A nonprofit can spend months planning a campaign, crafting messaging, recruiting volunteers, and building donor relationships. Then a percentage of every donation quietly disappears into processing costs. Most organizations pay attention to fundraising revenue. Fewer spend enough time looking at how donations actually arrive. That matters because ACH Donations and Credit Card Donations behave very differently once the money starts moving.

One may cost less, another may convert more donors. One can strengthen recurring giving programs, while the other excels when someone wants to donate immediately from a smartphone during a fundraising campaign. For nonprofits trying to maximize every dollar, the conversation isn’t really about payment technology. It’s about how much money reaches the mission.

Understanding the tradeoffs between ACH and credit card payments can help organizations make smarter decisions about nonprofit payment processing and create a better experience for donors at the same time.

What Are ACH Donations?

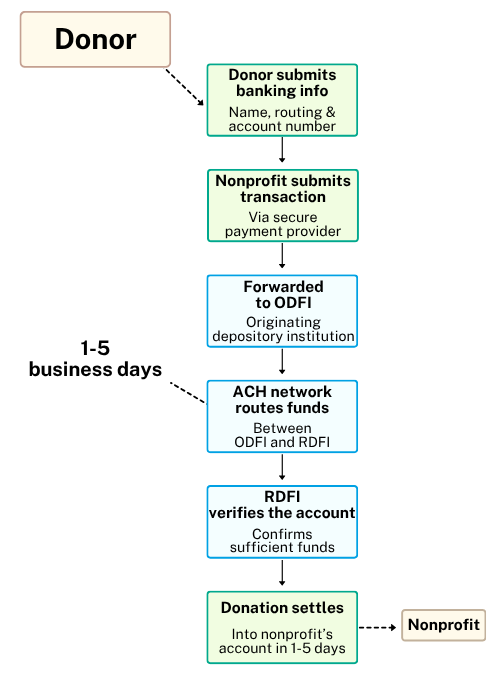

ACH donations move funds directly from a donor’s bank account to the nonprofit’s bank account through the Automated Clearing House network. In 2025, the ACH network processed over 35 billion payments, equalling approximately $93 trillion. These remarkably large numbers show just how embedded ACH transactions are in daily financial activity.

How ACH Donations Work

- A donor enters their personal banking information through a secure digital donation form.

- The nonprofit submits the transaction through its payment provider.

- The payment provider forwards the transaction data to the Originating Depository Financial Institution (ODFI).

- The ACH network routes the funds between the ODFI and the Receiving Depository Financial Institution (RDFI).

- The RDFI verifies the donor’s account has sufficient funds.

- The donation settles into the organization’s account.

Unlike card payments, ACH transactions generally take a bit longer to fully settle. Depending on the banks involved, funding can take anywhere from 1 to 5 business days.

Common Uses for ACH Donations

ACH shines in situations where consistency matters more than speed, such as with monthly giving programs, membership organizations, and recurring donor initiatives. ACH also becomes increasingly attractive as donation amounts increase, because the fee is so small regardless of the size of the transaction, unlike credit card fees, which take a percentage out. Therefore, ACH is best suited for even large one-time donations.

What Are Credit Card Donations?

Credit card donations are fast and require very little explanation to donors. Most people already use cards for everyday purchases, which means the donation experience feels natural.

How Credit Card Donations Work

A donor enters their card information, the payment processor sends an authorization request through the card network, and the issuing bank approves or declines the transaction almost instantly. The donation is complete within seconds, but the settlement of funds will take a day or so as the processor works behind the scenes.

ACH Donations vs Credit Card Donations: Key Differences

Transaction Costs

ACH transactions use a far lower-cost flat-fee pricing structure compared to percentage-based card fees. When donation volume grows, those differences become meaningful. A few percentage points may not seem important on a $25 donation. They become much more noticeable on a $5,000 gift.

Donor Convenience

Convenience is a very powerful force, and credit cards win by a long shot in this category. Most people know their card number, have it saved in browsers and mobile wallets, or have it easily accessible.

Retrieving bank account and routing information, however, requires more effort. Any extra work on the donor’s end can negatively impact conversion rates, particularly for first-time donors who aren’t already set up on recurring payments.

Processing Speed

Card authorizations happen almost instantly. ACH transfers generally require additional settlement time and a few extra days to have access to the funds. Organizations running urgent campaigns may appreciate the immediate feedback that the cards provide.

