Is your healthcare facility struggling to keep patients? Are you looking for more ways to boost business? Do you need to find an alternative way to treat your patients and make a healthy profit quicker? Medical financing may be the answer you have been searching for. Follow along to discover how simple financing options can boost your business.

Why Should I Implement Medical Financing if My Facility Accepts Insurance?

In the United States, health insurance’s design is to provide financial relief to patients. It should cover checkups, emergency visits, or long-term medical treatments. Unfortunately, a majority of Americans suffer from crippling medical debt that is nearly impossible to pay off. Even with employer-supplied or privately purchased health insurance.

Furthermore, nearly 50% of Americans choose to decline or significantly delay medical treatment due to out-of-pocket costs. Treatment is important. Whether elective, preventative, recovery, palliative, or emergency, it all makes a difference in a patient’s quality of life.

Oftentimes it is absolutely necessary. Because of this, it is important to offer patients a way to financially cover all their treatment.

This is where offering medical financing will benefit your patients. Patient financing allows access to treatment that otherwise would have been out of reach. Plus, healthcare businesses that offer an in-house lending program do better than their competition.

Furthermore, in-house, point-of-sale (or in this case, point-of-care) financing fulfills your patients’ financial concerns immediately. No need for a patient to take the time to research lenders or look for the right financiers. Patients won’t walk out of the facility with no idea how they will pay for uncovered services.

When a healthcare provider can present financing options in-house, a patient has immediate trust. They already trust you for their health. So, rather than shopping for financing on their own, an option from a trusted source is the best solution.

What is Medical Financing?

Medical financing provides a way to receive treatments or procedures that insurance do not cover, such as elective surgeries or to cover the still expensive co-pay that a patient’s bank account can’t. Essentially, a patient would take out a medical loan or apply for a line of credit for upfront medical costs that they could not afford otherwise.

Medical Loan

A medical loan is another way of saying a personal loan for medical expenses. Most financiers do not have strict usage boundaries with their loans. Therefore, personal loans and medical loans are interchangeable.

The borrower receives a fixed amount of money and they designate how they utilize their approved financing. They would then repay the loan incrementally over a fixed amount of time and with fixed interest rates.

Medical Line of Credit

Comparatively, a line of credit offers a borrower a maximum limit. The borrower can use as little or as much as they like from their credit limit. They can then repay it incrementally, and continue to borrow up to their limit, as much or as little as they need.

How Can My Patients Benefit From Medical Financing?

It’s rare that insurance covers 100% of medical procedures. Even in cases when insurance does cover all or the majority of a procedure, the deductible alone can be financially taxing. Because of this, many patients struggle with providing the necessary funds for uncovered, out-of-pocket expenses upfront.

A patient can use their medical loan to pay for a variety of medical expenses that your practice may offer. Medical loans can also cover a patient’s day-to-day financial needs while they recover from their medical procedure.

Moreover, patients can benefit from medical loans by consolidating numerous medical bills into one easy payment. This can simplify your patients’ bills. It can even make their monthly payments less if they qualify for a lower APR.

What Procedures Can Medical Financing Cover?

When it comes to paying for treatment, medical procedure financing has virtually no limitations. Your healthcare facility may offer any of the following. Your patients can have peace of mind that they can receive their procedure with easy medical loan approval right from your office.

- Dental procedures

- Orthodontics

- Fertility/Infertility procedures

- Vision care

- Hearing care

- Cosmetic surgery

- Hearing care

- Hair restoration

- Weight loss surgeries

- Chemotherapy

- Dialysis

- Any other long-term treatments for chronic illnesses

- Physical therapy

- Drug and alcohol rehabilitation

- Long-term care

- Therapy and mental health services

- Urgent care/unexpected medical emergencies

- General Healthcare

- Intensive care

- Veterinary services

How Would My Patients Get Medical Financing?

Patients who need medical financial aid can apply for healthcare financing at an institution like a physical lender’s office, a bank, or even through an online lender. The benefit of online lenders is that many offer partnerships with healthcare facilities.

However, if you are wanting more patients to say “yes” to their procedure, integrating in-house medical financing through an online lender is the answer.

When you offer a lending program in-house, you can help your patients apply for financial assistance right in their chairs or at the front office.

