Loan Management Software provides lenders and even retailers a platform to extend and service customers’ loans. This type of software replaces many previously paper-driven, human-performed aspects of the loan lifecycle. And in doing so, Loan Management Software offers many benefits and features. Let’s take a look.

Loan Servicing Software is Scalable

The lending industry’s digital transformation has created many fintech solutions. These tech players like SoFi and Upstart allow businesses to access much broader markets of potential customers.

Some of these solutions are P2P platforms where potential lenders are paired with borrowers. These platforms are facilitating lending at an unprecedented scale, allowing organizations and even individuals sitting on cash to loan it out.

In many ways, the explosion of lending-focused fintech platforms has mirrored the broader market of P2P applications like Uber, Instacart, and Upwork. These marketplaces connect available talent or resources with customers needing a ride, freelance work, or someone to do their shopping.

The reach of these application-based businesses is as broad as their marketing efforts. For instance, SoFi has funded $73 billion in loans to date. Upstart originated nearly $12 billion in loans in 2022.

To put those numbers in perspective, Wells Fargo originated $159 billion in loans in 2021. As for Upstart, originating 7.5% of the total loan amounts of one of the biggest banks in the world is not bad for a company that is barely over a decade old.

The acceleration of these tech upstarts to capture so much market share so quickly shows you just how scalable they are. The limited radius of influence endemic to brick-and-mortar financial institutions does not encumber them.

As a lender, lending management software may provide you with the same type of reach. If your lending management system integrates with a customer-facing platform, you can originate loans for customers wherever they are; whether that’s New York, Kalamazoo, or Malibu.

Loan Servicing Software Offers Better Customer Experience

This leads us to our next point: loan products offered through a digital platform facilitate better customer satisfaction.

Accessibility

Accessibility is important to customers in the financial space. For 41% of consumers searching for a primary bank, ATM and branch availability were primary factors, and 16% cited online or mobile tools. This beat out fees (25%) and even interest rates (8%).

Similarly, 31% of customers cited online or mobile tools as the primary reason they are satisfied with their current bank, followed by customer service (29%) and ATM and branch availability (27%). Only 2% cited rates as a primary reason for satisfaction.

These findings are significant. 16% of customers were looking for accessible online and mobile banking as they searched for a bank or lender. However, once they were enrolled with an institution, this number nearly doubled in importance. Meanwhile, the percentage of customers most focused on rates dropped by 75%.

These findings suggest that online and mobile accessibility are crucial for keeping customers and borrowers, eclipsing concerns like their interest rate or how it might compare to competitors.

Money talks, as they say, so marketing better rates can go a long way. However, it can be difficult for the average consumer to understand what percentages mean regarding monthly payments. Moreover, what a percentage means to one customer might mean something totally different to another based on outstanding balances and lifespans.

Customer-facing Dashboards

This is why some banks and lenders are pivoting to marketing customer-facing dashboards. These platforms can do a number of things, like categorizing spending and creating pie charts. They can show FICO scores. And they can help set budgets.

In fact, 31% of polled consumers would leave their bank if they were unsatisfied with its digital services. Banks with excellent customer-facing applications are capitalizing on these sentiments and gaining new business.

This wide range of functionalities may not apply to your lending business (although FICO scores may). However, the upshot of these banking dashboards is certainly relevant: customers want access to their financial products. A loan management solution with a robust customer dashboard can help draw in new borrowers and keep current ones from exploring refinancing.

Loan Servicing System Automates Tasks

Another benefit of loan management systems is that they automate manual tasks in the lending process. This is true not only for the (heretofore) manually intensive origination process but the life of the loan as well.

For instance, a loan management system can automate reminders to borrowers about upcoming monthly payments. Customers like being in the loop digitally with email and especially text reminders. Automating these reminders can also help lenders ensure they will be paid on time.

Reducing Manual Hours

The automation of these tasks saves money in several ways. Firstly, automation significantly reduces the hours required to service the loan. The average midsize business spends at least 14 hours every week chasing down late payments, translating to 18 full weeks of an employee’s yearly salary.

