Technology has consistently revolutionized business. Those who adapt, find new customers, and succeed. Businesses that are slow to respond often struggle and lose market share to more agile competitors.

But today, this change is happening faster than ever before. New technologies like 5G communications and artificial intelligence are completely disrupting business models and changing how businesses operate.

This disruption creates new opportunities at every turn, but businesses must be ready to embrace the change to turn disruption into profits. Part of that disruption is coming from digital payment system technology. Faster wireless communications and miniaturized computer hardware are creating an environment where virtually any device can send and receive payments.

A significant driver of this change is the Internet of Things (IoT). These interconnected devices are growing in number and, in some cases, are already conducting payment transactions.

To help your business navigate this new technology, we’ll explain IoT payment solutions and how they will be integrated with current payment systems worldwide.

What Are IoT Devices?

Internet of Things, or IoT devices, are essentially electronic devices that are not considered standard computer hardware like a PC, laptop, or smartphone. However, despite not being standard computer hardware, IoT devices have internet connectivity and can send and receive data over wireless networks such as 5G.

Beyond just internet connectivity, IoT devices can contain sensors, encryption hardware for security, and other miniaturized hardware.

Ultimately, IoT devices are designed to interact with the real world and respond to environmental triggers.

For example, an IoT sensor in an office can detect when people are present in a specific area and relay that data to other systems or individuals.

IoT devices have use cases for consumers, enterprise, and industrial applications.

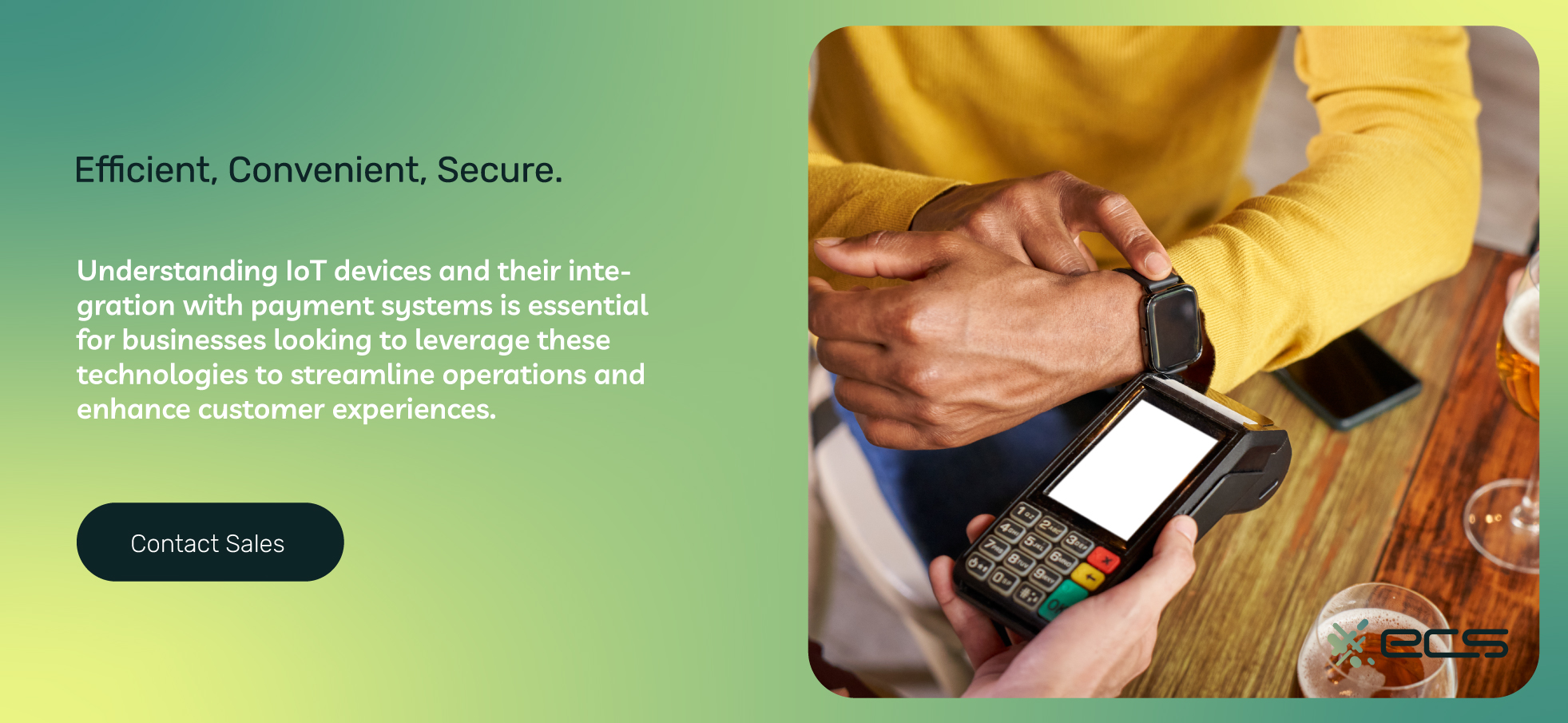

Some examples of IoT devices for consumers to use are wearables, such as the Apple Watch, which can function as a wearable payment device.

