Consumer trends in digital payments have changed drastically over the past few years. Customers these days expect to have different options when paying electronically. In fact, most expect to be able to pay digitally everywhere they go whether they are in a retail store or even when they are out at an event. In some of these cases, stationary terminals are not an option. This is where wireless credit card processing comes into play.

Customers also want to be able to pay electronically when certain service providers arrive at the customer’s locations, for example, for home repairs or other services that require payment upon completion.

Many of these services require wireless credit card processing, which essentially means credit card processing without being hardwired to a computer or internet service.

Adding wireless credit card processing makes it easy for businesses to expand their offerings and give themselves a competitive edge in a crowded market.

Below, we’ll explain exactly how wireless credit card processing works and the benefits it can bring to your business.

What Is Wireless Credit Card Processing

Credit card processing is likely already a central part of your business. Traditional credit card processing terminals use a card reader or terminal device to capture card data when customers pay for a purchase.

A Point of Sale system (POS) or a network cable physically attaches the card reader to the internet. When connected to a POS system, the POS system provides the physical connection to the internet.

Both cases require a physical connection to the internet to transmit the card data to the payment gateway for processing.

Wireless terminal credit card machines do not require a physical internet connection. Sometimes, the wireless card machines also don’t require a connection to other devices.

Wireless card readers or mobile devices handle the connection to the internet. This can be over the cellular network, such as 4G or 5G. The connection can also be via a secure Wi-Fi signal if one is available.

Small business credit card machines like these, wireless or mobile, offer businesses the flexibility to accept more types of payments to help grow their business.

How Does Wireless Credit Card Processing Work?

Wireless credit card processing works similarly to the traditional credit card processing. However, instead of transmitting customer card data over your wired terminal or POS system, it travels via Wi-Fi or the cellular network.

The essential customer experience has not changed, but wireless connectivity does give customers and businesses more options for accepting cards.

Below are the full steps for a wireless credit card transaction using a credit or debit card as a form of payment.

Card Capture

To begin, a wireless card reader or mobile card reader will accept the customer’s credit or debit card. The payment gateway sends the data to your payment processor for initial fraud checks.

Most modern EMV readers no longer use magnet stripes, although the card readers still have this capability for other purposes.

Authorization

The payment gateway will then return a message that the card is valid and has passed the initial fraud checks. The wireless process operates at virtually the same speed as a non-wireless transaction, ensuring that it does not negatively impact the customer experience in any way.

Batch Processing

Traditional processing generally stores transactions and then processes them together at certain intervals to save time. Wireless processing allows combining both traditional and wireless transactions in a batch.

Settlement

After batch processing, the system charges the issuing banks. The issuing bank is the financial institution that the card originated from. Then, the business’s merchant account receives the funds.

Clearing

The issuing bank then does its final fraud checks and determines available funds. The clearing generally takes about two days in most cases. Generally, the funds are available immediately after that.

At this stage, the merchant’s payment processor will deduct any fees associated with the different transactions, including any rolling reserves, depending on the merchant agreement. The next step deposits the total into the merchant account of the business.

Using wireless credit card processing will help most businesses get paid faster. Funds usually take about two days to reach the merchant’s account.

Benefits Of Wireless Credit Card Processing

Wireless credit card processing has many benefits, some of which may not be apparent at first glance. However, upon further inspections, you begin to realize how important they are and how they can help a business grow and streamline its operations simultaneously.

Faster Checkout

One important benefit of wireless credit card processing is how it can speed up the checkout process for many businesses.

For example, servers can bring wireless card readers to different tables to accept payments in a restaurant setting. This helps to avoid long lines at a stationary checkout area during busy periods.

Wireless payment systems are commonly used in restaurants that have both indoor and temporary outdoor dining areas. They offer the convenience of setting up a dedicated wireless checkout station outdoors when required.

This flexibility means you can still rely on a traditional stationary checkout indoors, but you have the option to use wireless solutions during busy periods or for special events.

Flexible mobile and stationary payment options can also work for larger retail establishments where salespeople wander the floor to work with customers. With wireless card processing, transactions can be completed where the salesperson and the customer happen to be. There’s no need to walk back to a checkout area.

