With technology advancing faster than ever before, the future of payments is poised to revolutionize the way we shop and sell, promising a seamless fusion of convenience, security, and unimaginable possibilities. Technological advances are impacting virtually every aspect of our lives. Everything from how we communicate to how we run our businesses to the customer experience is changing as new technology emerges.

Staying ahead of these technological changes isn’t just an option in business. It’s a necessity. Falling behind in one area or not leveraging the right technology can quickly cede an advantage to your competitors. This means every business needs to stay on top of the latest trends in technology.

One area undergoing the most change is payment processing. New forms of digital payments have emerged recently, and consumers have adopted them at a record pace. Now, consumers want many different payment options, whether in person or online.

This means businesses must stay one step ahead of the latest payment trends to capture these customers. Leveraging these new payment technologies can give businesses the edge they need in a highly competitive marketplace.

In this article, we’ll cover the latest emerging payment technology trends. We’ll also look to the future to see what new technologies are on the horizon.

Digital Wallets Experience Fast Adoption

The first example of a mainstream digital wallet dates back to 1997. The Coca-Cola Corporation wanted to develop a mobile way for consumers to pay for drinks at vending machines. In 1997, they based their original digital wallet on text messaging, which was still somewhat new.

Of course, we all know mobile technology has changed drastically since then. Modern digital wallets now exist on smartphones and use near-field communication (NFC) technology to complete payments.

NFC only works in ranges of 5 cm or less. So, the phone or device is essentially “tapped” on one of the newer NFC payment terminals.

Even a few years ago, the modern digital wallet was more of a niche way to pay. Only early adopters were interested in going through the setup to enable their digital wallet.

However, like many changes in consumer trends, the pandemic caused an increase in interest in contactless payment systems. Digital wallets saw an increase in adoption in 2020 of 12%, and that trend has continued.

Recent polls have shown that 53% of consumers use a digital wallet more than traditional payment methods. What’s more interesting is that the same polling showed 51% of respondents would not shop at a business that didn’t offer digital wallet payments.

For many businesses, not accepting digital wallet payments can dissuade over half of your customer base from shopping with you. Metrics like this show how imperative it is that businesses stay up to date with the latest payment processing trends.

Evolution Of The Digital Wallet

The popularity and rate of adoption of digital wallets tell us that this technology is here to stay. But as with most technology, it’s also evolving rather quickly.

The next version of this payment technology will be so-called “super wallets” or super apps. These are essentially extensions of the digital wallet, but they can perform many other functions. Many people consider these as future credit cards.

Countries outside of the United States have already released these super wallets. Besides just holding your payment information, a super wallet can also hold things like electronic car keys, ticket information, driver’s licenses, and more.

Several states in America have already passed legislation allowing various Apple apps to work as legal identification. This is the early stages of creating a super wallet here in the U.S.

Affluent customers and unbanked individuals equally favor super apps and super wallets, making for an interesting statistic. This means their popularity cuts across demographic lines. It also means businesses must know that most customers will soon use these apps.

Elon Musk, the founder of Tesla and the current owner of X (formerly Twitter), has teased that he wants X to be a super app with digital wallet functionality.

The bottom line is that digital wallets are the future of upcoming payment trends in retail, and many of the top tech firms like Apple and X are working on promoting their adoption.

If your business isn’t accepting the latest digital wallet payments, contact ECS Payments. We offer the latest payment solutions built around digital wallets and other advanced payment systems. Contact us today to learn more and start driving sales with digital payment innovations from ECS Payments.

Digital Wallets and CBDCs

Central bank digital currencies (CBDCs) are digital versions of a country’s fiat money. Not long ago, niche economic circles discussed these as a far-fetched idea, not realizing they would actually be the future of payments. But now, virtually every nation is conducting testing on the viability of CBDCs.

China has already conducted real-world implementation of CBDCs using their digital Yuan. Real consumers conducted the tests in several large Chinese cities.

The U.S. is not far behind. The Federal Reserve is studying a digital dollar and how it can increase access to banking services and speed up payments. However, at this time, there is no pilot program underway like there is in China and some other countries.

When the central banks launch these CBDCs, they will require a digital wallet. It’s not clear if CBDCs will have their own digital wallets or if they will be compatible with existing wallets.