Currently, smartwatches take advantage of NFC technology, but in the future, they will work with IoT retail solutions to provide payments via 5G or other wireless networks.

Other examples are refrigerators that can sense when certain food items are placed inside or order new items as needed through smart device payments.

IoT devices are placed in cargo containers or trucks to track temperature or report when doors were opened, or cargo was unloaded for business and industrial use.

Machine To Machine (M2M) Payments

One specific area of interest in the payment industry is how IoT devices relate to machine-to-machine (M2M) payments.

M2M is when two devices communicate and conduct a transaction without humans initiating the payment. Depending on the scenario, M2M payments are fully automated or partially automated.

You can think of M2M payments as an entirely new category of payments. Similar to business-to-business (B2B) and business-to-consumer (B2C).

As devices become more intelligent and more connected, it is a logical step that they can handle transactions with each other without the need for human intervention.

An example of an M2M payment in the real world would be a smart energy IoT device located in a home or office building.

The device can track electricity usage and the electricity cost at different demand times. It can then decide to sell power back to the grid at an optimum price or purchase more units when demand is low.

This is just one example, but everything from smart appliance shopping to automotive applications can benefit from M2M payments.

The benefit of M2M payments comes from the frictionless nature of the automated payment systems. M2M payments completely remove the need for invoicing or billing in the traditional sense.

M2M payments can also facilitate payments and procurement immediately when necessary. There is no need for someone to be notified and then fill out a requisition or invoice.

The IoT device can order items or make a purchase immediately based on predetermined triggers and conditions. The IoT device can autonomously update internal inventory records or POS data whenever it makes transactions.

Consumers and businesses will begin adopting M2M payments in the coming years, making them a high-growth area.

Connecting IoT Devices To Payment Systems

For IoT devices to conduct M2M payments, they must first securely connect to existing payment systems and infrastructure.

Most applications accomplish this through the 5G network for contactless IoT transactions. This enhances security and provides the high speed and low latency required for IoT devices to connect to more extensive networks and systems.

Specifically for payments and transactions, IoT devices use a type of digital e-wallet. IoT digital wallets are similar to consumer digital wallets such as Apple Pay.

The IoT digital wallet uses tokenization to encrypt payment data, such as a bank account or credit card number. The token is sent via the 5G network to the payment processor.

Financial institutions involved, such as the issuing bank, if it’s a credit card, store the underlying credit card or payment information. These storage facilities are known as token vaults and are the only locations where payment data is stored.

The IoT device can create a new, unique token with each transaction, and it does not send sensitive payment information within the token itself.

The current payment systems you already use implement tokenization for Near-Field communication (NFC) payments, such as tap-to-pay with mobile phones.

M2M payments simply apply that proven technology to IoT devices to expand the number of locations and devices that can participate in transactions.

Use Cases For IoT Devices & Payment System Integration

Consumer, enterprise, and industrial sectors are actively using or developing numerous applications for IoT payment integration.

Automotive

Integrated IoT payment has several applications in the automotive industry. Waymo is developing self-driving or autonomous vehicles, which are one example of IoT integration.

These autonomous vehicles can contain IoT devices for paying tolls or other connected car payments while operating on the roads.

The goal is to eliminate the need for manual payment or invoicing, which is both time-consuming and adds extra costs for all parties involved.

The frictionless nature of M2M payments helps to enable other related technologies, such as fully autonomous vehicles.

Logistics

Logistics is an area where IoT devices and payments are being integrated.

Today, IoT devices are incorporated into many shipping containers for intermodal transport to track location and temperature and detect when doors are opened or unlocked.

Beyond these functions, payment integration can allow shippers and businesses to pay directly as soon as cargo is picked up or delivered.

These IoT devices can also handle payment changes due to expedited delivery or changes in the destination.

Smart Home Payment Integration

Smart home IoT devices can order a wide range of products and services as needed based on environmental triggers. Other smart IoT devices can use voice commands to make online payments. Other voice-assisted features can be used to reach appliance customer service or complete other tasks.

Wearable Devices

Devices embedded in clothing or as part of augmented reality glasses can connect with payment terminals automatically and complete transactions. Tokenization and other technologies securely accomplish this task to keep the customer’s data safe.