Increasing Payments

Automation of payment reminders also increases the likelihood of customers making payments. One study found that businesses following up with 70% or less of their owed payments were more likely to receive payments 31to 45 days after their due date, but those that follow up on 90% of invoices were more likely to get paid within a week of the due date.

A partnership of text and email reminders improved the likelihood of getting paid on time by 56%. These findings show that customers should be engaged in an omnichannel approach. However, this is next to impossible without an automated platform to keep track of the loan and send these reminders through different channels.

Reducing Human Error

The automation of loan servicing can also significantly reduce human error. One place in the loan management process where this truism is readily apparent is origination. Collecting customer data and then translating that back and forth with underwriting teams can become an opportunity to lose or erroneously change information.

With automation, there is no data entry. Data input by the customer (name, contact info, email, income, and employment information) can be carried right to the underwriters or credit analysts in their original forms.

IBM has concluded that bad data (e.g., human error) may cost domestic businesses as much as $3.1 trillion per year, including the financial sector. With the average employee making 118 mistakes per year, automating origination and underwriting processes can eliminate the financial impact of these mistakes—by circumnavigating them altogether.

Loan Servicing Software Can Leverage AI

Speaking of the underwriting process, another increasingly common loan management software feature is using Artificial Intelligence. AI, as it’s called for short, is essentially the ability of a machine or software to analyze data sets and draw conclusions.

