarding Credit Card Settlements and Payment Processing Best Practices

Credit card authorization is the process where a transaction request is sent to the customer’s bank or credit card issuer to ensure sufficient funds or credit. Credit card settlement is when the funds are officially transferred from the customer’s account to the merchant’s account. Sometimes, the settlement and authorization can occur simultaneously, and other times, the business has to batch out their transactions to initiate the settlement. It depends on the industry.

Yes. It is very important to settle your credit card transactions by end of day. Delaying settlements can lead to lost sales if funds are no longer available, increased chargebacks from customer confusion, and difficulty fighting disputes due to insufficient documentation. They may also trigger red flags with payment processors, causing further delays or even fund holds.

Some industries hold authorizations on a card without settling the charge to ensure they are adequately paid. The business freezes a certain amount, typically higher than the final cost of the translation, to account for damages or lost property. This type of process is popular for hotels or rental car businesses.

To minimize chargebacks, businesses should ensure they settle their credit card transactions by the end of day. They should also carefully monitor POS authorization codes, and use accurate transaction descriptions. Working with a payment processor that provides strong support and documentation tools can also help mitigate disputes and streamline settlement processes.

Settle transactions by end of day.

Understand and act on POS terminal authorization codes to avoid problematic transactions.

Use payment processing software with robust features, such as pre populated line items and tailored solutions for industry specific needs.

Educate staff about the settlement process.