Close Sales

If you work with leads or sales, you know how important it is to have almost zero friction when closing a sale or locking in a downpayment. In this regard, wireless card processing enables you to secure a down payment or full payment as soon as you make the deal, especially if you are meeting with a lead outside the office or during a business trip.

Without this ability, you would need to send the lead an invoice or have them call or visit a website to make the payment. Those options take time and allow the lead to have second thoughts or not follow through.

Having the ability to capture a payment right on the spot helps to close more deals. That means your cost to acquire new customers is lower, and your conversion rate increases.

Expand a business

Wireless credit card processing allows you to expand your business beyond its physical location. If you’re in retail, you can take advantage of other places to sell your goods, such as events or pop-up stores.

You can sell your items outside your location for restaurants or cafes, such as food truck pods or other community areas reserved for alternative restaurant options.

There are many ways that accepting payments outside of your business location can help you find new income streams and easily grow your revenue. This type of outreach also helps you build your brand to a wider audience and attract new customers.

Provide Mobile Services

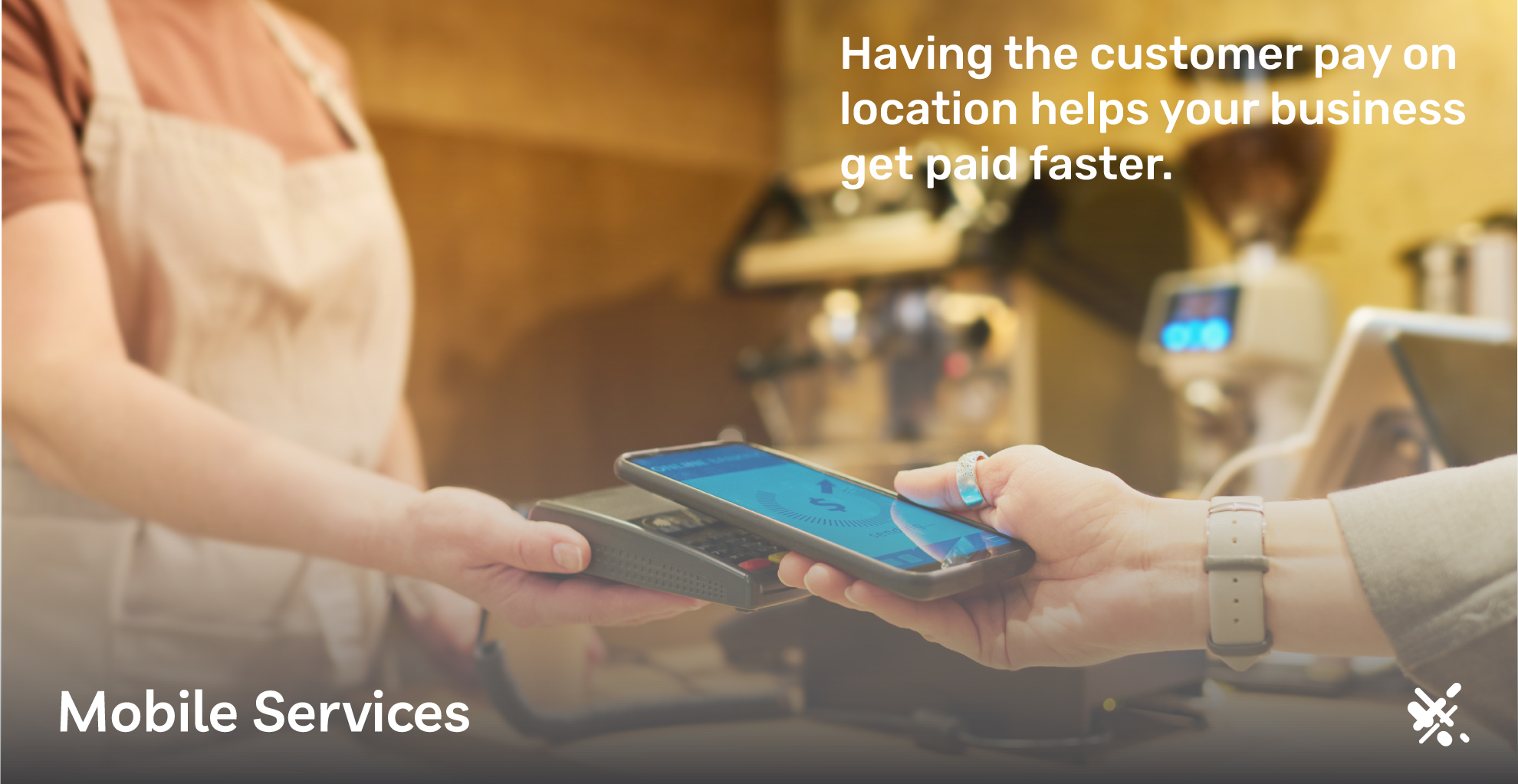

Mobile services have grown in popularity in recent years, and having wireless and mobile payment options helps your business add these services. Having the customer pay on location helps your business get paid faster.

Improved Appearance

If you choose not to do any business outside of your physical location, being able to implement wireless processing still has benefits. One benefit is that it gives you a cleaner and tidier checkout area.

Instead of cables and wires running to and from your POS system, you can have a sleek setup that looks more modern and appealing. Clean and modern payment areas can be especially important if you’re in a trendy industry. Your customers will appreciate the sleeker look of your checkout area that isn’t cluttered with cables and wires.

Tidiness can also be important in settings such as a food truck. In these situations, workers often move the payment terminal. With a wireless card reader, this is much easier and prevents a lot of clutter in small retail settings, such as a food truck or cafe.

Start A Business Without A Physical Location

Starting a business can be difficult, mostly due to the startup capital involved. Renting and furnishing a storefront for the business contribute significantly to this cost. Many entrepreneurs have bypassed this expense by using pop-up locations and other innovative ideas to start businesses that don’t have a physical location.

