The idea of implementing payment solutions with biometric authentication isn’t a new concept. Biometric authentication concepts have been around for decades. First imaged in science fiction, this technology started to evolve from theoretical to real world applications.

So, while biometrics may be nothing new, today’s technology is allowing biometric sensors and devices to become smaller. This allows for biometric identification payment systems in new areas that simply weren’t possible even a few years ago.

Biometric authentication opens up a world of possibilities for payment security. It can streamline processing and reduce fraud, which helps lower costs for merchants and consumers. However, certain concerns over privacy and ethical considerations can arise.

Below, we’ll discuss the advancements in biometric technology for financial transactions and how they will impact the payment solution system in the coming years. We’ll also examine several challenges that biometric technology will need to overcome before widespread adoption and acceptance is possible.

The Basics Of Biometric Authentication

Biometric authentication uses one or more biometric markers to confirm a person’s identity against a known database or copy of that biometric data. Biometric refers to some biological trait that you exhibit that cannot be altered or, at least, can’t be easily altered.

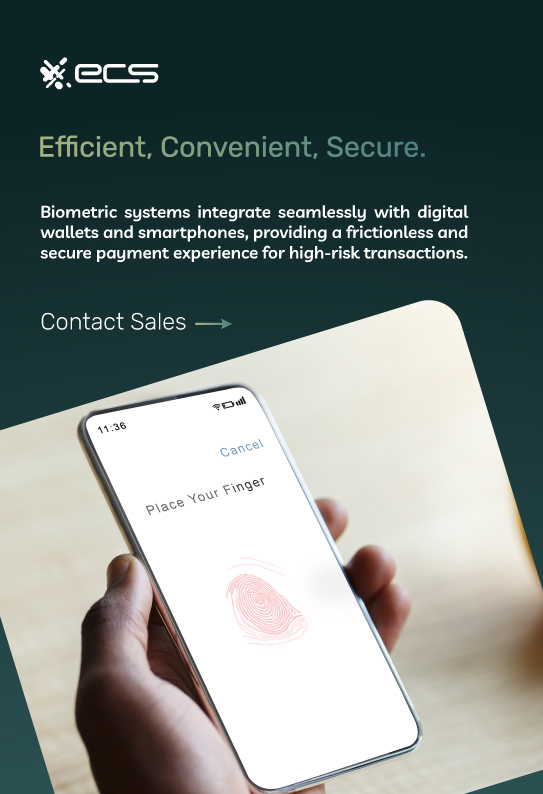

A simple example of a biometric marker is a fingerprint. Fingerprint identification has existed for decades, but early methods involved manual comparisons. Newer technology allows fingerprint readers to become miniaturized, such as in the older versions of the iPhone. Customers can make fingerprint authentication payments or perform other functions with an iPhone.

The miniaturized sensors that read biometric data can use a locally stored copy of the data or connect to global databases to compare identities.

Fingerprints are just one example, but newer technology has allowed for the use of more types of biometric data. This includes everything from blood vessel patterns in your skin to facial recognition.

The goal of biometric authentication is to provide a reliable method of ID verification that adds the least amount of friction to the verification process. That means it reduces the need to carry any sort of identification, remember a password, or carry a specific device.

What Is Biometric Payment Authentication

Whenever you make a digital payment, several authentication measures are taken. Most of these measures revolve around ensuring the credit or debit card being used is valid and that there are sufficient funds to cover the transaction.

One area that’s lacking in current digital payment solutions is a way to verify that the person using the card is the owner. Several methods, such as CVV numbers or PINs, can help ensure that the person making the transaction is actually in possession of the card. However, these methods don’t help confirm that the authorized cardholder is the one making the purchase.

Some high ticket purchases may require the cardholder to show a physical ID for verification. And due to fraud in some high tourism areas, merchants may also require ID for some purchases. However, these methods are slow and frustrate legitimate customers who simply want to pay for their goods and move on.

Biometric payment security solves this problem by adding an extra layer of security that can confirm the customers identity. Biometric scanning for secure transactions enhances the verification process, ensuring that the authorized cardholder is indeed the one making the purchase. This technology removes a significant risk of fraud and also helps to deal with certain disputes, such as with friendly fraud.