Applying online for a medical loan or line of credit is a quick and easy process. This usually takes a few minutes to complete. Approval is available before the patient has time to leave your facility. Swiftly addressing patients’ number one concern, money, immediately gives them little reason to deny a procedure.

Is Medical Financing More Advantageous than Payment Plans?

Offering payment plans can be a great option for healthcare facilities to get their patients to commit to treatment. Payment plans split large medical expenses into multiple months of automatic payments. They require no collateral, no interest, and no lender involvement.

Unfortunately, payment plans have their downside. With this solution, you will get paid over a period of time, rather than immediately. Because of this, payment plans are risky to providers. Patients can leave with their treatment complete and default on their payments.

They may have changed their card, or put an almost expired card on file. Chasing down patients for unpaid invoices is not the best option when it comes to securing your due compensation.

Alternatively, you can incorporate medical financing with a designated lender. This would still provide your patients the option to split their medical expenses into monthly payments. However, this solution has zero financial risk on your part.

The lender would be assuming all risk with the medical loan. They would be responsible for sending the money, offering the credit, and collecting the repayment.

With finances secured, your payment is instantaneous from the financier. And the patient can have same-day treatment or schedule for the next availability. Without having to worry about how they will afford to cover the expense upfront.

Because of this, healthcare practices offering their own lending programs outsmart their competition and boost their profits tremendously.

What Qualifications Would My Patients Need for Medical Financing?

Luckily, most personal loans are unsecured. Unsecured loans do not require any collateral such as a home, vehicle, or savings account. This means the patient will not need to sacrifice important areas of their life in the name of their health.

However, approval on unsecured personal loans is typically reserved for borrowers with good credit scores. Better credit scores attract better rates. More attractive rates incentivize patients to move forward with their medical procedures.

If a borrower has poor personal credit, there is the option of secured personal loans. Secured loans require collateral for approval. However, they can benefit a borrower with more competitive rates than an unsecured loan.

Ultimately, every lender’s criteria are unique. Below are the general factors that play into the decision-making of a medical loan application acceptance:

- Credit score- The higher a credit score is, the better the loan terms are. Typically, higher credit scores give borrowers lower interest rates. Poor or no credit scores will yield higher interest rates. This in turn makes loans more expensive and thus more difficult to pay off.

- Income- Generally, the more a borrower makes, the higher the loan approval will be. If a borrower does not make enough to cover even the monthly expenses of the loan terms, they may not qualify for medical financing.

- Loan terms- Interest rates vary depending on the amount of money needed or the time frame required for repayment.

Comparing Medical Loans

Before your patient commits to a loan or a line of credit, they may want to do some comparison. There are many different lenders out there, and you want to be sure you can help provide the best options to your patient. Some details make a difference in the impact of a loan’s financial burden or assistance to your patients.

Annual Percentage Rate (APR)

Examining the annual percentage rate (APR) is important when deciding on the right loan or line of credit. APR is the additional cost of the loan on top of the loan amount. This includes the interest rate as well as any other extra fees the lender charges.

A lower APR is generally offered to applicants that have good or excellent credit scores and low debt-to-income ratios. These types of borrowers pose less risk to the lender. Because of this, the reward is lower loan costs.

Reversely, applicants with poor, little, or no credit history have higher APRs. Lenders charge higher fees to high-risk borrowers to compensate for the potentially hazardous approval.

Ultimately, the higher the APR is, the more expensive the loan is. And the less affordable it becomes to borrow money. Medical loan APRs can range from as little as 2.49% to upwards of 35.99%.

Amounts

Every borrower is unique. Therefore, approval terms and rates are different based on each borrower’s circumstances. A lender would need to be well-established to offer a large loan. However, the amount offered is typically based on an applicant’s income and credit score.

Approval amounts are higher for borrowers with larger incomes and better credit scores. Conversely, approval rates are lower for applicants with poor credit and little income. The lender wants to avoid as much risk as possible. A lender assumes additional responsibility when giving money to a borrower who might not have the best track record or financial means to repay the money.

Loan amounts can range from as little as $1,000 to as much as $100,000 or more. Your patients would need to determine how much they want to apply for based on their procedure cost, follow-ups, and day-to-day financial needs during recovery.

Medical Financing Fees

Lenders all have differences when it comes to their fees. Some lenders do not charge additional fees other than the interest rate. Some lenders may charge origination fees, late fees, prepayment penalty fees, returned check fees, or more.