The China pilot program used a specific app for the digital Yuan. However, the app’s functionality allowed for top-ups via Mastercard and Visa. CBDCs will eventually come, possibly launching in Asia first. But when they arrive, consumers will look for merchants who can accept these new digital wallets.

This means businesses will need to be prepared to accept different digital wallets. In some cases, consumers will use government-issued wallets; in others, they may combine them with super wallets or apps.

You should incorporate digital wallets into your current payment workflow if you’re a merchant. This will help make the transition easier as new technology emerges.

New Payment Technology = New Revenue Potential

With the rapid changes in payment technologies, some merchants find it difficult to keep up. The changes that will come with the future of payments may seem hard to adapt to.

However, it’s important to remember that virtually every advance in payment technology has opened up new revenue streams for businesses. The more ways consumers have to pay, the more customers you have. Not only that, the more payment options offered generally result in higher overall ticket amounts.

The advance of digital wallets is a perfect recent example. Despite digital wallets being new, polling finds that customers who use these new technologies tend to spend more than they otherwise would.

In the Forbes survey discussed earlier, 47% of respondents said they spend more money using a digital wallet than cash, cards, or other payment methods.

Driving higher ticket amounts is one of the most cost-effective ways for businesses to increase revenue. Since it doesn’t require acquiring new customers, this revenue growth method has a very high ROI.

The statistics and payment trends show merchants should be excited about new payment technology, which invariably increases overall sales and growth potential. This is especially true considering the relatively small investment needed to adapt to these new technologies.

Items like new payment terminals or updates to POS systems are not hard to implement if a merchant uses a reliable payment processing company.

Cryptocurrency Payments

Cryptocurrency has had a wild run over the last few years. In the heat of the Bitcoin frenzy, younger consumers flocked to Bitcoin and other cryptocurrencies as both an investment and a possible payment solution. It was an exciting addition to the future of payments.

Several luxury car brands, such as Ferrari, announced they would accept Bitcoin when paying for one of their vehicles. Ferrari announced that they made the decision due to requests from both their dealers and consumers.

A Ferrari isn’t your typical retail purchase. However, when a large luxury brand such as Ferrari announces that its customers want to pay in cryptocurrency, retailers should take notice.

Ferrari announced in October of 2023. Before that, many firms tried mainstreaming cryptocurrency payments for retailers selling traditional goods. Most of these options revolve around Bitcoin debit cards. These cards use the traditional credit card payment network, but customers add funds via Bitcoin.

With Bitcoin debit cards, the retailer accepting them does not receive cryptocurrency. Instead, the car issuer converts the customer’s funds from crypto to fiat, and the retailer receives the fiat. The transaction is handled like any other card transaction through existing payment infrastructure.

Below are some companies that offer popular Bitcoin Debit cards in 2023:

- Coinbase

- Crypto.com

- Wirex

- Binance

As mentioned, these cards convert crypto to fiat before sending the funds to the retailer.

However, other retailers are accepting cryptocurrency directly from crypto wallets. Crypto wallets are a digital wallet that stores cryptocurrency. These mobile wallets can exist on smartphones or other devices.

The customer’s and retailer’s wallets generally communicate via a QR code to transfer funds.

One example of this is the clothing brand Ralph Lauren. Their high-profile Miami retail store accepts direct cryptocurrency payments from customers’ digital wallets. In the case of Ralph Lauren, they receive the crypto, not fiat funds. They can then store or convert the funds to fiat on a cryptocurrency exchange.

Other retailers accepting direct cryptocurrency payments are AMC Theaters and Jomashop.

How A Retailer Can Accept Cryptocurrency

Most retailers can already accept the crypto-to-fiat type of debit cards. All of these operate on the Visa or Mastercard networks and process just like any other debit card. To accept direct payments, there are a few options that retailers can consider.

The first is simply to create their own crypto wallet. This option is only viable for small or niche merchants with relatively low volumes. However, this is also the easiest method to use and requires the least investment.

The other option is to create an account with a cryptocurrency exchange to accept retail crypto payments.

One example is a company like Coinbase. A retailer can open a Coinbase account and access their exchange services and API (application programming interface).

You can integrate the Coinbase account with many different POS systems. When conducting a crypto transaction, the POS system will scan the customer’s wallet to transfer the funds. When the transaction is complete, the Coinbase API will send a message to the POS system that the funds are being moved.

