The United States has officially ended production of new pennies. The final circulating pennies have been struck, and while billions of pennies remain in circulation, no new ones are entering the system. That raises questions many merchants haven’t had to think about before.

- How will I provide change for a cash purchase?

- Will cash purchases need to be rounded?

- Will customers argue over a few cents on cash transactions?

- Do I need to change my prices?

- Do I need to switch to card only transactions?

The fear of future penny shortages isn’t the reason businesses are moving toward electronic payments, but it does highlight a larger reality. Cash has become more complicated to manage while electronic payments have become easier, faster, and more common.

That’s why the debate around accepting credit cards looks very different today than it did twenty years ago. One reason businesses take cash only is because of the fees associated with digital purchases that eat into profit. But, is staying cash-only costing more than those fees ever could?

That brings many owners back to one question: Should a cash-only business accept credit cards despite despite the expense of processing fees?

A customer who only has a debit card or one who is stopping in on a run and only has a mobile wallet on their Apple Watch; those lost opportunities all affect your revenue. For many merchants, the economics of accepting credit cards are no longer about processing costs alone. They’re about customer expectations, operational efficiency, and keeping pace with how people actually pay today.

Why Many Businesses Stay Cash-Only

There are legitimate reasons why many businesses have resisted making the move.

Avoiding Processing Fees

The most obvious reason is cost. Every card transaction comes with fees. Depending on the card type, transaction method, and processor, a percentage of every sale goes toward interchange fees, assessments, and processing costs.

Whether you’re running on tight margins or simply don’t have any desire to give away a portion of your revenue, keeping 100% of every cash transaction can feel like the smarter financial decision.

Immediate Access to Funds

Cash is available to you immediately once the transaction is complete. There are no settlement periods waiting for deposits. The immediacy that cash provides can be particularly appealing.

Traditional Business Practices

Some businesses have operated successfully with cash for decades. If a process has worked for twenty years, changing it can feel unnecessary. That’s understandable. The problem is that customer behavior doesn’t always stay loyal to tradition.

Operational Simplicity

A cash-only setup requires very little infrastructure. You don’t need any payment terminals or software integrations, and you never have to troubleshoot payment technology.

Many owners appreciate that simplicity. At the same time, cash comes with responsibilities that are easy to overlook. You need to have available change, balance your cash drawers, investigate any discrepancies, and make physical deposits.

The end of penny production, however, goes to show how even small pieces of the cash ecosystem continue to evolve. Most businesses won’t notice a difference tomorrow morning. But managing physical currency requires ongoing attention.

How Consumer Payment Preferences Have Changed

Payment habits today look dramatically different than they did even ten years ago.

Customers Carry Less Cash

Cash is still part of everyday commerce, but it’s no longer the default payment method for many consumers. According to the Federal Reserve’s 2024 Diary of Consumer Payment Choice, consumers continue to rely heavily on debit cards, credit cards, and digital payment methods for everyday purchases. Many customers simply don’t carry the amount of cash they once did, especially for larger transactions.

Contactless Payments Are Growing

The shift toward faster and more flexible payment experiences with tap-to-pay increased by more than 200% world wide year over year. Whether customers use contactless cards, mobile wallets, or wearable devices, the expectation of quick, frictionless payments continues to grow.

Convenience Influences Purchasing Decisions

People don’t usually think deeply about payment options until they encounter friction. Then they think about nothing else. A customer who discovers they can’t use their preferred payment method may simply choose another business next time. Convenience tends to win.

The Hidden Cost of Being Cash-Only

When evaluating whether staying cash-only is truly saving money, business owners have to look beyond the fees they avoid. When asking should a cash-only business accept credit cards, it becomes less of a cost question and more of a revenue question when missed sales, smaller ticket sizes, and customer convenience are factored in.

Processing fees are visible. Lost opportunities often aren’t. That’s what makes the analysis tricky.