Funding Speed

The benefit of a line of credit is that it can be applied instantaneously. Loans, on the other hand, rely on physical funding to a borrower’s bank account. The sooner funding can hit your patient’s account, the sooner you can start treatment. Some lenders fund borrowers’ bank accounts 24 hours later. And other lenders may take up to a week to fund the borrower.

Loan Terms

Loan terms are the amount of time the borrower has to repay the loan plus all interest and fees. The length of time tied to a loan will affect a borrower’s monthly payment. It will also affect the overall cost of the loan.

Loan terms can be short-term ranging from a few months up to 12 months. Or long-term can be 13 months, 60 months, or even 300 months, which is 25 years.

The shorter the loan terms are, the higher the monthly payment will be. The longer the loan terms are the shorter the monthly payment will be. Because a condensed timeframe squeezes higher payments into fewer months. And a longer time span spreads the payments into smaller monthly increments.

However, the longer a loan takes to pay off, the more interest will accrue. This makes the loan’s total cost more expensive. Conversely, the quicker a borrower can pay off their loan, the less interest they will have to pay.

Let’s take a further look into the different types of loan terms, the benefits, and the disadvantages of each.

Loan Terms for Medical Financing

There are a variety of terms offered to pay off medical loans and lines of credit. A common question you may receive from your patients as they apply for funding is “Which option is better, short-term or long-term?”

Despite being in the medical field and not in financial services, it is best to understand the basics. Especially when offering in-house financing to your patients. Knowing how to best help your patients in every aspect will make you more trustworthy to your clients. Producing more treatment conversions.

Loans can range from a few months to 25 years. So why would a borrower choose one option over the other? Let’s take a look further to better understand your patients loan term choices.

Short-Term Loans for Medical Bills

Generally speaking, short-term loans need to be repaid after a few months, up to a year. So when choosing between 6 months to a few years, why would someone go with the short-term option?

Short-term loans are best suited for borrowers who need a small amount of money quickly. These may be patients who can almost afford a procedure, but not in full. They can take out a short-term loan to cover the remaining portion of a treatment that they want to or need to start immediately.

Advantages of Short-Term Loans

- Quick access to funding for services otherwise unaffordable

- Become debt free faster

- Less expensive in a total

- Most do not have a prepayment penalty

Disadvantages of Short-Term Loans

- Higher monthly payments

- Higher interest rates

- Limited borrowing amount

- Quick approaching repayment deadline

Long-Term Loans For Medical Financing

Conversely, long-term loans are repaid over a few years. This can go all the way up to 25 years. However, it is more common to see long-term loans in the 5-7 year range. The length of time would vary from patient to patient based on their credit scores and financial needs.

Advantages of Long-Term Loans

- Quick access to funding for services otherwise unaffordable

- Become debt free faster

- Less expensive in a total

- Most do not have a prepayment penalty

Disadvantages of Long-Term Loans

- Disadvantages of Long-Term Loans:

- Higher monthly payments

- Higher interest rates

- Limited borrowing amount

- Quick approaching repayment deadline

Ultimately, a borrower would need to choose the loan that offers the funding they need for treatment. Additionally, they would need to decide if the monthly payment or the final total cost is most important to their budget.