In the past, implementing this type of identification verification was cost prohibitive, and the technology was not always reliable. However, newer technology in the form of smaller sensors and cloud computing is allowing biometric identification services to be cost effective and highly reliable.

Secure Payments With Biometrics

While some of the underlying technology for biometric payment authentication is complex, much of it will be transparent to the end user and the merchant. The goal is to provide a secure, but fast payment. Integrating biometric sensors in payment processing play a critical role in achieving this balance.

Retail Biometric Payments

In a retail setting, fingerprint scanners are sometimes added to a typical payment terminal. The terminal is linked via the retail POS system to the cardholder’s issuing bank, which holds the customer’s biometric data.

The fingerprint data is confirmed at the same time as the credit card transactions, so it does not add additional time to the transaction.

This type of biometric authentication is reserved for higher risk transactions and would likely not be required for typical daily transactions. In those settings, traditional measures like PINs and other technology are sufficient.

However, with the rise of smartphones and digital wallets, mobile payments’ biometric authentication may become increasingly relevant.

Facial Recognition For Payments

One drawback of fingerprint biometric authentication is that it requires contact. As you’ve likely noticed, contactless payments are becoming the expected norm with customers, at least with everyday purchases and transactions.

Biometrics in contactless payments allows facial recognition integration, which enables secure transactions without physical contact. Facial recognition allows for contactless payments and biometric authentication, which are supported by biometric payment gateways to handle additional data. Facial recognition can take place within the POS using a camera.

Another option is to use a less invasive method that the customer can control. Facial recognition can take place on the user’s smartphone. Newer iPhones already contain Face ID technology.

Face ID or similar technology is combined with digital wallets to create a token. This token is sent along with the payment to confirm the biometric data, in this case, facial recognition.

Overall, this integration with smartphones and digital wallets will likely be how biometric authentication is integrated with retail transactions. Once again, this won’t be used for all transactions at first, but for certain high risk transactions, it can significantly lower the risk of fraud.

Types Of Biometric Authentication Technologies

You’re probably familiar with fingerprint and facial recognition. However, many new biometric technologies are being developed that use other markers and methods.

Voice Recognition Payment Systems

One newer area of biometrics is voice recognition and analysis. This technology appears to be less invasive when viewed by consumers. For example, a customer can simply repeat their name or a certain phrase during a transaction. The biometric system will then analyze the voice and compare it with a known sample on file.

This is done quickly as the voice analysis creates a numbered string via an algorithm. That numbered string is compared to the original known sample stored in a database.

Iris Scanning Payment Security

Each person’s iris is unique and can be scanned, similar to facial recognition. An iris scanner generally needs to be in close proximity to the eye, but a mobile device could be used for easier scanning.

Continuous Authentication

With continuous authentication, scans or data are constantly being read in real-time. With continuous biometric authentication, the customer does not need to make any extra effort since their device constantly confirms that they are in possession of it.

When the customer makes a purchase, this information is relayed to the payment terminal via a digital wallet token or NFC communications.

Continuous authentication offers the least friction during payment transactions since no extra steps are introduced to the actual checkout process. However, this additional layer of security would require cooperation between device makers and payment processing companies to develop standardized protocols and safeguards.

So, while exciting, continuous authentication is likely part of the future of biometric authentication and is not something for the short term.

Multimodal Biometric Authentication

With multimodal biometrics, several biometrics are used simultaneously, and they can be combined in different ways. For example, facial and fingerprint IDs are necessary to complete certain transactions.

Behavioral Biometrics

Another interesting area of biometrics is behavioral markers. Behavioral markers can include things such as typing patterns. Individuals tend to have unique and identifiable typing patterns when using a keyboard or similar device.

Algorithms can detect and analyze these patterns for continuous biometric authentication during device usage or online shopping.

Current Real Word Use Cases For Biometric Payment Authentication

Biometric payments have several use cases that would immediately benefit customers and businesses.

Micropayments

Micropayments are payments less than $1 and used for digital goods and services. They haven’t really taken off due to the lengthy authorization process for normal digital payment methods such as credit cards. The whole point of micropayments is so customers can instantly access digital goods whenever they want.

Biometric authorization via the customer’s device solves this problem and can open up a new revenue channel for many online businesses.