Lost Sales Opportunities

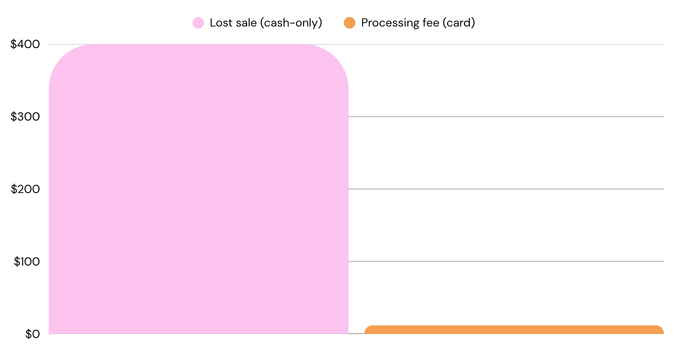

Picture a customer walking into your store planning to spend $400. They reach the register and realize they only have a card. Maybe they leave to find an ATM. Maybe they don’t. Many business owners assume customers will come back. Some do. Plenty don’t.

Reduced Average Transaction Sizes

One challenge for cash-only businesses is that spending is naturally limited by the amount of cash a customer has available at the moment. Electronic payment methods remove that constraint.

Research has shown that consumers rely on cards for a significant share of their spending activity, particularly for larger purchases where carrying cash may be impractical.

The number of credit card payments increased from two payments to 17 in a month from 2023 to 2024. The average dollar value per payment was also increased by 21%. When customers have the flexibility to pay electronically, businesses often find it easier to complete higher-value transactions.

Missed Business From Younger Consumers

Many younger consumers rarely carry cash. For some, paying electronically isn’t a preference. It’s simply how they pay for nearly everything. Requiring cash can create enough friction to push them elsewhere.

Competitive Disadvantages

If your competitors accept multiple forms of payment and you don’t, customers notice, and if they like to pay with their mobile wallet, rather than carrying cash, it will surely become a huge disadvantage. Maybe not immediately. But over time, convenience becomes part of the competitive equation.

Is Accepting Credit Cards Worth It For Small Businesses?

For many businesses, accepting credit cards creates advantages that extend far beyond the checkout counter.

Increased Revenue Potential

Every payment method you accept creates another opportunity to complete a sale. Removing barriers at checkout often translates into more transactions. Sometimes growth comes from marketing. Sometimes it comes from making it easier for customers to buy.

Higher Average Ticket Sizes

The larger the transaction, the more important payment flexibility becomes. Customers making larger purchases often prefer cards. For one, cards offer incentives like points and cash back, so for larger purchases, customers will typically prefer a card to cash due to the higher earnings.

Customers may not have a large amount of cash with them. Carrying cash can make a person an easy target for theft or other dangerous situations. Additionally, large amounts of cash take up a lot of space. Despite the risks and inconvenience of using cash, some clients may not have the funds available upfront and may need to rely on credit to make a purchase.

If a client has to choose between two products but only has enough money for the less expensive item, you could lose a sale. However, if you offer credit card payments, that customer is more likely to choose the better, more expensive option if they can purchase it with credit.

Improved Customer Experience

A payment experience that feels easy and familiar removes unnecessary friction from the buying process. Nobody walks away saying, “That was the best payment terminal I’ve ever used.” But they absolutely remember inconvenient experiences.

Enhanced Business Credibility

Consumers tend to associate electronic payments with professionalism and modernization. Fair or not, businesses that accept cards will appear more established and trustworthy to their clients.

What Credit Card Processing Actually Costs

Processing fees deserve careful evaluation, but they should be viewed within the broader context of business performance.

Understanding Processing Fees

Most processing costs consist of three components: interchange fees paid to issuing banks, assessment fees paid to card networks, and processor markups. Your costs will vary depending on transaction type, card type, and your processor’s pricing structure.

Looking Beyond the Percentage

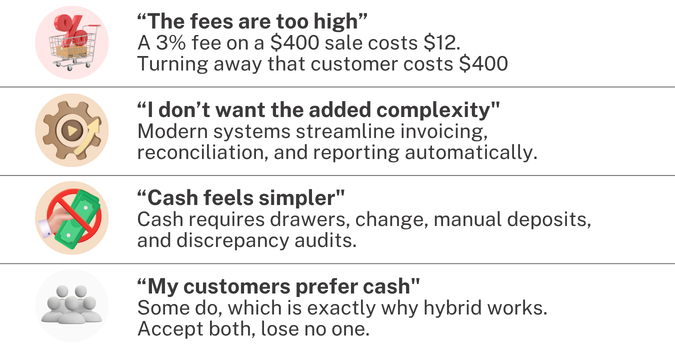

Business owners often focus exclusively on the percentage of the transaction fees. But evaluating cost without considering revenue impact creates blind spots. Though a 3% fee on a sale may feel expensive ($12 from a $400 sale, for example), a 100% loss on a sale ($400 to play with the same example), because you only take cash, is much more costly.