Benefits of Adopting Medical Financing to Your Medical Practice

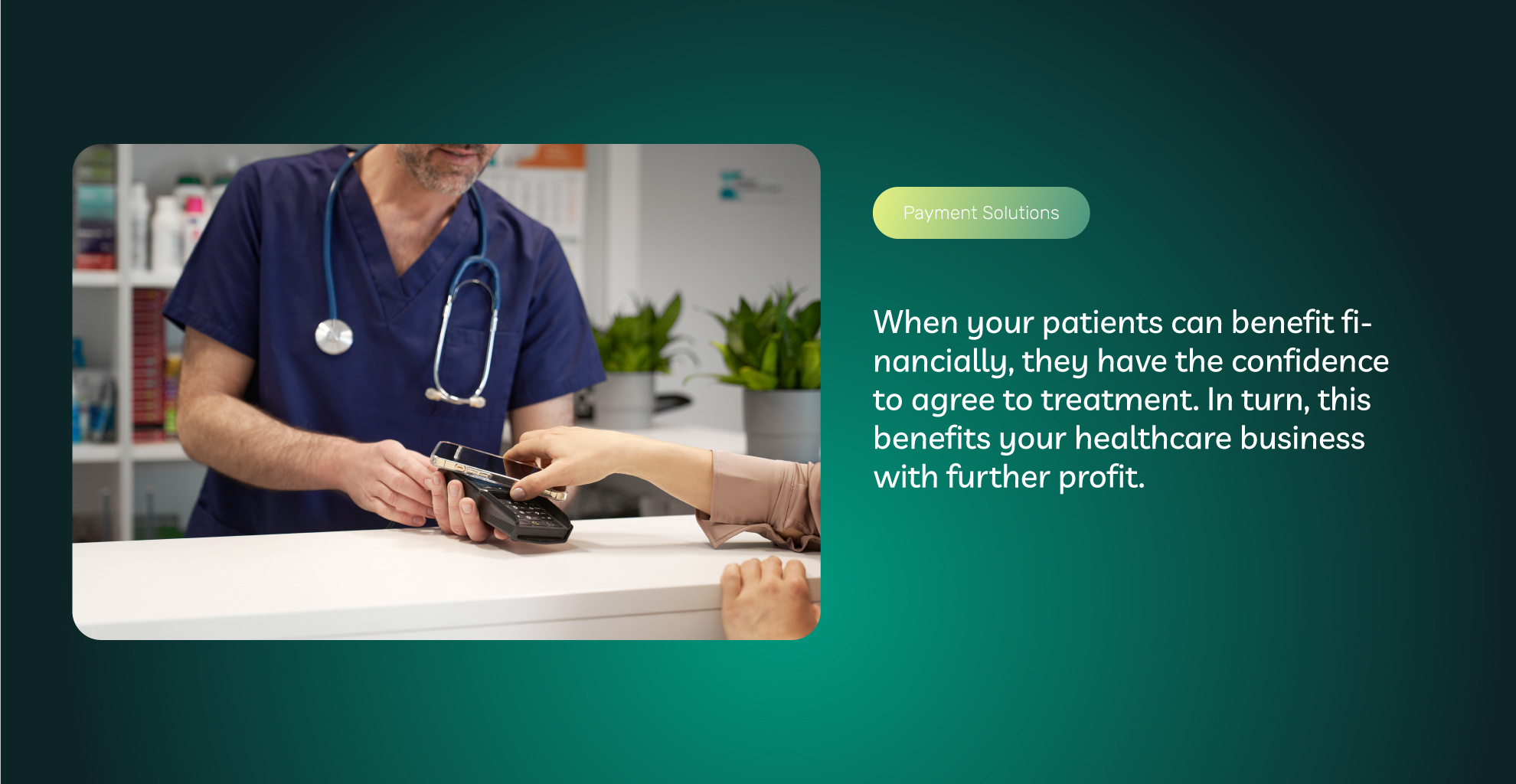

Adopting medical financing for your patients has many advantages. For both your patients and your practice. When your patients can benefit financially, they have the confidence to agree to treatment. In turn, this benefits your healthcare business with further profit. Below is a list of all the advantages offering medical finances has.

Loan Consolidation

If your patients are paying off multiple procedures, medical loans can consolidate all debt into one simple payment.

Acceptance of Medical Treatment

Procedures whether cosmetic, emergency, or ongoing are all important. But finances can stand in the way of getting patients the help they need. Medical financing offers a solution for patients to feel confident saying “yes” to treatment.

Higher Profit Margins

As a healthcare provider, your goal is to help your patients receive the treatment they need. Finances play a huge factor in patients’ willingness to accept their treatment plan. In-house medical financing provides your patients with a way to work around their budgets. It also provides you with instant payment from the financier. More yeses mean more profit for your healthcare business.

Flexible Loan Terms

Every patient is unique. Different procedures, available funds, and budgets require different financial assistance. Everyone benefits from medical loans and lines of credit with fixed-rate financing and flexible repayment terms and APRs.

Quick Funding

Many medical procedures cannot wait. However, many healthcare providers are unable to perform a treatment if a patient has no financial means to cover their services. Medical financing offers almost immediate funds to get a provider the money they need to perform the treatment. Therefore, patient care is not delayed. Funding can be as soon as the same business day, the next, or a week later.

Affordable Alternative to Credit Cards

Medical loans or lines of credit generally have lower interest rates compared to credit cards. If a patient were to pay for their medical bills with their credit card, they may be paying interest of 16%-35%. And they could max out their credit card limit.