IoT Payment Challenges

While IoT payment integration offers a lot of promise, there are still obstacles to overcome.

Payment Security In IoT

We already discussed how IoT uses tokenization for security during payment transactions. However, totally secure IoT payments will require additional technology.

Due to the limited hardware within an IoT device, it often can’t contain advanced security layers, making it vulnerable to hacking and other cybersecurity attacks.

Another problem is password protection. Once again, due to the limited hardware, most IoT devices only use a simple password. The devices become vulnerable if users do not change or use these passwords correctly.

Part of the solution to these problems is the development of “trusted” IoT devices. Trusted IoT devices will incorporate cryptographic hardware to provide security protection beyond just a simple password.

The specific cryptography will render the devices unclonable, enabling them to possess unique identifiers that the payment system trusts. This will increase the security of IoT payment platforms.

Consumer privacy in IoT payments is another security concern in the payments market. Without additional security features, IoT devices can compromise personal data.

Accountability

One hurdle with IoT payment integrations is that devices have no accountability or liability. Authorizing payments can present an interesting issue regarding who is responsible when disputes occur.

The user periodically reauthorizes devices as a solution to this ongoing problem. By periodically reauthorizing automated or semi-automated payments, the device’s owner becomes accountable for payments made by the device.

Another solution to this issue and other security problems is using a public ledger or blockchain for IoT payments.

A public ledger in blockchain keeps an open record of all transactions on a network. Each node must confirm the ledger. This consensus can detect cloned or unauthorized devices and reject any transactions originating from them.

Another feature of blockchain technology that is useful in IoT payments is smart contracts.

Smart contracts are digital agreements that exist on a blockchain. The smart contract automatically executes when the parties involved meet the conditions of the contract.

Integrating IoT payments with smart contracts can execute many transactions when the blockchain confirms certain conditions have been met.

While this type of integration is still in its infancy, it shows the most promise for security and accountability. This is why IoT in fintech and blockchain technology are often discussed together.

Standardized Communication Protocols

Standardized communication protocols are necessary for any type of secure data transmission.

The current payment system used by businesses already has these protocols in place. Businesses access them via payment gateway APIs and other services.

However, since IoT devices are still relatively new, they lack certain standards necessary for secure data connections.

Part of the solution to this obstacle is simply using existing protocols, such as those for WiFi and 5G. Another option is to have the IoT device communicate with another edge device with more computing power. This edge device then transmits the data onto the payment system in a more traditional way.

Using a separate edge device can work in many enterprise and industrial settings. However, this may not be possible for consumer use or autonomous vehicles.

Standards are, therefore, the key to enabling consistent and secure transmissions between IoT devices and the larger payment system infrastructure.

Preparing For IoT Payment Integration & Digital Payment Trends

Preparing for IoT payment integration and M2M payments requires businesses to be agile and receptive to disruptive change.

You can achieve this by implementing best practices for payment processing. For example, most businesses should already accept the latest digital wallet payments and wireless processing options. This will help you transition to mobile wallets and IoT integration.

Beyond that, security best practices are something a business should focus on as they look to the future of IoT integration. Businesses with lax security will now face an uphill battle when implementing IoT and M2M payments.

Overall, the future of IoT in payments is likely not far off. It won’t be long before voice-activated payments and other IoT payment options start to appear in your payment data analytics.

Finding The Latest Payment Technology For Your Business

Digital payments are changing rapidly, and smart businesses are leveraging them to reach new customers and reduce operating expenses.

At ECS Payments, we offer the latest payment innovations designed for retail, B2B, mobile, and e-commerce processing.

Whether your business needs the latest digital wallet integrations or advanced POS systems for retail and online sales, our engineers can offer you the most cost-effective solutions for payment processing.

Contact ECS Payments today to learn more about our digital payment solutions that can prepare your business for the future.

Frequently Asked Questions About Integrating Payment Systems with IoT Devices

Internet of Things are electronic devices beyond standard computer hardware with internet connectivity and can send and receive data over wireless networks.

Some examples of IoT devices are

•Smart refrigerators

•Smart speakers

•Smart locks

•Smart thermostats

•Smartwatches

•Smart TVs

Pretty much any electronic device that has the word “smart” connected to it could be considered an IoT device.

M2M payments are transactions between two machines or devices that can be fully or partially automated without any human initiation.

IoT devices use various security measures to facilitate M2M payments, such as using 5G networks for contactless transactions and digital wallets with vaults for tokenization and secure storage of payment data.

Using IoT devices for payment automation has many benefits and can enhance daily life. However, challenges with IoT payment systems include:

•Security with limited hardware and simple passwords.

•Accountability for payment approval.

•There is a lack of necessary standardization for secure data connections.