Industries Where Card Acceptance Delivers Significant Value

Some industries benefit more than others from broader customer accessibility with electronic payments. Customers now expect quick, contactless transactions. Fast checkout with these payments improves customer flow and can simplify your invoicing, billing, and collection in the following industries:

- Restaurants and Food Service

- Retail Stores

- Service Businesses

- Contractors and Home Services

Common Concerns About Accepting Credit Cards

If you’re considering transitioning from cash to digital payments, you may have similar concerns that plenty of other business owners have expressed. Business owners often raise similar concerns when considering a transition:

- The Fees Are Too High

- I Don’t Want Additional Complexity

- Cash Is Simpler

- My Customers Prefer Cash

Your concerns are valid. But there are ways to work around your concerns to see that concerns don’t have to equal truth behind alternative payment options for your business. As far as cost goes, the key is comparing fees against potential revenue gains, customer retention, and operational efficiencies. If you only look at expenses, that tells only half the story.

Cash may have seemed simpler in previous years. But today’s payment systems are significantly easier to manage. In fact, modern payment systems frequently reduce complexity rather than create it. Digital payments have helped streamline reporting, reconciliation, invoicing, and transaction tracking. Not to mention inventory, customer relationships, and more.

And yes, sometimes customers do prefer cash, which is why a hybrid option is a great choice for many businesses.

Questions Every Cash-Only Business Should Ask

Ultimately, the question of should a cash-only business accept credit cards depends on how often customers ask for card payments, how much revenue may be lost at checkout, and whether competitors offer more convenient payment options.

Before making a decision, consider a few practical questions:

- How Many Sales Are Being Lost Today?

- How Often Do Customers Ask About Card Payments?

- Are Competitors Accepting Electronic Payments?

- Would Faster Payment Collection Improve Cash Flow?

- Could Additional Convenience Increase Revenue?

The answers often reveal more than processing fee calculations alone.

Signs It May Be Time to Accept Credit Cards

Several indicators suggest it may be time for a cash-only business to consider accepting credit cards, including growing customer demand and changing expectations. Increasing competition from businesses that offer multiple payment methods can put cash-only operations at a disadvantage, while expanding business operations often requires the flexibility of electronic payments.

Furthermore, larger average transaction values often exceed what customers are comfortable carrying in cash, making card acceptance essential for customer convenience and an improved overall experience.

How ECS Payments Helps Businesses Transition From Cash-Only Operations

Making the move from cash only to hybrid or full digital payment doesn’t have to be disruptive. ECS Payments is an expert in transitioning our merchants to smoother payment solutions with ease. Our payment solutions are designed to fit existing operations rather than force operational changes.

From countertop terminals to mobile payments, businesses can accept credit and debit cards through our reliable processing platforms. Our customizable and clear pricing structure options help business owners understand their processing costs and make more informed decisions. Of course, questions will inevitably come up. Fortunately, ECS Payments merchant services provides dedicated support to help businesses navigate setup, optimization, and growth.

Final Thoughts

Although production of the penny is no longer, cash isn’t disappearing tomorrow. Many customers still use it, and many businesses will continue accepting it for years to come.

The challenge is that consumer expectations continue moving toward convenience, flexibility, and electronic payments. For a growing number of businesses, the largest cost isn’t the processing fee attached to a card transaction. It’s the revenue that never materializes because a customer couldn’t pay the way they wanted.

If you’re asking, “Should a cash-only business accept credit cards?” the answer depends on your customers, your industry, and your growth goals. But it’s a question worth examining carefully because the economics of payment acceptance have changed.

ECS Payments helps businesses evaluate those tradeoffs and implement payment solutions that balance cost control, customer convenience, and operational efficiency. If you’re considering accepting credit cards for the first time, a conversation with the ECS Payments team can help you determine what makes the most sense for your business.