Loan servicing software allows a business to easily extend credit to borrowers by providing a comprehensive platform for managing every aspect of the loan lifecycle. Loan management software can help screen potential borrowers, service loans, and integrate with other systems.

The more dynamic and comprehensive the platform, the more it will assist the lender. While this is true in all areas of lending, it is particularly true in riskier or less traditional lending paradigms like microlending, payday loans, and point-of-sale loans.

What Is Microlending?

Microlending involves issuing small loans to individuals or organizations that do not have access to a traditional, institutional loan. They may have poor credit. They may not have access to conventional banking institutions. Or, they might just want a loan too small for a conventional institution to be interested in lending.

As many as 200 million businesses worldwide may lack access to funding. Generally speaking, microloans that these businesses seek can range from a hundred dollars to up to $50,000. While there are businesses in the domestic market leveraging microlending, a substantial portion of this global $124 billion industry is in developing nations.

Women comprise 80% of the borrowers, and 65% of the businesses are rural. Regions that dominate the industry are Latin America and the Caribbean ($48 billion), Southeast Asia ($37 billion), and Africa ($10 billion). The predominance of microlending in “emerging markets” reflects the origin of microlending.

The Interesting Origin of Microlending

Microlending is a relatively recent invention, going back to the 1970s. Grameen Bank—whose slogan is “bank for the poor”—would extend loans to impoverished artisans in Bangladesh, India, Cambodia, and other developing countries.

These loans were extended mainly to women artisans, such as basketweavers. Such lenders would not need the large amounts of capital normally extended in a business loan. They would only need small loans. Moreover, such impoverished individuals had no credit or means of reaching a conventional bank.

Economist Mohammed Yunus came up with the idea of extending loan opportunities to these impoverished artisans, who were primarily women. He reasoned that these women borrowers were invested in providing for their households and would honor their loan agreements.

He also came up with the idea of “solidarity group lending,” whereby microloans could be divided against several recipients to reduce transaction costs for each borrower. As the borrowers already formed a cohesive social group, they would step in for each other should anyone default, guaranteeing (nearly) repayment of the total loan amount.

Mohammed Yunus’ idea was a socio-economic experiment to help marginalized communities. His lending ideas were not just driven by profit but by the ethical imperative that even “poor” individuals can help themselves out of poverty. Ultimately, Yunus was awarded a Nobel Peace Prize in 2006 for inventing microlending.

Microlending and the P2P Economy

So, what’s this got to do with the price of rice in China (or the cost of handwoven baskets in Bangladesh)? The origins of microlending continue to be relevant today. Microlending is still a means for individuals and small businesses to access the necessary capital.

Recall, however, that the origins of microlending were, in part, a community imperative. Yunnus extended a group loan to impoverished women whose social relationships helped guarantee repayment. What kind of social “glue” exists like that between the 33.2 million small businesses that exist throughout the United States?

None, really. But that’s okay. A new phenomenon, peer-to-peer lending, can facilitate microlending in tech-saturated markets like the United States. P2P lending allows individuals and financial institutions to extend available capital through a marketplace application, where eager borrowers can locate the microloans they seek.

The global P2P lending market is valued at $143 billion and $18 billion in the United States alone. Platforms like SoFi, Upstart, Lending Club, and Funding Circle are some of the most prominent names. Borrowers take microloans for business and personal reasons like funding life milestones or consolidating debt.

Lenders do not necessarily have to be financial institutions. In fact, most lenders in the P2P space are individuals who have some extra money lying around. Consumers are receptive to peer lending, and the industry as a whole is expected to grow at a CAGR of a whopping 26.5% through 2030.

Are There Risks to Microlending?

There most certainly are risks to microlending. Recall that microlending involves extending loans to borrowers who have bad credit, are essentially “unbanked,” or need smaller loans (meaning they don’t have much to begin with). Each one of these possibilities carries its own set of risks.

First, there are the borrowers with bad credit. Lousy credit indicates that a borrower has had trouble meeting their loan obligations in the past for whatever reason. But bad credit is often (also) an indicator of future behavior. For instance, 16% of individuals filing for bankruptcy have filed for bankruptcy before.