Wireless and mobile credit card processing makes this possible for anyone with a great idea but may not have the startup funding needed to open a physical store.

If you have a great idea or product, you can start selling it immediately by taking advantage of wireless and mobile credit card processing.

Wireless Credit Card Processing vs. Mobile Credit Card Processing

People often interchange the terms wireless credit card processing and mobile credit card processing. Both wireless credit card processing and mobile credit card processing do indeed have overlapping features. However, there are some differences that merchants should be aware of between these two methods for capturing card data and running transactions.

With wireless credit card processing for small businesses, there is a wireless credit card terminal where the customer will physically present their card. They use the reader just as they would if purchasing at a physical retail location, like a storefront.

The difference is that the reader can work anywhere with Wi-Fi or an adequate cellular signal. Sometimes, the reader can save the data even if there is no signal.

With mobile credit card processing, the business generally uses a device they already own, such as a smartphone or tablet. The business downloads an app from their payment processor or payment gateway, enabling them to run credit card transactions from that device.

In these cases, users manually enter the card data. This is similar to a virtual terminal that many online businesses use when taking credit card orders by phone. The customer service representative will take the credit card information over the phone and input it into the software for processing.

Some newer apps now enable the device’s camera to capture card information, just like many banks offer mobile check deposits through their apps. The app takes a photo of the check, and the software can read the routing, account numbers, and the amount.

Cost Differences

All transactions will have processing fees, which can be different for wireless and mobile transactions. Of course, this will depend on your specific merchant agreement. Still, mobile processing will generally have higher transaction fees if you manually enter the card number into a smartphone or device.

With wireless card processing, where you use a terminal to capture card data, the fees will be similar to what you pay for your traditional processing.

Is Wireless Credit Card Processing Safe?

Many merchants hesitate to implement wireless or mobile credit processing because they fear the technology may not be as secure as a hardwired connection. While it’s true that wireless technology can have security risks, they are not higher than other forms of processing you already do.

Using security best practices recommended by credit card companies and wireless hardware manufacturers can easily mitigate most risks.