Potential Benefits Of Cryptocurrency Acceptance

One of the main benefits promised by crypto is that there are no chargebacks. This means no chargeback fees or other hassles. Crypto transfers are essentially permanent. However, a retailer can still refund a purchase if they choose to.

However, there is no way for the customer to force a refund or chargeback. It’s important to note that this is only possible with direct cryptocurrency payments. Crypto to fiat debit cards follow the same rules as other Visa or Mastercard-branded debit cards.

Another possible benefit is low transaction fees in many cases. Crypto fees can be extremely low, especially on larger purchases. This is possibly why some luxury retail brands are promoting their use.

The downside is that fees can fluctuate wildly due to the currency crypto marketplace. For example, during the height of the Bitcoin boom cycle, fees to move funds skyrocketed and, in many cases, were higher than traditional card processing fees.

Fees have since normalized for the most part and have been relatively low. New technologies like the Lightning Network have been implemented to speed up Bitcoin transactions and reduce fees.

Real-time payments and cross-border payments are another use case for cryptocurrency. These payments can move across countries without dealing with international banking issues. They can also work for instant payments and online payments.

Cryptocurrency vs CBDCs

It’s easy to confuse these two possible future payment technologies, but they are quite different from each other. CBDCs are essentially just a digital version of a government’s currency. They are “centralized,” meaning they come from a central authority. In the case of a U.S. CBDC, they would come from the U.S. Treasury and Federal Reserve.

In a retail setting, businesses treat these CDBCs like cash or standard credit card payments. As a retailer, you may need new hardware or software to accept certain CDBC payment methods. But overall, they would just be a digital version of the dollar.

Cryptocurrencies are not government-issued. They are also not centralized in many cases (although some are, such as XRP). Being decentralized means these are peer-to-peer transactions, and there is no middleman or clearing house.

One interesting aspect of these two technologies is that they also compete with each other in some ways. If the U.S. government ever releases CBDCs, it’s unclear what they will do to cryptocurrencies.

For example, China banned certain cryptocurrency activities before implementing its CBDC testing program. It’s unclear if these two moves were related, but they demonstrate the competing nature of these two technologies.

In a country like the U.S., it’s possible that these two technologies could coexist, assuming the right regulatory framework. This means that retailers in the future may accept both CBDCs and cryptocurrencies.

The Future of Payments In The E-commerce Landscape

Over the past decade, e-commerce has been growing steadily. It shows no signs of slowing down. The pandemic reignited the market as many shoppers did more of their buying online, from home.

But now, even as the pandemic has faded away, those trends continued, and e-commerce continues to see robust growth in 2023 and beyond. However, that growth has also not been equal across the entire e-commerce space. Several areas have seen more rapid growth than others.

One example is in the area of subscription services. In the early days of the Internet, subscription services were quite popular and drove much of the technological advancement in payment technologies.

However, that trend faded, and soon, traditional retail took over as platforms like eBay and Amazon set the tone for e-commerce. But subscription services are hot again, covering a range of products and services.

One of the hottest trends in the last few years is subscription box services. You’ve likely seen these services advertised, or perhaps you even use one yourself. With subscription box services, customers pay a flat subscription fee.

The company sends customers a curated box of specialty items for that monthly fee. Depending on the service, this box can contain clothing, outdoor equipment, or just about anything.

These boxes have become extremely popular with consumers. Most marketers believe that one of the reasons these are so popular is because e-commerce has reduced a lot of “window shopping” that consumers would usually do.

This means consumers often feel unaware of all the products that may interest them. To counteract this, consumers put their trust in various brands to help curate a selection of bespoke items that match their tastes.

But this trend of subscription box brands requires special payment considerations. Subscription boxes require payment services that maintain continuous payments through different situations.

In subscription models, one of the biggest threats is churn. Churn is the rate at which customers unsubscribe. Payments can significantly influence churn because any billing information issues on file can lead to a missed payment. If the customer doesn’t want to fix the issue, that results in a lost subscription.

Also, the small payment hiccup may cause the customer to consider whether the subscription is worthwhile, which can also lead to churn.

Payment technology advances have helped remove many of these pain points for subscription box retailers. By finding ways to keep the monthly billing on schedule, the right payment processing allows these businesses to maintain profitability and increase their average revenue per customer.