Making Credit Decisions

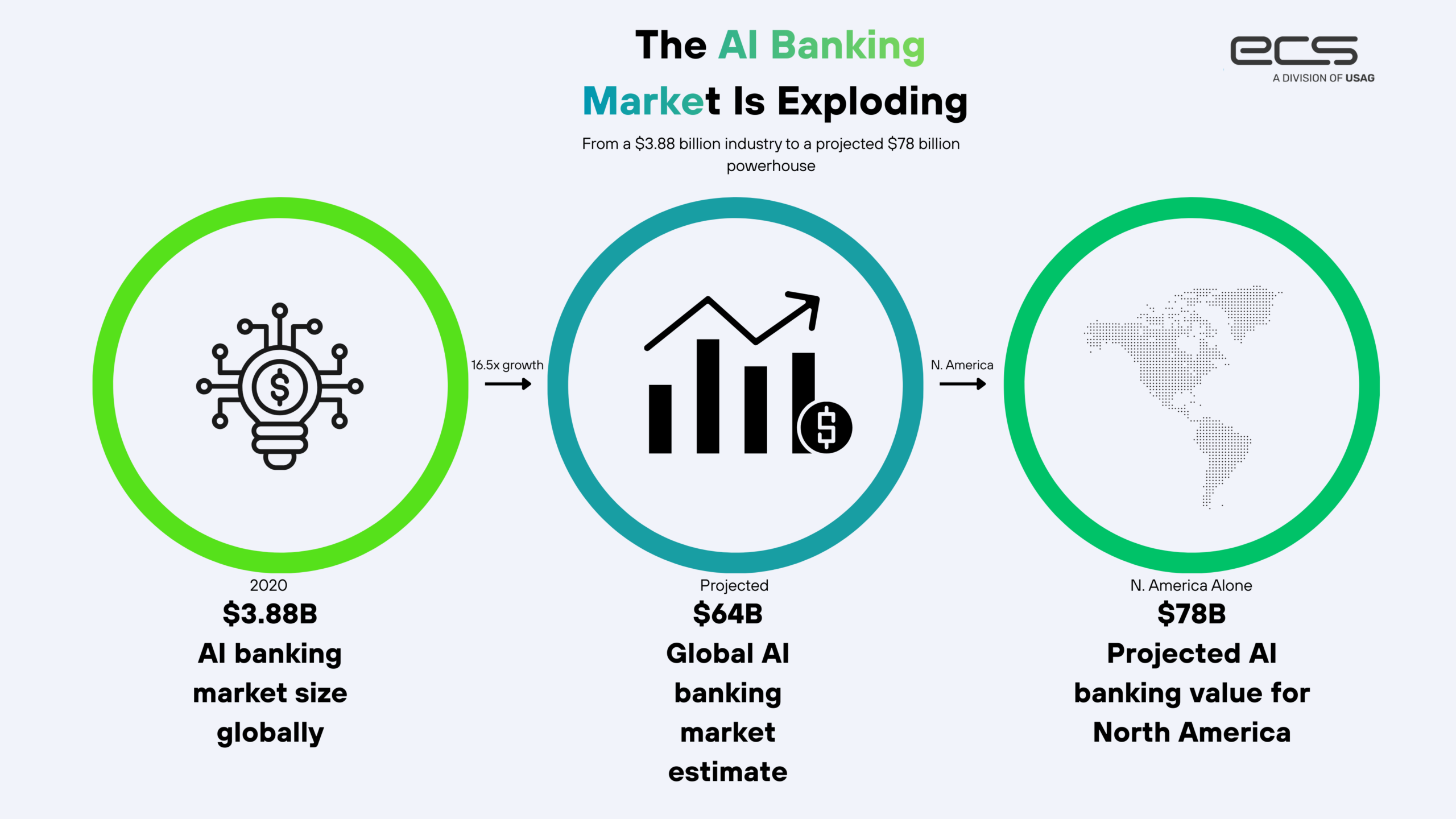

AI is perfect for things like making credit decisions. The use of AI for loan decisions fits into the broader picture of AI in banking. The AI banking market was $3.88 billion in 2020 and is estimated to soar to over $64 billion. In fact, some surveys have concluded much higher numbers: that AI banking will have a market valuation of $78 billion in North America alone.

AI can perform credit risk analysis on potential borrowers, sometimes within seconds. That’s because AI can rapidly assess real-time data and construct statistical models rapidly. Credit decisions that would formerly take hours, days, or weeks can now be made in seconds.

For instance, a new tech startup in the UK, MQube, has software that uses AI to make a mortgage decision in 15 seconds. For consumers applying for credit cards, the standard expectation is that the decision after the application will take 60 seconds or less.

But What About the Credit Analyst Jobs?

One might wonder what will happen to all the credit analysts with the advent of AI. It’s a larger question that can be applied to many industries, not just banking. However, historical trends tell us that new technology may not spell out the doom of certain banking professions. In fact, it might create more demand.

For instance, the advent of automated tellers was predicted to permanently eliminate the need for live tellers. What has ended up happening is something of the reverse: banks have continued to open branches. Live tellers and bankers provide additional services that ATMs cannot replicate.

So, let’s look at the use of AI as a loan management software benefit, particularly for startups and midsize lenders. In conjunction with our earlier comments about scalability, we see that AI allows lenders to do more. More loans can be originated, processed, and serviced than ever before, with the same amount of human capital or even less. Some estimates suggest AI can take over 90% of the workload of vetting, extending limits, and enforcing controls.

And these small to midsize lending operations can also avoid more financial losses with AI. That’s because AI can provide improved credit risk assessment. One study found that machine learning facilitated by AI can reduce losses from delinquent customers by 25% or more.

Loan Servicing Software Provides Analytics

The other side of the coin (that is, opposite credit analysis) is using AI and big data to service existing lenders. Lending and mortgage management software can provide you with data points to make decisions about individual customers and your business as a whole.

Many banks use these types of analytics to make decisions about upselling additional products to the customer. For instance, a bank that observes a high frequency of purchases from hardware stores and/or contracting services may be poised to offer that customer a HELOC or a mortgage refinance.

If your lending business is only focused on one type of loan or financial product, these types of cross-selling-focused analytics may not make sense. However, data points gleaned from customer behaviors can still help you make big-level decisions.

For instance, let’s revisit the conversation about customer experience and automated reminders. Analytic software could give you nuanced breakdowns about the most effective ways to notify each type of customer about upcoming payments.

For instance, you may find that borrowers aged 18-32 have the highest response rate to text reminders, and borrowers aged 32-44 respond better to emails. You might learn that text messages are more effective when sent three days out but less effective when sent four days or more before a payment due date.

This type of information can inform your business strategies about the most effective ways to engage current borrowers. It can tell you how to market to prospective customers more effectively. And in the process of doing all that, it can save you money, reduce defaults, and increase your profit margins. According to some studies, data analytics can increase profit margins by 81%.

Examining the Loan Portfolio

Another aspect of big-picture management is examining the overall loan portfolio. The impartiality of machine-driven analytics can help assess which parts of the portfolio are lucrative and which ones can be let go.