Customer Onboarding

If your business involves any type of customer onboarding, then biometric authentication and payments can immediately streamline the process. Processes like KYC and other compliance issues can slow down customer onboarding and create friction. However, companies must follow these procedures depending on the industry, such as MSBs.

Biometric payments and authentication can make this process much smoother for both the customer and the business.

Biometric Access for Banking Transactions

Additionally, biometric access to bank accounts enhances security and convenience for customers. This technology ensures that only those authorized can perform banking operations, reducing fraud and unauthorized access.

Contactless Payments Beyond NFC or Digital Wallets

With certain biometric payments, customers won’t need to pull up a digital wallet app or tap their card on an NFC payment terminal. For example, with facial recognition, the system can authenticate the user and charge the payment method that the customer has on file with the business.

This significantly streamlines the payment experience and can increase merchants’ revenue.

Are Any Companies Using Biometric Payment Solutions For Payments?

Yes. In addition to the Apple wallet, which incorporates fingerprint and facial recognition, Amazon has deployed its Amazone One Touchless payment solution. Amazon One uses vein recognition technology; customers only need to wave their palm over a contactless scanner.

The system authenticates the user and then charges the customer’s Amazon account or payment method on file.

Amazon has stated that there have been no false positives after millions of interactions with the system. Amazon has moved the Amazon One technology to their Amazon web services for further integration with other systems and for use by other developers.

JP Morgan

JP Morgan launched a private test program in 2023 to test biometric payments at select retail locations. Adopters of biometrics, such as JP Morgan, have experienced positive customer feedback, and these test programs are currently ongoing.

Mastercard

Mastercard and NEC began a partnership to combine NEC biometric technology with Matercard’s payment services. The system uses facial recognition, and customers can make payments at retail locations simply by smiling at a camera.

The partnership between Mastercard and NEC has led to several offshoots of the technology currently being developed, including AI and machine learning applications.

Benefits Of Biometric Payment Systems

Implementing biometrics in payment systems offers various benefits for both the merchant and the customer. Enhancing payment systems with biometrics can lead to improved security, faster transaction workflows, and lower fraud risks.

Lower Risk

The entire payment system structure is built around risk and risk management. Fee structures, interchange rates, and processing fees are all based on the risk of a transaction. This is why dipped card transactions with a signature are generally less expensive to process than card-not-present transactions.

With biometric payments, the final piece of the security puzzle falls into place, and the payment system can confirm that the actual cardholder is making the transaction.

Biometrics and payment fraud prevention work together to lower the chances of unauthorized transactions and provide a more secure payment environment.

Biometric payments can be made in retail or online, so the technology will benefit almost all merchants that currently accept digital payments.

Faster Transaction Workflows

Transactions that currently require a signature or physical ID checks are slow. They are slow for the customers but also slow down a merchant’s business, leading to a poor customer experience.

Biometric payments can remove the need for signatures or physical ID checks while maintaining security and lowering transaction costs. The result is a faster transaction and an improved customer experience.

Additionally, biometric verification for online payments can streamline eCommerce, providing a seamless and secure transaction for customers shopping online.

Less Risk For Customers

Businesses usually discuss credit card or payment fraud from their own perspective. However, identity theft and fraudulent charges can also be huge inconveniences for customers.

With identity theft, customers can spend months trying to unwind all the damage to their personal credit and other financial accounts.

Biometric payment authentication can greatly reduce the risk of identity theft. This helps consumers avoid costly fraud and also makes them more comfortable using digital payment methods.

Personalization Opportunities

Personalization in business is becoming essential for creating a positive customer experience. Customers want the brands they interact with to provide services and offers directly tailored to them as individuals.

Biometric identification can help businesses identify who is purchasing from their store or online website and then better tailor offers for that individual.

Generally, this type of personalization occurs through reward or loyalty programs. While these are extremely useful, they add complexity, and customers eventually have to manage the account.

With biometric authentication, much of this personalization can happen behind the scenes, creating a more seamless experience for the customer.

