If you checked your bank account right now and saw 5% of your money had vanished, I am sure you would investigate the cause immediately. Unfortunately, many growing merchants face this loss daily in their processing statements, often without realizing it.

Treating merchant services as a set-and-forget utility leaves profits to slowly leak from your business. Unlike utility bills, your expenses on electronic transactions do not have to be static. If managed properly, you can actually use them as a lever for growth. Regular reviews let you move beyond surface transaction fees to uncover strategic advantage and reveal transaction failures or customer friction points.

If you have never performed a payments review before, don’t panic; the first steps are simpler than you might imagine. And we’re breaking down what you need to know.

Why Payments Deserve a Quarterly Strategic Discussion

Don’t treat your payment setup as a one-time project. Many owners think this box is checked when they launch. However, consumer behavior and financial technology change faster than most service contracts.

A quarterly payments review should be a regular, strategic conversation. Your business changes every quarter—maybe you’ve added products or your average order value has shifted. Each change affects your risk and processing costs.

By committing to regular payments reviews, you create a space to reveal hidden revenue and significant savings. This is not to encourage haggling over basis points with a provider; instead, focus on identifying inefficiencies in your business. For example, a spike in “Do Not Honor” codes may signal a technical issue or a shift in how banks view your transactions. Or, if you have a majority of debit transactions, you can take advantage of interchange pricing over flat rates. Catch these trends early to reduce risk and improve cash flow health.