Another area of concern is PCI DSS (The Payment Card Industry Data Security Standard) compliance. PCI DSS is a set of security and data handling practices put forth by banks and financial institutions involved in credit card processing. To comply with their merchant agreement, merchants must follow these standards.

When properly implemented and when using approved hardware, wireless credit card processing and mobile processing are both fully PCI DSS compliant.

Wireless Credit Card Processing Security Tips

Below, we’ll offer some tips to help make sure your wireless and mobile processing is safe and secure.

Ensure All Devices Are Up To Date

Hardware and software vendors both regularly provide updates for their mobile payment terminals. It’s important to check for these updates regularly so your devices and software are always up to date, including any computers, smartphones, or tablets in your processing workflow.

Most of these devices will have settings to make them update automatically. It’s best to enable these features since updates are generally security-related.

Use The Latest Wi-Fi Encryption

You’ll likely use Wi-Fi with any of your wireless credit card processing devices within your business. Most of the time, these devices enable built-in encryption by default.

However, users can generally choose between different encryption methods and levels. Avoid WEP-based encryption as it is outdated and no longer secure. If your router only offers WEP, you must upgrade to a more recent model.

WPA2 and WPA3 encryption are both recommended. WPA3 is newer, but you can still use WPA2 if your devices don’t support the newer protocol.

You can change all these settings by accessing your router’s dashboard and configuration settings.

Only Connect To Trusted Networks

You may have to use public Wi-Fi at an event or location when using mobile credit card processing. Always confirm the Wi-Fi is safe before connecting any device. Hackers may try to set up fake Wi-Fi hotspots using common names to trick users.

So always confirm the Wi-Fi name with the location you are at. Don’t randomly connect to Wi-Fi that happens to be available.

Choosing a Wireless Credit Card Processing Solution

Adding wireless or mobile processing to your current payment processing may seem overwhelming, considering new hardware and software exist to implement. But it is very straightforward as long as you follow a few simple steps when choosing the best options.

Decide On Your Goals

It would be best to always base business decisions on goals, and choosing a wireless processing solution is no different. First, decide what you want to accomplish and what you need your new processing to do to help you reach your goals.

Earlier, we mentioned many of the benefits of wireless credit card processing, and that can be a great start. For example, look into mobile processing solutions if you want to start taking your products or services directly to customers.

If you want to add new checkout areas that are more flexible for your current retail locations, you will want more wireless options to help you add those without needing extra cabling.

You’ll also want to consider the future and your business’s future in a few years. If you see yourself expanding into other areas that require both of these technologies, then it’s best to start implementing them now.

Choose A Payment Processor

Not all payment processors can help you set up wireless or mobile processing. Some credit card processors have limited knowledge or do not offer the hardware and software solutions your business needs.

ECS Payments is a leader in wireless and mobile processing, and we have in-house experts who can help you determine the best merchant services for your business.

As payment technology rapidly changes, it’s important to have a payment processor that is a trusted technology partner that helps you leverage new technology to maximize your business’s revenue potential.

Hardware

You’ll likely need new hardware, such as wireless credit card processing terminals. There are many options in this regard, and your payment processor should be able to walk you through which will fit your requirements.

It’s important to consider compatibility when choosing new hardware. For example, depending on the POS system you currently use, specific wireless hardware may work best with that system.

EMV readers, an acronym for Europay, Mastercard, and Visa, are the most recent readers available. These readers have the latest protocols to accept various contactless and chip payment methods.

Buy or Lease

Most payment processors offer options to buy or lease your new hardware. Both have benefits and downsides, and you should consider which is best for your situation.

With leasing, you will have lower initial costs than buying the hardware outright. Lower costs can be beneficial for newer businesses already dealing with high startup costs and need funds for other areas of the business. Leasing will also generally offer regular hardware upgrades.

You trade in your existing hardware for the latest models at regular intervals, keeping your technology fresh and up to date. The downside is that you will generally pay more over time than just purchasing the hardware outright.

One thing to also be aware of is the leasing contracts and the terms involved. Some leasing contracts for payment processing hardware can be unusually long, lasting for years. They can also have automatic renewal clauses that may not be apparent when first signing.