As e-commerce sectors like subscription box retailers grow, so does the competition. This means the cost to acquire a new customer goes up. By using the latest payment technologies, businesses can increase their customer lifetime value, which makes the cost to acquire a better investment.

E-commerce Buy Now Pay Later (BNPL)

BNPL is a newer type of retail credit to enter the list of ecommerce payment trends. It works via open banking and API access between the BNPL provider and the customer’s bank account or other financial institutions.

The BNPL service works with the retailer, and the retailer generally receives the entire purchase price immediately. Although, in some cases, there can be different agreements.

BNPL adoptions have skyrocketed in the last few years. It has slowed down recently, but according to a McKinsey report on digital payment trends, a third of consumers say they’ve used BNPL services in the last year. More interestingly, 15% of consumers who haven’t used this type of financing say they are interested in doing so.

This suggests a good amount of consumer preference for these services, which will likely continue to grow.

Some of the more popular BNPL services are:

- Affirm

- Afterpay

- Klarna

- Apple Pay Later

Some of the moves to BNLP have displaced credit card usage, although it can vary. Of the roughly 30% who used BNLP services, 29% say they use BNLP instead of credit cards.

One thing to keep in mind with BNPL and other new payment technologies is that regulation can often be a game-changer. Much of the success of BNLP payment technologies was due to relatively low regulation in this new space.

This allowed many firms to jump into action to attract a lot of investment capital. Many of these firms are operating at huge losses, hoping to grab market share. State and federal authorities are actively considering new regulations. This regulation could change the BNPL landscape.

Regulation is always an X-factor when it comes to new payment technologies. However, that doesn’t mean retailers need to be hesitant. BNPL services have been relatively easy for e-commerce retailers to integrate into their currency payment processing workflow. As a result, the adoption was generally worth the effort in most cases.

This is another example of why merchants should try to be open to new payment processing technologies.

The Future Of Digital Payments And Payment Processing

Currently, it looks like the change most retailers will see is in the use of digital wallets. Whether on smartphones or smartwatches, using physical cards may become a thing of the past.

However, that doesn’t mean that the card networks and payment processing underneath it all will change drastically. Instead, many new technologies are simply integrated into the current payment industry system merchants already access.

However, being additions to the system means merchants must keep up with digital trends in payment. As we’ve seen with digital wallets and services like BNPL, a merchant can alienate a significant portion of their customer base by not offering these technologies.

Therefore, any merchant looking to grow their business in 2024 and beyond should embrace new digital payment technology and try to integrate it into their current workflows when possible.

Widespread cryptocurrency adoption and CBDCs are likely further away. But digital wallet payments are paving the way for both technologies to emerge. Physical cards will likely become a “legacy” payment method over the next decade. The card network will still be present, but most people use their cards via a mobile wallet.

This provides a lot of integration possibilities, especially those around BNPL. While most people use BNPL for online sales, retailers could likely integrate it with wallets to offer new ways for customers to instantly use it when buying at a retail location.

BNPL is available at retail locations but can slow down the checkout process considerably. Advances in open banking and new mobile wallet technology, such as super wallets, will help usher in this new type of instant retail credit.

How Merchants Can Get on Board With The Future of Payments

To accept the latest digital payment trends, merchants need a trusted technology partner to turn to.