Then, there are the individuals who are unbanked for other reasons. In the United States, it’s unlikely that a consumer would not have access to a brick-and-mortar banking branch to discuss loan options with a banker. By contrast, this is a reality in developing nations where microlending was invented.

Unbanked individuals may have bad credit. They may have inherited poor financial literacy. They may have a bad taste (about banking) in their mouth from the 2008 subprime lending crisis. Or there may be a nuanced mix of reasons why they cannot turn to a traditional financial institution for a loan.

Are Smaller Loans Riskier Business?

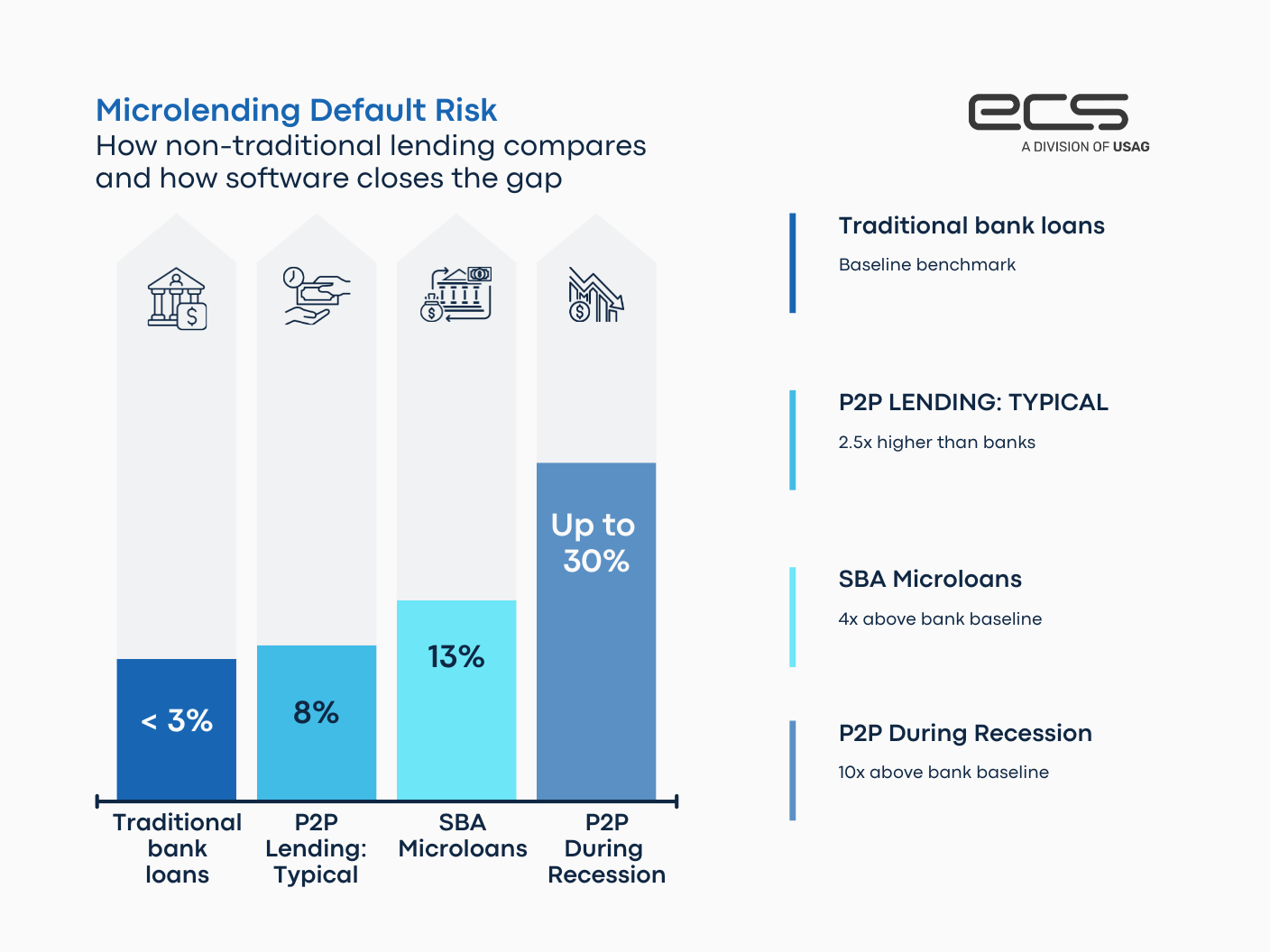

And then, some individuals just need a smaller loan. This in itself can present a risk. The average size of a microloan is $13,000 in the United States (it’s $144 in India). A borrower taking a smaller loan may have a greater likelihood of defaulting.