Call For A Team Meeting

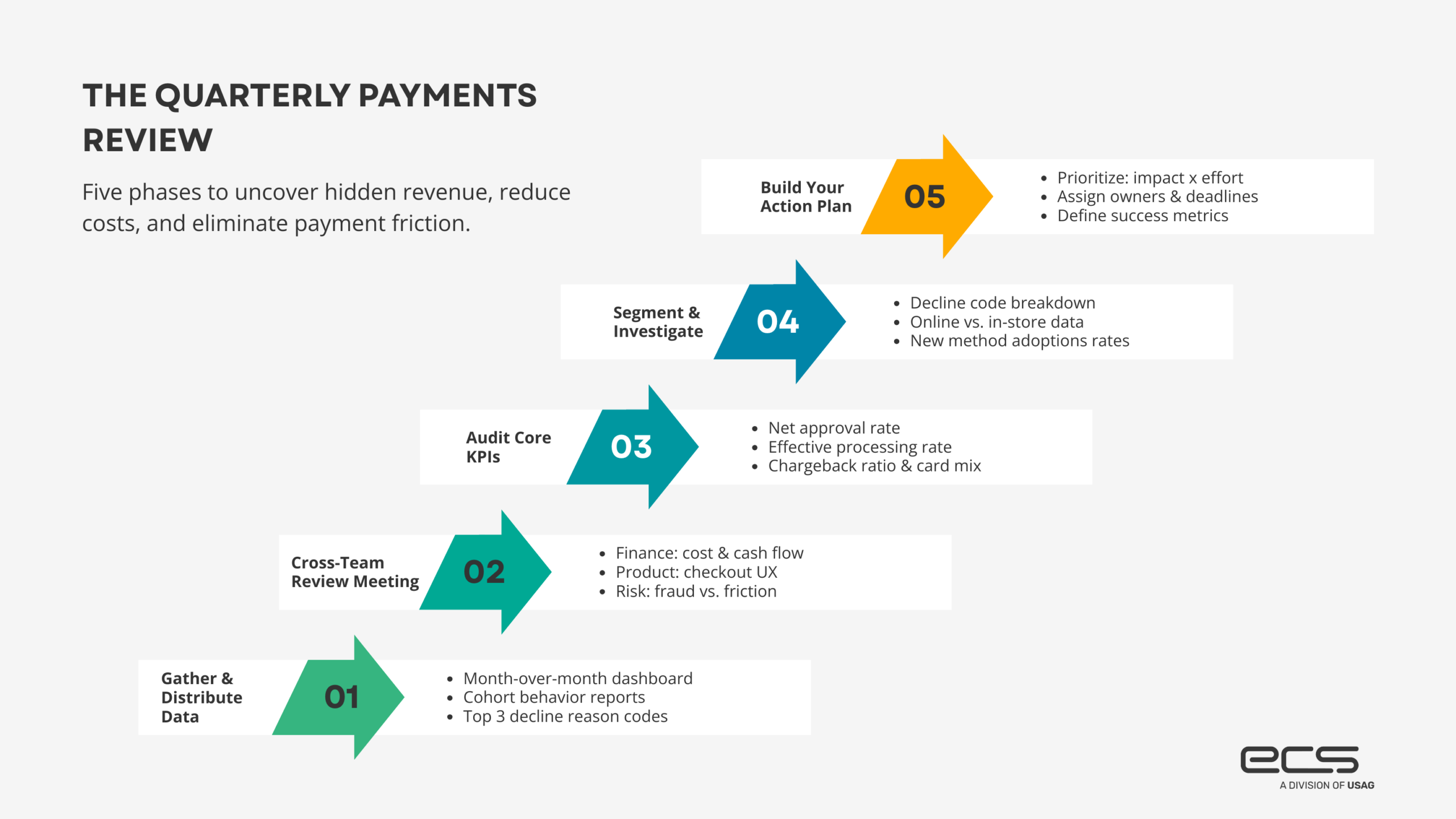

A truly effective payments review requires more than a glance from an accountant. Payments touch all operations, so adopt a cross-functional perspective. Finance tracks the bottom line and cost of capital. Product and operations teams provide essential context on the customer journey.

You cannot have a meaningful conversation without clean data. To ensure all relevant departments are engaged, prepare and distribute a brief summary of the previous quarter’s payment data ahead of time. This allows everyone to arrive informed and gives department heads the necessary time to correlate payment trends with their own internal metrics, such as marketing spend or customer service tickets.

These pre-read materials should include a dashboard showing month-over-month trends along with a cohort report on how different customer groups behave. By identifying your top three reason codes for transaction declines and establishing this initial baseline, you gain a clear picture of where your money is getting stuck before the discussion even begins. This level of preparation transforms the meeting from a simple data review into a proactive session focused on payments optimization.

Product managers: can explain if a new checkout feature caused a dip in conversions

Operations: can highlight if shipping delays increase disputes.

Risk and fraud specialists: may find that overly rigid security settings deter legitimate customers.

When these teams collaborate in a review, they stop working in silos and start viewing payments as a collective tool for scaling. Each team uses insights differently, but the goal remains the same: make the payment process as frictionless as possible.

The Standard Agenda for a Quarterly Payments Review

To keep these meetings productive and avoid getting lost in a sea of spreadsheets, follow a consistent agenda. You should begin by reviewing your core key performance indicators (KPIs). This includes your total processing volume, your overall approval rates, and your chargeback ratios.

If you have limited resources or time for analysis, prioritize your Net Approval Rate and your Effective Processing Rate above all else. You can use these two metrics to quickly tell how many of your attempted sales are actually settling and exactly what percentage of your gross revenue is being consumed by fees.

According to data from the Federal Reserve, consumer payment choice is constantly shifting between debit, credit, and cash, which means your volume by card type can strongly influence your blended rate. After the high-level numbers, highlight notable trends or anomalies. If your approval rate dropped two percent last month, investigate the “why.” Was it a specific card brand or region? Incorporate customer feedback; if support hears mobile checkout is confusing, adjust your payments strategy to prioritize mobile optimization.

Tools and Reports to Support the Review

One of the most powerful tools is decline code analysis. This report breaks down why transactions fail: insufficient funds, expired cards, or suspected fraud.

For small businesses looking to streamline data analysis, we recommend using the integrated reporting dashboards provided by your merchant service provider rather than building custom solutions. These platforms are designed to aggregate multi-channel data into a single view, which saves your team hours of manual reconciliation. If your merchant service provider does not offer these tools, ECS Payments has designed its proprietary dashboard to help merchants find all their reports in one central location.

The data supports this need for efficiency, as labor remains the single largest expense for most companies, consuming 70% of business spending. When you automate your reporting, you protect your most expensive resource: your team’s time. Forbes Advisor highlights that while technology is evolving, a significant gap remains in how small businesses utilize digital tools. In their report on Small Business Statistics 2024, they reveal that nearly one in three businesses still operate without a website, and many continue to struggle with the manual costs of inventory and labor.