Another area of leasing contracts to be aware of is early cancellation fees. If you decide to terminate the lease, look at what your fees and penalties will be. Leasing can be an option for some business owners, but always carefully read the contract and ask questions before signing the dotted line.

Mobile Processing

Mobile processing will have a few options to consider. Since mobile options can work on your existing devices, you may want to explore those options first.

You can achieve this by using the app supplied by your payment processor or payment gateway. You first install the app on your smartphone or other devices. You then log in to the app with your supplied credentials, which may be the same as your payment gateway.

For some situations, this may be enough for you. You’ll have to manually enter the credit card information when using the mobile app.

There is additional hardware to make these mobile solutions work more like wireless credit card readers. You can use additional dongles that connect to the smartphone or tablet to capture card data.

There are also readers that work via Bluetooth to connect to the device you have the processing app installed.

Depending on your situation, either technology may work best for you. You’ll want a device to capture card information for those selling retail items from a mobile location, like a pop-up store or food truck.

Customers are familiar with this workflow, and your checkout process will be much faster.

Salespeople or service representatives who visit customers or clients directly may not need these payment options. For these situations, manually entering credit card information may be all that is required.

Research Processing Fees

Different processing methods and ways of capturing card information can all impact your processing fees. Depending on the type of transaction, different fee structures can apply to wireless and mobile processing.

Confirm with your payment processor what your new fee structure will be and what you can do to lower those fees or get better rates. Sometimes, using a different method of card capture when mobile can reduce your fees.

For example, manual entry of credit card information, such as with a virtual terminal, is a card-not-present transaction. These typically charge higher base rate fees than when the card is present.

The amount of your average transaction can also play a role. For example, you may want to require a signature with larger purchases. Another example is if you accept tips, you may then want a signature depending on your checkout procedures.

Additional Hardware

Depending on your business, you may have a few extra items. In most cases, a receipt printer will be an integral part of the payment processing. These are also available in wireless versions with wireless card terminals.

These come in various formats to fit your business, so choose accordingly based on your needs.

Next are things such as barcode scanners. Barcode scanners are part of an overall POS system and are used to scan products upon checkout. These also help to take advantage of most POS systems’ built-in inventory tracking.

Finally, some businesses may require these for ID or age verification. So, in some cases, it may be mandatory.

More Information About Wireless Credit Card Processing.

For any business, the benefits of accepting credit card payments far outweigh any costs involved. This holds true for wireless and mobile processing as well. Adding these inexpensive options provides a strong ROI for businesses in almost any industry.

If you want to add wireless payment processing to your current payment workflow, contact ECS Payments. We offer the latest payment solutions, including wireless and mobile options to fit any business.

Contact ECS Payments today to learn more about wireless and mobile processing.

Frequently Asked Questions About Wireless Credit Card Processing

Wireless credit card processing is a method of accepting credit card payments without being hardwired to a computer or internet line. It uses mobile devices or wireless card terminals to connect to the internet via secure Wi-Fi or cellular networks.

Wireless credit card processing optimizes the checkout experience and the flexibility of your business. Checkout is faster, you can accept payments at various locations, and you can even start a business without a physical location or take your business on the go. ECS Payments can help you implement wireless credit card processing solutions at your business so you can streamline your operations and offer a more convenient payment experience to your customers.

Wireless credit card processing involves a wireless card terminal, and the data can be transmitted anywhere with secure Wi-Fi or with its own cellular signal. Mobile processing often uses a smartphone or tablet with an application provided by the payment processor where card data is captured manually on the application or virtual terminal. ECS Payments offers solutions for both wireless and mobile credit card processing. Contact us today to get started and see which option is the best fit for you.

Security risks for wireless credit card processing are not higher than other forms of processing if proper security measures are in place. To ensure security, it’s essential to keep all devices and software up to date, use the latest encryptions, and only connect to trusted networks and private Wi-Fi. PCI DSS compliance is crucial. Contact ECS Payments to learn more about how you can become PCI compliant and keep your customer data safe.