As an example, the default rate on Prosper, the largest domestic P2P platform, is generally above 8%. And in troubled economic times, that number can soar up to 30%. To put that number into perspective, the default late for consumer-facing loans from traditional financial institutions is generally less than 3%.

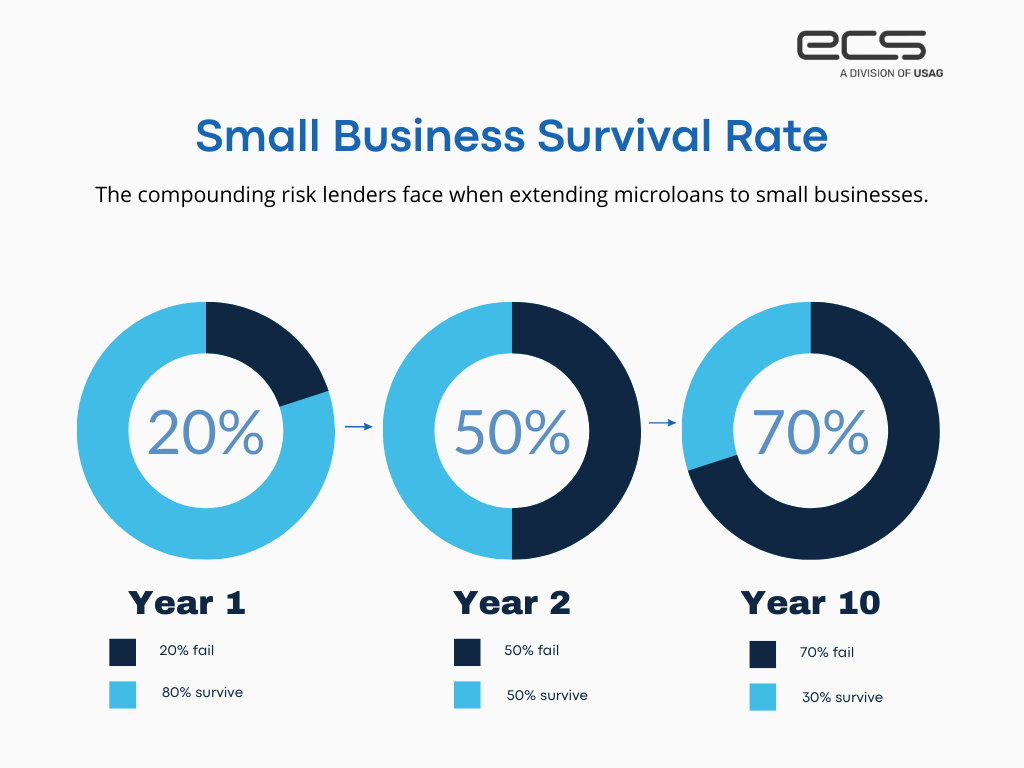

A business loan under $50,000 (the upper limit of what the SBA considers microlending) is probably a small business. No corporation or midsize business would take a loan this small because it would not accomplish anything. Small businesses have a substantial rate of failure: 20% within the first year, 50% by the 5th year, and 70% within a decade.

Then, there are microloans taken by individuals. For example, an individual might take a microloan to consolidate their credit card debt, their medical debt, and what’s left of their car loan. What happens to that borrower when inflation hits record levels and the U.S. enters a recession?