Larger banks have entire departments committed to keeping their most profitable customers engaged. For example, suppose they learn that a credit card customer has transferred a large balance to another institution. In that case, they will keep track of that and call the customer when the new promotion winds down to see if they want to transfer their balance to a new promotion.

You may think smaller lenders cannot leverage this nuanced analysis, but they can. It’s all made possible with the automation provided by the software and its ability to rapidly analyze large data sets—like a loan portfolio.

Loan Servicing Software Integrates With Retailer Goals

Not all businesses using loan software are lenders or financial institutions. Some of them are retailers or service providers. These merchants are offering third-party integration point-of-sale loans to customers making large purchases.

BNPL

For example, in the retail space, there has been a proliferation of BNPL transactions (buy now, pay later). Companies like Klarna, Affirm, and Afterpay allow customers to break a purchase into smaller, interest-free payments.

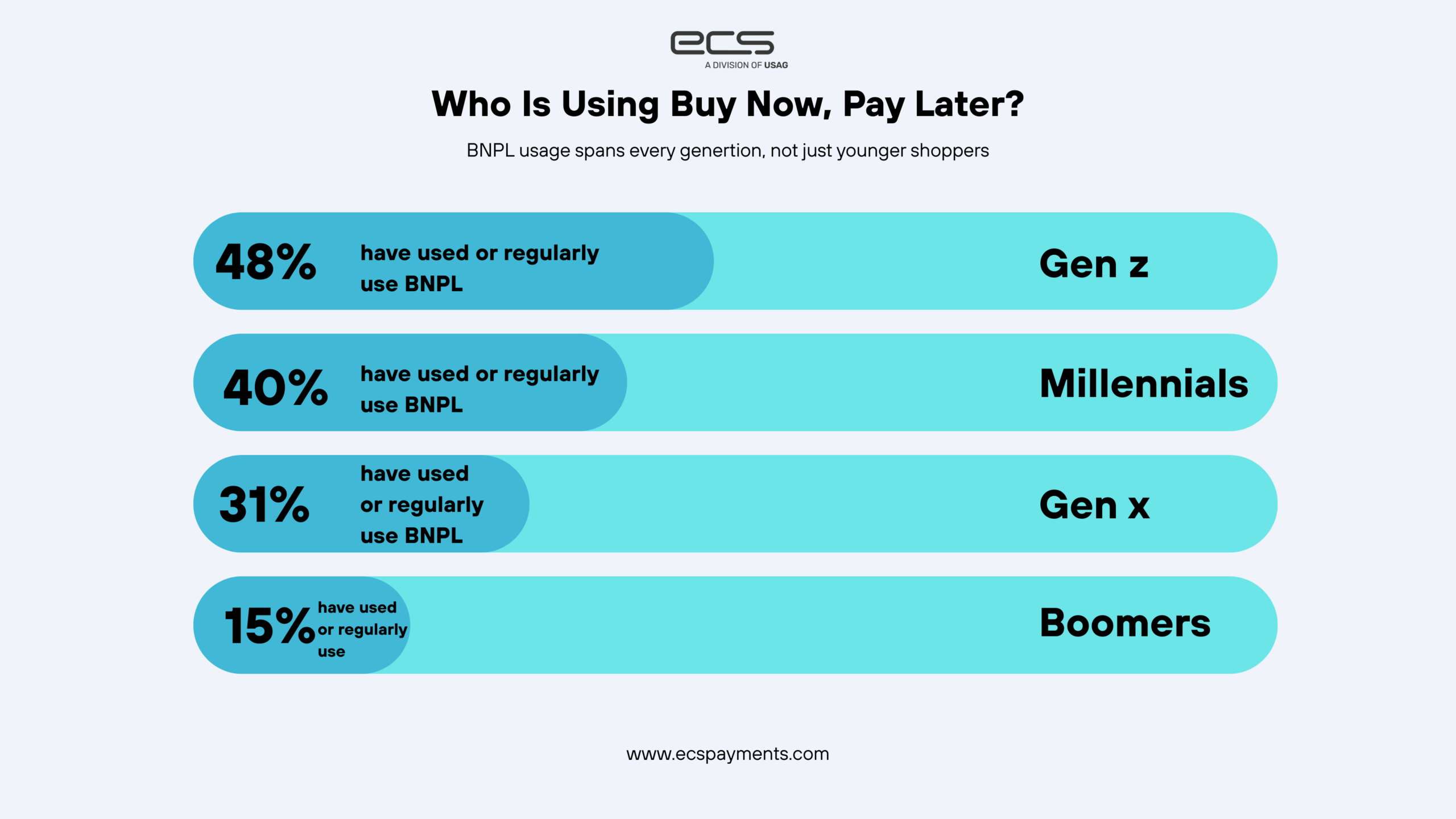

BNPL payments have made significant inroads into consumer behavior. 48% of GenZ shoppers, 40% of millennials, 31% of GenX shoppers, and even 15% of baby boomers have used or regularly used BNPL to make purchases.

BNPL options can help close a sale for customers who are on the fence about cost. Some studies suggest that BNPL options can increase the likelihood of a sale being completed by up to 30% while increasing the average ticket size by as much as 50%.

This makes BNPL very appealing to all types of businesses. Moreover, consumers are not just using BNPL for big-ticket items but even for smaller purchases. In fact, 47% of polled online shoppers said they used BNPL to purchase clothing during the Pandemic. This was the highest category of purchases, beating out appliances (29%), furniture (32%), and even jewelry (12%).

BNPL Disadvantages

There is a drawback to BNPL partnerships for merchants, and that is its costs. While most BNPL schemes are interest-free for the customer, businesses may pay up to 6% or more for the purchase. While the tradeoff of 6% in return for increased sales and ticket sizes may seem worth it, you can do better.

BNPL vs. Loan Management Software

