Do you own a brick-and-mortar business? What types of in-person payments should you accept? We’re going to be like that one family member who always ruins the football game you’re taping during get-togethers: all of them. If you want to watch the play-by-play, read on.

Cash: The OG In-Person Payment Option

OG stands for “original gangsta.” Cash is obviously the oldest payment process among all your choices (hence, our accolade). These transactions are the simplest for in-person payments: the customer hands you cash, and you hand over the goods or services.

But is it really that simple? You’ll have to take all that cash to the bank. If you don’t, you run the risk of attracting crime. Cash-heavy businesses like convenience stores. For instance, many marijuana dispensaries rely on cash payments because they face certain regulatory hurdles in accepting credit cards—and consequently face an increase in armed robberies.

Some cash-heavy businesses attempt to circumvent this issue by posing signage like “only $100 is kept in the register” or “employees do not have the code to the safe.” But there are other types of crime aside from violent armed robberies, like money laundering.

It is not uncommon for money laundering to occur without the business owner’s knowledge. An employee inside the business (like a manager or accountant) can be the point person for hiding illicit funds. For instance, in the food business, it is easy to fudge the numbers because reconciling sales and inventory is complicated.

Should My Business Accept Cash Payments?

Cash is undeniably a form of payment that is on its way out. As of 2022, 40% of polled Americans did not use cash for any weekly transactions. The average amount of cash carried by an American consumer was $67.

Most studies point to a trend of fewer consumers carrying less cash. And yet, a significant portion of the population is unbanked (6%) and relies exclusively on cash. Moreover, certain segments of the population (such as Boomers) still carry cash and will use it.

Significant consumer backlash is also building against the idea of a cashless economy. Are these ideological trends something you should pay attention to vis-a-vis the types of payments you accept at your business?

Accepting cash is still a good idea for in-person payment for most businesses, especially brick-and-mortars. There is always the unexpected customer who only has cash. Cash is also one of the best pop-up payment methods for fairs, festivals, and other events with potentially poor wifi connectivity.

Cash payments are also good for businesses with a high volume of low-ticket transactions, like convenience stores, bars, or coffee shops. Just remember to put safeguards in place. Empty your tills regularly, have cameras up, and post signage that discourages potential crime.

Checks: The Other Paper Payments

Checks are one of the most fascinating innovations in banking history. Emerging in the Middle Ages, they essentially allow someone to take a slip of signed paper somewhere and collect the amount of money written on the check.

As amazing as that is, letting customers pay with checks has some drawbacks. For starters, checks can bounce. In addition to the cascade of fees resulting from a bounced check, you will also have to chase down the customer’s payment.

Checks also need to be brought to the bank. However, some banks offer mobile banking apps that allow you to snap a picture of the check. In addition to the fact that this particular depositing method takes more time to process, not every financial institution provides mobile banking. If you use a local bank, like most small business owners, you may have to bring your checks in.

Paper checks are also becoming an extreme rarity among consumers. Less than 4% of consumer transactions are paid for with checks. Check payments have a relatively high average dollar value of $300 per transaction. These findings indicate that checks are not used for everyday purchases but more commonly for large periodic payments like taxes, tuition, utilities, housing, and debt payments.

Should My Business Accept Checks?

This question is somewhat polar opposite to the question of cash payment methods. If your business has many low-ticket transactions, you should not accept checks; if you do, you should not advertise it.

If you’ve got hundreds of transactions per day, you don’t want to deal with running down one bad check. Many businesses in the high-volume bracket have learned this the hard way. For instance, you’ll see many grocery stores and restaurants with signage posted that they do not accept personal checks.

Some types of businesses should accept checks. If you provide B2B services, checks are a safe bet. They may even be the preferred way of making payments for your clients since they can be mailed in response to an invoice. Checks can also be a preferred way of payment for large purchases because they have a substantial paper trail.

Car dealers, real estate investors, consultants, and lawyers—accepting checks is a good idea and perhaps even required in your industry. Asking for or accepting checks in these types of relationships is not a burden to the customer or client. It is if they are trying to buy a coffee—for them, for you, and everyone else in line while they’re writing the check.