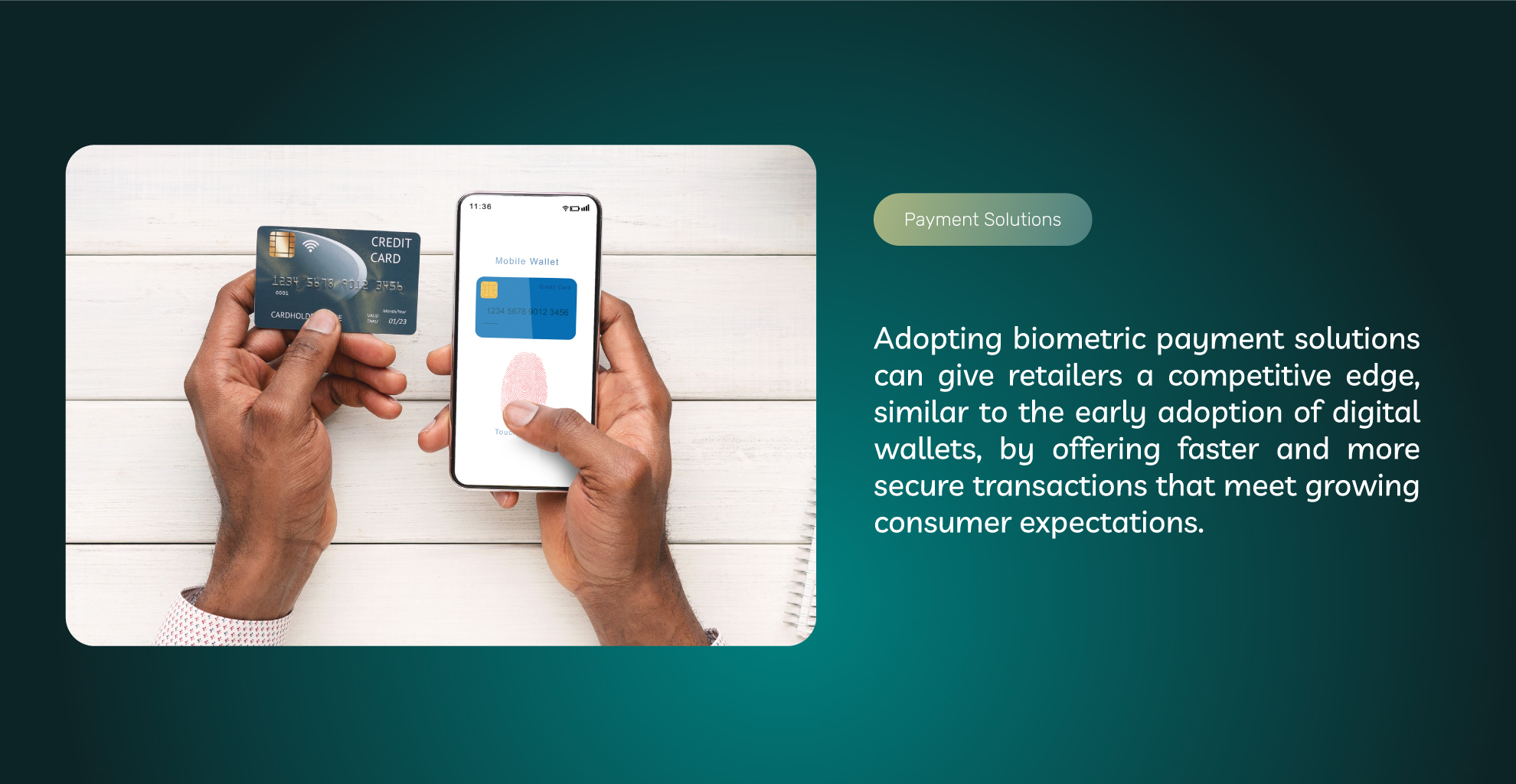

Competitive Advantage

Retailers noticed during the early pandemic that customers quickly adopted digital wallet payments and started seeking businesses that accepted the new technology.

Those retailers that were quick to adopt digital wallet capable payment terminals had an immediate competitive advantage over those retailers who were slow to spot this new trend.

Biometric payment solutions may very well play out similarly as customers gravitate to the improved speed and security that biometrics offer.

Brands and retailers that adopt this new technology will likely have an advantage in the marketplace over companies that hesitate or are resistant to the change.