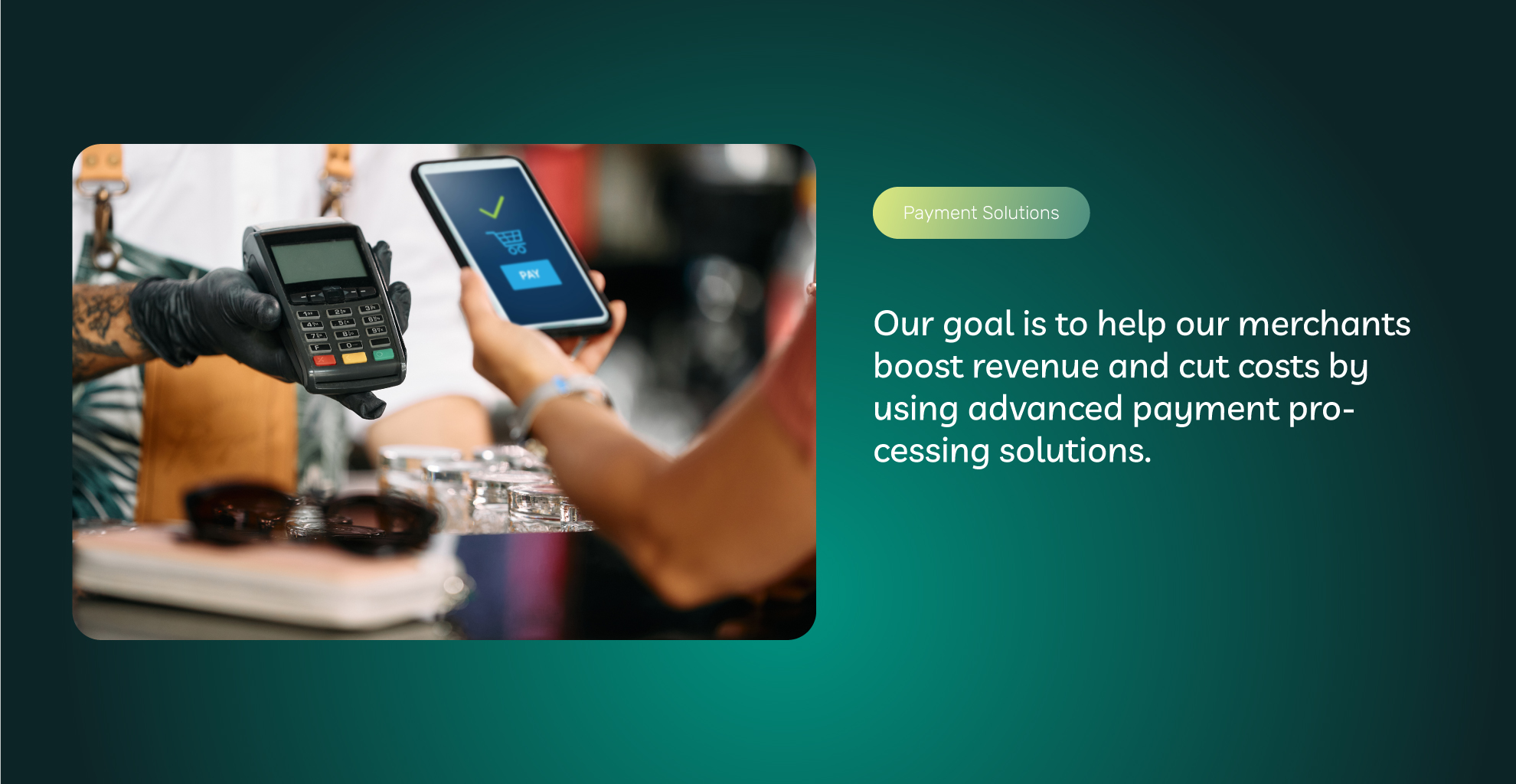

At ECS Payments, we are at the forefront of innovative payment solutions that use the latest technology available in the digital payment space. Our goal is to help our merchants boost revenue and cut costs by using advanced payment processing solutions.

Contact ECS Payments today to learn more about the latest digital payment solutions designed to help our business succeed.

Frequently Asked Questions About The Future of Payment Processing

The future of payments is evolving rapidly with technological advancements like digital wallets, tap-to-pay, CBDCs, and cryptocurrency.

To stay ahead of payment trends, businesses should adapt to new payment technologies as soon as possible. Even if consumers aren’t using these technologies en masse, they will eventually, and you will already be prepared. ECS Payments offers the latest payment solutions to ensure your business can effectively embrace these innovations and stay competitive within your market.

Not all businesses need to change their payment processing solutions to accept the latest payment trends. The future of payments is exciting. However, your business might fare perfectly well without the need to accept cryptocurrency, etc. To see what type of payment solutions would best benefit your business, contact ECS today, and one of our knowledgeable representatives will be happy to assist.

53% of consumers prefer to use digital wallets. They are far more convenient and secure than traditional payment methods. Almost every consumer always has their smartphone on them. With their wallet digitally attached, providing digital wallet payment options is a no-brainer. Contact ECS Payments to get your NFC payment terminal today to ensure your business caters to the growing demand for this convenient payment method.