The individual lenders who comprise the P2P lending space cannot fall back on vast cash reserves or land in golden parachutes provided by government bailouts. P2P lenders are taking a substantial risk. And even institutional lenders who engage in microlending are potentially playing with fire (not literally).

How To Mitigate Microlending

There are ways to mitigate the risks of microlending. One of them is to essentially sell repackaged loans from a government entity like the SBA. The Small Business Administration does not extend loans themselves. Instead, they farm these loans out to consumer-facing banks.

The SBA insures the loan and promises to repay the lender if the borrower defaults. This can mitigate a substantial portion of the risk of extending small business loans (considering that only 30% survive ten years). However, this option is primarily only available to institutional lenders.

So, what are smaller organizations able to do in terms of mitigating risk? Can platforms and marketplaces like SoFi and LendingClub facilitate risk management? The answer is a frustrating yes and no. Many of these platforms do not allow lenders to choose their borrowers. The platform itself manages the application process and the loan management.

For lenders who just want to put their unused money to work, that might not be a problem. Getting involved with lending systems and debt collection is not on their bucket list; they may have their own businesses or assets to manage.

But for organizations for whom lending is a business, platforms like Sofi will not do. They need something a little more hands-on. They need to take their own loan applications, manage their own application process, and they need to do their own credit risk assessment. And that means some sort of loan or microloan management software.

What is Loan Management Software?