This is where loan management software comes into play once again. For retailers, a payment processor might offer point-of-sale lending or partner with a lender who does. The customer can apply for these loans at the point of sale. Sometimes, these loans do not even involve checking the customer’s credit—just terrorist and fraud watch alerts.

The rates on these “in-house” solutions will be much better than those you can find with Klarna, Affirm, or Afterpay. And more likely than not, the software will provide you with many of the bells and whistles we have discussed before (AI, analytics, and automation, to name a few).

Loan Servicing Software is Secure

Most loan servicing software options for small to midsize businesses will be cloud-based software solutions. This means your business does not need to store any data or customer information “on-site.”

The software company itself stores this information. Subsequently, the software provider is responsible for adhering to data security standards. This is particularly relevant for small and midsize businesses using loan software for point-of-sale loans.

That’s because these types of loans involve collecting customer financial information for recurring payments. Storing customer financial information is subject to strict requirements from the card networks (Visa and Mastercard in particular), which comprises the Payment Card Industry Data Security Standards (PCI DSS).

Larger companies and financial institutions are equipped to have their own in-house teams for storing and protecting customer financial information. But this is cost-prohibitive for most small to midsize businesses or even lenders who are selling repackaged loans.

Once again, loan management software saves the day. Whether it’s a BNPL loan or some other financial product, customer information can be saved, stored, and protected by the payment processor or loan software, alleviating you of this responsibility.

Loan Management Software Wrap-Up

Loan management software is secure, automated, AI-driven, and scalable. It’s an incredible solution for small to midsize lenders and businesses. Contact us to learn more about how lending software can integrate with your business goals and needs, or fill out the form below.

Frequently Asked Questions About Loan Management Software

What is Loan Management Software?

Loan Management Software is a system that enables lenders and even retailers to offer and manage consumer loans in a streamlined process. The software replaces previously paper-driven, human-performed manual tasks.

What tasks can Loan Management Systems automate in the lending process?