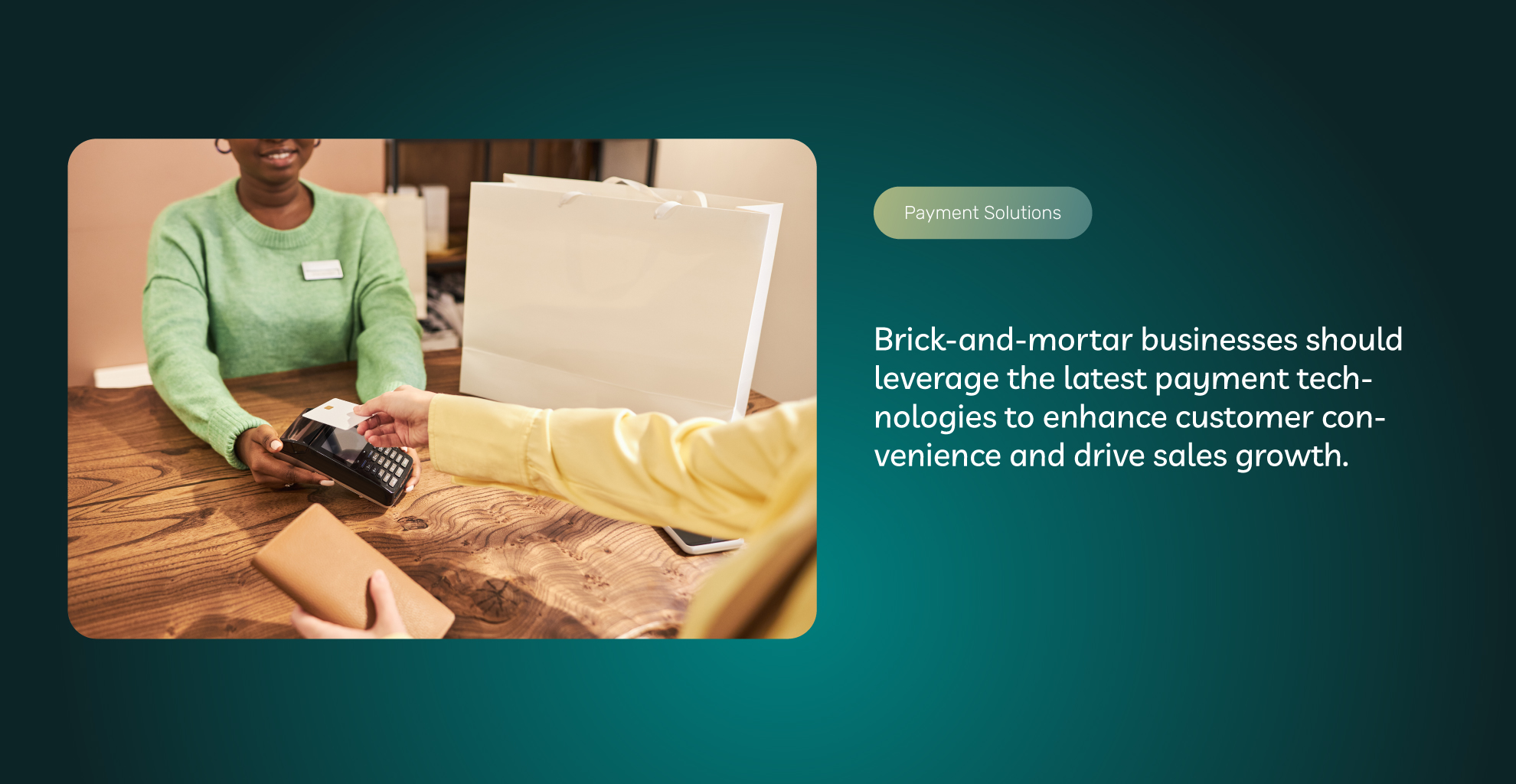

Debit and Credit Payments

Debit and credit cards undoubtedly stand out as the primary methods of payment for American consumers for both online and in-person payment. Around 40% of in-store payments are made with credit cards, and 31% are made with debit cards, far outstripping other payment modalities like digital wallets (12%) or cash (12%).

Most card issuers are shifting toward contactless payments. Mastercard and Visa will phase out the magnetic strip by 2035. EMV chips have long been popular in Europe but will probably have a short-lived reign in the U.S.

That’s because customers using plastic cards will simply wave their card over the card reader and complete the payment with radio wave technology. This technology uses small antennas built into the card to exchange encrypted payment information securely and rapidly.

Should My Business Accept Credit and Debit Cards?

This is an absolute yes. For starters, credit and debit cards are by far the most popular method of payment among consumers. Studies also show that customers may spend 160% more with plastic than they would with cash. Not only does accepting credit cards open you up to more business, it can likely increase the size of every transaction.

Of course, there are some downsides to accepting credit cards. One is that you need a payment system. This includes the hardware of a point-of-sale system and the software to animate and direct the hardware. A payment processor can provide and service both hardware and software. However, the processor will obviously charge you transaction fees.

Like any other decision you make over a business day, you must weigh the pros and cons and act accordingly. Does paying a small fee on every transaction mean it’s better to only take cash and check? Probably not. All the statistics cited above suggest you would lose a decent amount of business if you didn’t accept credit and debit card payments.

The ACH Alternative

The truth is, every business should take credit cards as a matter of customer convenience. However, some businesses that collect large recurring payments may want to offer ACH payments as an alternative. ACH payments are similar to money transfers in that bank account numbers are used to transfer funds from the customer’s bank to your bank.