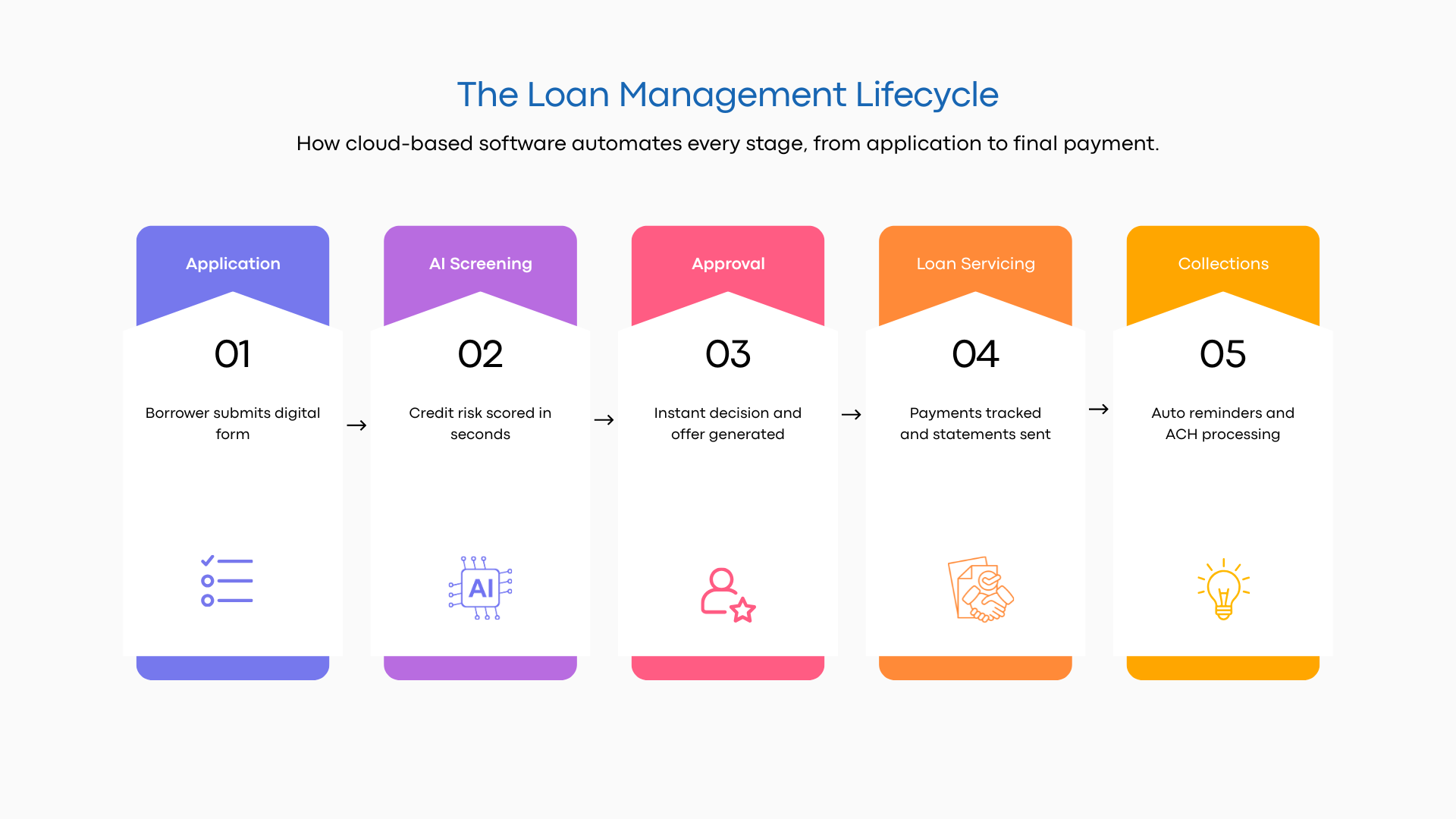

A loan management system is a platform that allows a borrower to manage all phases of the lending process. This can include everything from the initial application to sending out monthly reminders about upcoming payment due dates.

An overarching idea behind loan servicing systems is process automation. Parts of the lending process that used to be paper-based and prone to human error have migrated to digital platforms that use AI and real-time data power.

Loan management software can also provide a better customer experience. Banks and credit unions increasingly use cloud-based software to provide customers with transparent financial services. Borrowers can use mobile apps to check on the progress of their loan, see their interest rates, explore related financial products, and consider the possibility of refinancing.

Loan management software can also provide beneficial party integrations with other software suites. For example, lenders find that integration with accounting, compliance, and even HR software can reduce the cost of workflows. Taking HR as an example, organizations with sales teams can integrate credit applications with payroll incentives.

This type of integrated complexity is taken for granted at large banks. But it has been traditionally unavailable to smaller lenders and business owners…until now. The advent of remotely accessible, cloud-based SaaS allows organizations to access robust and comprehensive systems that can streamline their lending process.

What Is PayDay Lending?

Payday lending involves extending consumers credit in return for repayment from an upcoming paycheck. Payday loans are similar to microlending in that they are usually $500 or less. They are used (pretty much) exclusively by consumers to bridge gaps in financial solvency.

Today’s consumers live paycheck to paycheck (literally, not proverbially). The average consumer cannot afford a $400 surprise expense. This may be why 12 million Americans tap into payday loans each year. The typical earnings for an individual using payday loans is approximately $30,000, and 58% have trouble covering their monthly expenses.

A plethora of fintech apps that essentially provide payday loan services have emerged. Dave, Beem, and Brigit are a few of the recognizable names. These applications extend $50, $100, or a few hundred dollars to borrowers based on an analysis of the borrower’s banking statements (and other factors).

As you can surmise, it would be impossible for these organizations to extend payday loans to such a broad consumer base without the power of software integrations and analytics. Analytics allow these companies to observe patterns in the checking accounts of their potential customers and see if a payday loan can be extended (e.g., that a periodic paycheck is indeed deposited).

Brick-And-Mortar Payday Lenders

There are also brick-and-mortar payday lenders. Traditionally, these payday lenders have not had advanced software tools to manage their loan portfolios. They’ve had to hedge their risks by charging higher interest rates for payday loans or taking collateral.

One problem that traditional payday lenders have faced is collecting their money back. They may have attempted to mitigate this risk by taking collateral. However, the process of selling the pawned collateral takes up time and energy.

Loan Management Software can eliminate this problem in several ways. For starters, the lender can collect customer financial information at the point of sale, like ACH info, debit cards, or credit cards. This information can be saved in the system and then used to process recurring charges until the loan is paid off.