This would put them in a financial hurdle for any other day-to-day needs. Many medical loans offer some lower-end interest rates between 2-8%. It would also be separate from the patient’s credit card limit. This would give them more available funds in every aspect of their budget.

Flexible Payment Allocation

Borrowers can use their own discretion on their medical loans. They pay for their medical procedure. They can also cover the cost of living during their recovery time. To be honest, they can use it for literally anything else they choose to spend the money on.

Application Convenience

Implementing in-house medical financing provides your patients with a quick, simple, and convenient application process. They can apply on your website from the comfort of their home, in their treatment room, in the lobby, or at the front desk of your establishment.

Online applications take minutes to complete. And seconds to receive approval.

Pre-qualification Screening

Many online lenders will offer pre-qualification screenings for your patients. Pre-screenings do not impact their credit scores. This process simply uses the patient information already loaded into your client database.

A social security number is not required. This provides a practical preview into what your patient may qualify for when they officially apply.

Practice Management Bridge Software Can Help Streamline Your Healthcare Payments

ECS has a partnership with Practice Management Bridge that can help to conquer the challenges healthcare providers face and streamline all your practices (at your practice), offer in-house financing, receive more “Yeses” to treatment, and collect more payments.

ECS and Practice Management Bridge partnership offer state-of-the-art payment solutions that encompass features like online or mobile payments, QR codes on bills or in-office, integrated payment plans and point-of-care financing, and digital patient forms, and enhanced payment security features.

As we’ve discussed, offering medical financing is important. Regardless if your practice accepts insurance or not. Why? Well, because 60% of the workforce is stuck with high-deductible insurance plans which have resulted in $433 billion of out-of-pocket costs for patients for necessary, emergency, and yes, cosmetic procedures.

Consequently, patients face severe financial problems and contribute to the excessive debt in healthcare, ultimately affecting you and your practice.

It is no surprise that patients struggle with medical debts. And with paper billing systems still in place amongst many healthcare facilities, it is obvious that both patients and practices need resources to help lessen healthcare related expenses on both sides of the fence.

Benefits of ECS’s Practice Management Bridge Software Partnership

This is where Practice Management Bridge and ECS become essential tools. Opening up a healthcare merchant account with ECS has advantages. We provide our solution through digitalized and simplified payment and financing methods all aimed at improving the patient experience while reducing administrative burdens.

We facilitate custom patient financing options and payment plans that cater to the diverse financial situations each patient faces. As a result, you will see an improvement in the probability of practicing successful collections.

In addition, to maintain compliance with the requirements of the payment industry, ECS employs robust security measures to ensure sensitive data protection when transferring and storing patient card information.

There are many advantages to using this platform, among them are:

- 20% less time spent on billing management

- 25% better payment reconciliation

- 90% reduction in manual refund processing

- 5% increase in payment collections

These results prove who ECS and Practice management bridge improves the probability of successful collections for practices.

ECS and Practice Management Bridge essentially offer an integrated approach to lessen the burden of medical professionals’ significant issues.

Medical Financing Make You a One-Stop Shop for Patients

As a healthcare facility, it can be a matter of life or death when it comes to patients accepting treatment or not. Many chronically or terminally ill patients may refuse palliative treatment. They want to avoid causing a financial burden on their loved ones when they pass on.

Alternatively, some patients may suffer from self-esteem issues with their teeth, weight, or hair. Others may have deteriorating joints or painful injuries. These may not be not emergencies. But, the treatments these patients desperately seek may seem out of reach due to financial availability.

When your healthcare facility adopts medical financing, you instantly become the hero in the story. You’ve become a one-stop shop for all medical and financial needs. There is no need for a patient to leave your office to look for ways to pay elsewhere.

You receive treatment acceptance on the spot. All while giving cancer patients more time with their families. Creating radiant smiles. Or providing rehabilitation treatment to patients who struggle to walk or get a good night’s sleep.

Your patients can have success stories. And your business will flourish from helping the lives of others. Imagine the potential your medical practice will have when it begins to offer more financial avenues to pay for medical expenses. Schedule and complete all the treatment plans you’ve designed with no hassle. “Yes” becomes easy and “no” becomes a thing of the past.

To contact sales, click HERE. And to learn more about ECS Medical Financing visit Healthcare.

Updated February 2025