Landlords, schools, insurance agencies, and utility companies are a few examples of organizations that charge their customers a fixed amount every month. These charges have been agreed upon beforehand, so the convenience offered by plastic payments is less important.

In fact, many of these payments (rent, tuition, life insurance, electric bills) are put on autopilot. It doesn’t take much for the customer to enter their checking account info once and put these payments on autopilot.

ACH payments are good for businesses because their processing fees are much lower. The average ACH payment costs about $0.30, versus 2-3% for card payments. However, keep in mind that many of these businesses are not collecting in-person payments.

Requesting customers to input checking and account numbers is too burdensome to do in person, especially in high (or even medium) volume sales. However, there are still some in-person situations that would merit collecting ACH info over card numbers.

Signing a lease, setting up an insurance policy, and signing a tuition agreement are a few examples of in-person payments where it is not cumbersome to ask for a paper check or for the customer to fill out an ACH form. For everything else, there’s Mastercard (Visa, Discover, and American Express).

P2P

What is person-to-person payment or P2P payments? Think of PayPal, Venmo, and Zelle. These applications allow one person to send another person money right from their phone. Can businesses use P2P technology to collect payments? Yes, they can. Should they? No.

P2P payments are easy to use and often instantaneous. They are not bad solutions for retailers with a very low sales volume (e.g., someone selling handmade soaps out of their garage) or independent contractors (e.g., web designers). However, they are not good for businesses with higher sales volumes or those that need to maintain more professional standards.

Would you like your doctor to request a copay via Zelle? Probably not. For starters, it seems too casual. Then there’s the potential for lots of HIPAA violations. What if your Zelle is sent to a joint account, and their spouse sees you are paying for (insert embarrassing thing in the notes)?

From the seller’s perspective, P2P applications have abominable fees. Take Venmo, for instance. They charge 3% of credit card payments and 3.49% + $0.49 on payments made with Venmo. These fees merit screaming “blasphemy” and tossing leatherbound books on alchemy into a large bonfire (e.g., they are not good).

Part of the problem is that P2P applications tend to charge flat-rate fees, which do not reflect the true cost of running a transaction. All card brands, Visa, Mastercard, Amex, and Discover, all charge different fees.

Credit and debit cards trigger different fees. Asking 3.5% AND two quarters on every transaction is okay when you’re just starting out, but it’s too much when you’ve reached a normative sales volume.

Digital Wallets

Our last payment modality is digital wallets. Digital wallets facilitate credit and debit card payments. However, the difference is that these cards are “uploaded” into a mobile device application (like ApplePay).

The customer does not need to present their card when they check out. They simply take out their phone and unlock the wallet with a biometric indicator (face scan or thumbprint) or inputting a passcode. They can then wave the phone over the payment terminal just like they would with a contactless card.

Digital wallet usage is on the rise. The survey above about card use also cited that digital wallets comprised 3% of consumer transactions in 2017. But less than a decade later, that number has already quadrupled.

While the use of actual (plastic) credit and debit cards still leads the way, there is a decent chance of mobile wallets eclipsing actual card usage in the future. Even if it remains a third choice (behind plastic payments), a significant percentage of your customers will be using them, especially younger consumers.

So…What Walk In Payment System Should I Use?

How to choose in-person payment methods depends on what you’re selling and your customer base. There is no one-size-fits-all answer. However, most businesses would benefit from accepting as many forms of payment as possible.

A good payment processor will be able to help you accept all non-cash payments (check, card, ACH, and digital wallets). For in-person transactions, you can probably skip P2P payments, but you should still probably accept cash.

Find out more about how ECS Payments supports in-person payments. Give us a call to speak to us directly or fill out our contact form.

Frequently Asked Questions About In-person Payments

Although cash payments are becoming less common, accepting cash is still a good idea for most brick-and-mortar or mobile businesses. Some customers prefer or only pay in cash, and it can be convenient if there are any connection or outage issues. However, businesses should implement safeguards to mitigate the risks associated with handling cash. If your business is interested in implementing an ATM to facilitate cash transaction opinions, contact ECS Payments.

Accepting checks depends on the nature of your business. It may be inadvisable for businesses with high-volume and low-ticket transactions. However, checks may be suitable for B2B services. Keep in mind that accepting checks always runs the risk of bouncing, so use discretion if you decide to accept checks.

Absolutely. Credit and debit cards are the most popular payment methods among consumers. Customers also tend to spend more when using plastic than cash or check. While there are associated costs with implementing card payments, the increased business volume and convenience factor often outweigh the processing fees. Contact ECS Payments to learn which type of card solution is best for your business.

ACH payments are best for businesses that collect large recurring payments, such as landlords, schools, and utility companies. The lower processing fees make ACH an attractive alternative to card payments. Collecting ACH information in person may not be practical for high-volume sales. To implement cost-effective ACH processing in your business, contact ECS Payments to get started.