Saving payment information, however, carries additional regulatory concerns. For example, Visa and Mastercard demand that all businesses retaining card information adhere to their PCI DSS standards. For most small to midsize businesses, adherence to these standards is cost-prohibitive.

Once again, cloud-based applications save the day. The software platform can be responsible for saving this payment information and meeting PCI DSS standards. It can also be responsible for meeting any other regulatory or compliance standards imposed at state and federal levels.

Another way loan management software can help is through automated payment reminders. Customers who have payments coming up can be texted and emailed. If, for whatever reason, payment information was not captured during the application, these reminders can help recapture a significant portion of unpaid debts…on time. And they can be automated with a software system with customer data (like contact information).

Point of Sale Loans

Another area of microlending is the point of sale in retail settings. And by retail settings, we mean to include B2C (even B2B) vendors of goods and services. Some customers cannot pay for an entire purchase in one payment. These customers need financing.

In-store financing is an attractive solution for these customers because it typically does not draw from or impact their credit as much as other loan types. Usually, point-of-sale financing is straightforward for consumers to obtain unless they are on a terrorist watch list or have a fraud alert.

For the merchant, the problem is how to connect their customer with this financing. Large corporations like Macy’s and Costco offer their own credit cards (although they are serviced and managed by third parties). Smaller businesses do not have their own credit card to provide customers with.

They can refer customers to the payment terminal to complete a point-of-sale loan. Usually, this involves asking a few basic questions. The purchase can then be completed and the merchant or service provider can be paid within 24-48 hours. The loan is managed by their payment processor or its banking partner.

In these cases, the merchant does not have to do any loan servicing. But for merchants who do want to offer their own loans, loan management software that integrates with their other systems is indispensable. Indeed, loan servicing software is indispensable for companies that provide point-of-sale loans.

AI, Machine Learning, and Mitigating Risk

Point-of-sale loans, Payday loans, and microlending typically have low lending requirements. After all, many customers taking advantage of these loans have bad credit, no credit, or just need a small amount of money.

However, analyzing data with AI and machine learning is still essential for mitigating risk. Take payday lenders, for instance. As mentioned, fintech applications like Dave use AI to analyze customer bank accounts to determine how much they can lend to a customer.

These advanced tools are no longer out of the reach of smaller lenders. Cloud-based lending SaaS can allow lenders access to the same powerful tools at affordable, small-business-sized prices. For lenders with a vetting process, AI tools are also indispensable for mitigating risk by keeping potential bad borrowers away. These tools can make credit decisions within minutes or seconds instead of hours or days of human investment.

Dynamic Loan Management Software Wrap-Up

Loan Management Software can help lenders provide and service all types of loan products, including payday loans, point-of-sale loans, and microlending. These types of loans come with specific amounts of risk, but that risk can be alleviated with the powerful AI tools inherent in the SaaS. Cloud-based suites can also offer integration possibilities to streamline other aspects of the loan management process. To learn more, contact us or fill out the form below.

Frequently Asked Questions About Loan Management Software

How can Loan Management Software assist in managing microlending and point-of-sale loans?

Loan Management Software’s comprehensive platform streamlines merchant processes from the application to the payment reminders. It also uses AI integrations to enable informed decisions for lenders.

What is the significance of microlending and lending software in emerging markets?

Microlending can reach individuals and businesses that may lack access to traditional loan options. Loan Management Software’s dynamic platforms allow lenders to efficiently manage their microloans.

Can Loan Management Software help reduce risks associated with microlending?

Yes, Loan Management Software’s AI, machine learning, and automation tools offer features such as borrower data analysis and recurring payment reminders so lenders can make faster credit decisions, manage potential risks associated with bad credit or smaller loan amounts, and receive higher percentages of their funds back on time in these diverse markets.

Is cloud-based Loan Management Software beneficial for every type of business?

Cloud-based Loan Management Software ensures both accessibility, affordability, and compliance with PCI DSS and other industry standards for lenders of any size. This includes small businesses.