Legal Compliance

In the United States and worldwide, new data privacy and security regulations are being discussed or implemented. Biometric authentication gives businesses a way to provide the ultimate security so they can remain compliant and protect consumers.

Biometric Authentication Challenges

Advancements in biometric payment technology offer many benefits, but there are challenges to overcome. As advancements in biometric technology payments continue to evolve, the future of payments biometrics will depend on how well the industry tackles the following issues.

Regulation

Some aspects of biometric data collection are still operating in a legal gray area. For example, some areas still don’t have laws detailing when or how facial recognition images can be captured or used.

This type of legal ambiguity can create problems for national or international brands that want to implement the technology.

Recently, the Target Corporation came under fire for capturing facial recognition images during self-checkout in Illinois.

Illinois recently enacted the Illinois Biometric Privacy Act (BIPA), which includes regulations for how biometric data can be captured and used. The problem arises because each state can have its own regulations, and many of these are changing as new technology emerges.

This lack of regulatory consistency is a significant hurdle for biometric payments.

Initial Costs

Biometric payments can save costs in the long run from decreased fraud. However, an initial investment is required.

Payment processors will need to integrate the technology into their current workflow and APIs, and card networks will need to find standardized protocols for handling biometric data.

Finally, merchants will likely need to purchase new payment hardware, such as terminals or POS systems. However, many modern POS systems likely already have most of the capabilities necessary for some biometric authorization.

Customer Adoption

Customer adoption is likely the X factor when it comes to how fast biometric payments enter the marketplace. Currently, airports and other facilities are already using facial recognition, so consumers are interacting with this technology.

For airports, customers can enjoy shorter boarding times when they use facial recognition at certain airports and TSA checkpoints.

However, TSA checkpoints are mandatory, and consumers don’t have much choice about whether to fly somewhere.

Retail is a different story, and if customers balk at certain biometric authentication techniques, adoption may suffer.

A key differentiator will be how much biometric payments improve the customer experience and how invasive the methods are. The more they help customers and are less invasive, the higher the chance of successful adoption.

Payment companies and businesses will need to collaborate to strike the right balance with biometrics so that customers do not feel uncomfortable with the technology.

Data Privacy

On one hand, biometric data can help with data privacy and security. However, for the system to work, biometric data must be stored somewhere so markers can be compared and authorization granted.

Ensuring the confidentiality of biometric data is crucial for biometric data security payments, as most consumers feel that their biometric data is more sensitive than other types of personal data, such as phone numbers or home addresses.

Payment companies must ensure that customer biometric data is held in the most secure way possible and that customers can opt out of what they choose.

One solution is allowing customers and individuals to store biometric data on their devices. Digital wallets and smartphones can store the data or communicate with service providers that store the data. In that type of scenario, the payment company would just receive a confirmation that the identity and payment are confirmed without actually handling the biometric data.

Biometric authentication trends, payments, and financial transactions are all moving to mobile devices, so most of the authentication will likely take place on those devices.

The Future Of Biometric Authentication in Payments

Biometric verification will likely soon become a part of our daily digital lives, so it’s inevitable that this technology will be used for payments and transactions.

Merchants should be open to these new technologies and carefully weigh the pros and cons relative to their business model, brand identity, and customer base.

The right implementations can give you a distinct advantage in the marketplace and open new opportunities. However, disregarding privacy or other concerns can end up harming your customer experience.

For more information about payment security, contact ECS Payments. We offer the latest digital payment solutions and technology to help your business thrive during today’s changing technological landscape.

Frequently Asked Questions About Biometrics in Payment Solutions

Biometric authentication uses one or more biometric markers such as fingerprints, facial recognition, voice recognition, iris scanning, and behavioral markers to verify a person’s identity against a known database.

Biometric payment authentication adds an additional layer of security to digital payments by confirming the customer’s identity against the credit card.

Benefits of using biometrics in payment solutions include:

•Increased security

•Streamlined processing

•Reduced fraud

•A more convenient payment experience for customers.

Yes, there are concerns about using biometrics in payment solutions which include a lack of privacy, ethical controversy, and the potential for false positives or negatives.

A real world example of biometric payment authentication is contactless payments using digital wallets. The customer would need to have their faces or thumbprint scanned by their smartphone to access the card on file.