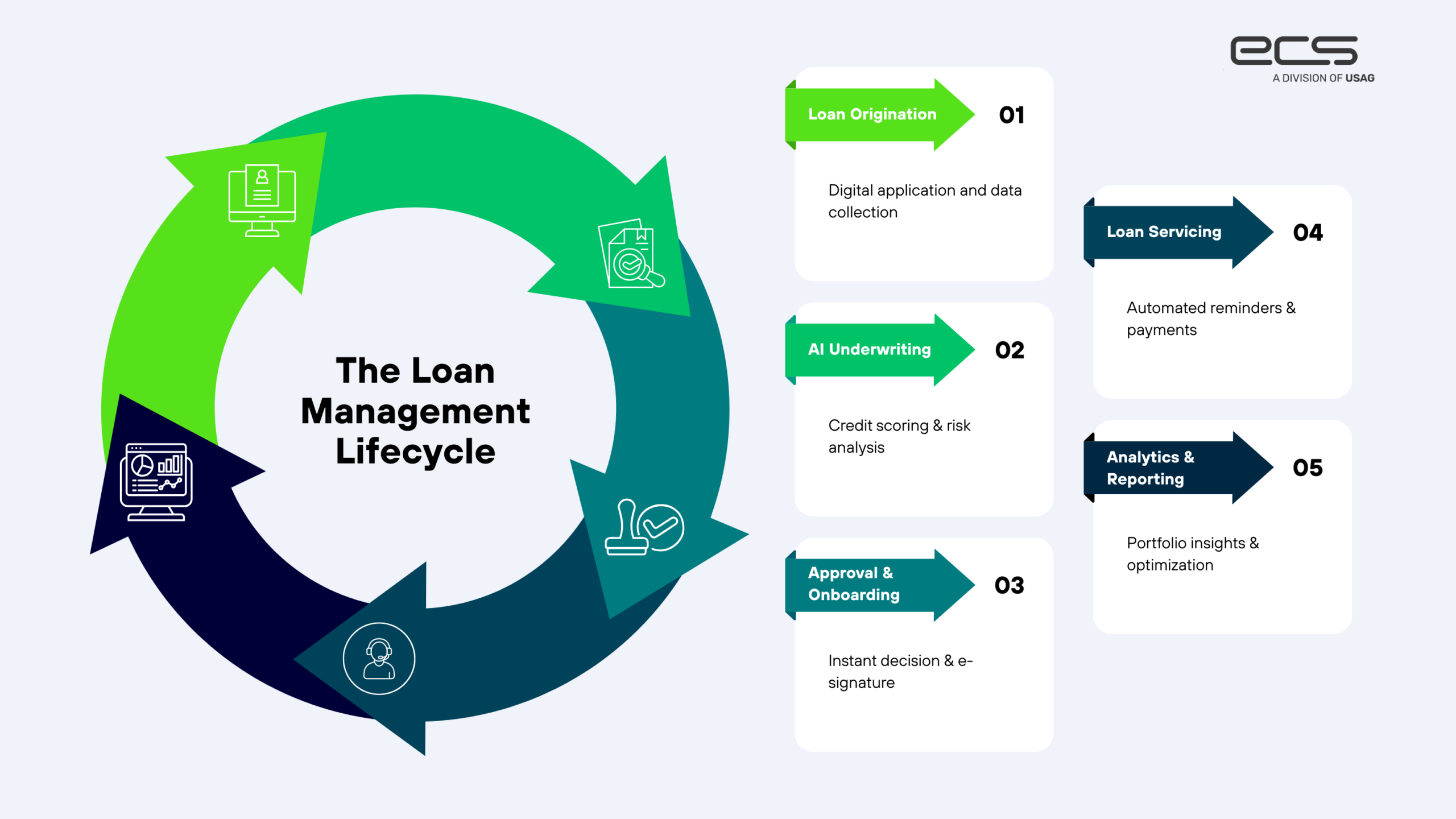

Loan Management Systems automate tasks throughout the entire lifecycle of the loan, such as data collection, document verification, application status updates, credit scoring, instant decisions, onboarding processes, payment reminders, repayment scheduling, data reporting and analytics, and compliance management.

How can Loan Management Software benefit my business?

Loan Management Software automates previously manual and laborious tasks and improves accessibility, a key factor for customer satisfaction. With payment reminders and less manual effort, your business will generate higher profits using the right software.

How does Artificial Intelligence benefit Loan Management Software?

Artificial Intelligence is key in automating Loan Management Software tasks such as expediting credit decisions, analyzing data and credit risk, increasing loan origination and servicing efficiency, and reducing financial losses.