For a professional quarterly business review payments session, a modern processor that delivers easy-to-digest reports is essential. Spending hours manually exporting and cleaning data in Excel wastes time that you should be using on strategy. By leveraging a platform that integrates your e-commerce and brick-and-mortar data, you avoid the common pitfall of running out of capital, the reason 29% of small businesses fail, by keeping a real-time pulse on your cash flow and processing efficiency.

Deep-Dive Sections to Include in Your Analysis

Once you cover the basics, review specific payment methods. If you recently added Apple Pay or “Buy Now, Pay Later,” check if those changes grew your pie or just shifted existing customers. Focus on adoption rates; If a new method has low uptake, it may be due to poor placement in the checkout flow, where customers cannot easily select it, or it may simply not be relevant to your specific customer demographic.

Another deep dive involves segmenting performance by channel. For merchants with both e-commerce and brick-and-mortar stores, data often tells two different stories. Physical locations may have high approval rates but hardware challenges, while online stores may face more fraud. By segmenting data, you can fix specific problems rather than implement broad changes.

Turning Findings into an Action Plan

A payments review is only as valuable as the actions taken. After identifying opportunities, prioritize them by (1) impact and (2) effort needed. For example, review whether insights need a system overhaul or a simple change, such as updating your payment descriptor to reduce “unrecognized transaction” chargebacks.

Once priorities are set, assign clear owners and timelines. If you find high international fees, assign finance to investigate regional routing. If mobile checkout lags, set a product deadline to improve it. Define success metrics for each action and set targets to hit by the next meeting.

ECS Payments: Your Partner in Professional Payment Reviews

Executing a sophisticated payments strategy depends on your partner. ECS Payments is a trusted partner to merchants across the U.S. We don’t just provide merchant accounts; our goal is to help merchants become strategic in their payments. Many large processors use a one-size-fits-all approach and offer only generic help desk support, while we emphasize the human element and real relationships.

When comparing ECS Payments to other processors, growing businesses find that our pricing models are specifically built to scale with you rather than penalizing you for increased volume. Unlike larger competitors who often hide fees in complex tiered structures or oversimplified flat rates, we offer transparent Interchange Plus pricing and personalized account management. This means you have a direct point of contact to help you interpret your data during your payments performance review, ensuring you never have to navigate a complex financial shift alone.

We know an effective payments optimization plan requires a true understanding of your business model. ECS Payments offers robust reporting and transparent pricing. Growing merchants need these to conduct an honest payments review. Our platform provides the granular detail needed to spot trends before they become problems.

If you are tired of feeling like just another number, switching to ECS Payments brings the insight and support you need to grow your revenue. We stand as a strong alternative to “black box” processors. We give you the keys to your own data and provide expert guidance to interpret it.

Building a Framework of Continuous Payments Optimization

The most successful merchants treat payments optimization as a journey. This means using insights from your quarterly meetings in your broader product and pricing plans. If data shows customers prefer a payment method, use that insight to influence your product marketing and site design.

Make it a habit to track the impact of past actions in every subsequent payments review. If you implemented a new fraud filter last quarter, did it actually reduce chargebacks without hurting your legitimate sales?

By closing the loop on these decisions, you build a culture of accountability and data-driven growth. According to the U.S. Small Business Administration, staying on top of financial health and efficient operations is a primary driver of long-term viability. Their resources on managing a business emphasize the importance of regular internal audits and reviews.

Take Control of Your Financial Future

Running a business is complicated enough without worrying whether your payment processor is holding you back. A dedicated payments review is the single most effective way to ensure that your money is working as hard as you are. By bringing the right people together, analyzing the right data, and taking firm action, you can turn a mundane administrative task into a powerful engine of profitability.

Do not wait until a major issue arises to look under the hood of your merchant services. You can start optimizing your bottom line today by evaluating your current performance and identifying hidden revenue gaps.

If you are ready to see what a professional, data-based approach can do for your business, reach out to ECS Payments for a free audit. We will help you analyze your current statements, identify areas for payments optimization, and show you exactly how much more efficient your processing could be. It is time to stop guessing and start growing.