If someone feels motivated to donate after watching a video, attending an event, or reading a social media post, speed matters. Complicated payment experiences kill momentum, and surprisingly, altruism. Credit cards are also appealing in that users can earn rewards points, travel miles, or cashback benefits.

Donation Limits

ACH is the safer choice for large gifts. Cards can have tighter controls, such as spending limits and fraud controls that create unnecessary obstacles for significant donation sizes.

Recurring Giving Performance

Here’s a reality that many nonprofits learn the hard way. People replace credit cards constantly. Cards expire. Fraud triggers replacements. Account numbers change.

Bank accounts tend to remain stable much longer. That stability often results in fewer failed recurring transactions and fewer awkward emails asking donors to update payment information.

Why ACH Donations Are Growing Among Nonprofits

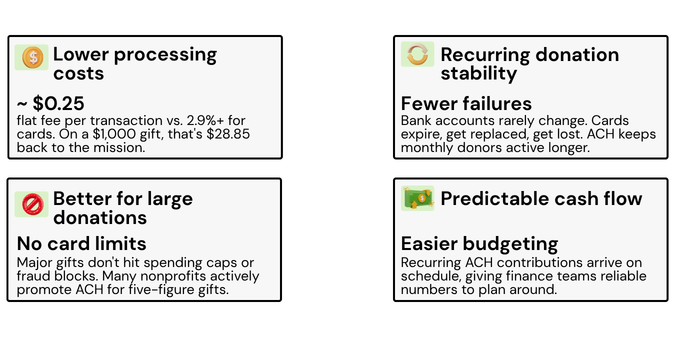

Lower Processing Costs

Fundraising leaders eventually notice a simple fact. Saving money on processing is effectively the same as raising additional money. If an organization processes hundreds of thousands of dollars annually through recurring donations, lower ACH costs can translate into substantial savings over time.

Improved Recurring Donation Stability

Monthly giving programs live and die by retention. Every failed payment becomes an opportunity for donor attrition. Beyond insufficient funds, card transactions can fail due to expiration dates and card number changes for replaced cards. ACH reduces the risk of failed transactions because bank account information rarely changes.

Better Support for Large Donations

Major donors are often concerned with the impact of their contributions. When a significant gift reaches the organization with lower processing fees, everyone benefits. Many nonprofits actively promote ACH payments for major donations for this reason.

Predictable Cash Flow

Recurring ACH contributions create consistency. Consistency makes budgeting easier. And every nonprofit finance director reading this already knows how valuable that can be.

–

Because ACH excels in lower costs and improved recurring donation stability, they make the most sense with:

- Monthly Giving Programs

- Major Gift Campaigns

- Membership-Based Organizations

- Planned Giving and Sustainer Programs

Why Credit Card Donations Remain Popular

Fast Donation Experience

The easier it is to donate, the more likely someone is to do it. Credit cards help reduce any hesitation.

Mobile-Friendly Giving

Social media has been a major platform for modern fundraising campaigns. According to Federal Reserve payment data, card payments continue to dominate consumer payment activity in the United States. When donors encounter a fundraising appeal on their mobile devices, cards often provide the quickest path to completion.

Impulse Giving Opportunities

Events, emergency appeals, and social campaigns thrive on speed. A donor who can complete a contribution in thirty seconds with their card is more likely to follow through than one who has to take extra steps with an ACH transaction.

Donor Preference

Cards offer familiarity, rewards programs, and easy access. Because this is a majority preference, credit card donations are imperative to keep gift streams flowing.

–

Because credit card transactions excel in speed and convenience, they make the most sense with:

- Event Fundraising

- Online Giving Campaigns

- Social Media and Mobile Fundraising

- First-Time Donors

Cost Comparison: ACH vs Credit Card Donations

Understanding ACH Processing Costs

ACH pricing frequently uses one of two models:

Flat-Fee Model: You pay a set amount (usually between $0.20 and $1.50) for each transaction, regardless of the size.

Percentage-Based Model: You pay a small percentage of the total transaction amount (typically between 0.5% and 1.5%). There are many cases where this percentage has a cap. You may pay a 1% fee, but the fee stops at a maximum dollar amount regardless of the payment size (e.g., capped at $10).

Costs will vary by provider, but ACH remains one of the most economical electronic payment methods available.

Understanding Credit Card Processing Costs

Card processing costs include interchange fees, assessment fees, and processor markups. Your pricing structure could be based on true interchange, a flat rate, or tiered pricing. The structure is more complex, and costs often rise alongside donation size because each pricing structure is a percentage-based one.

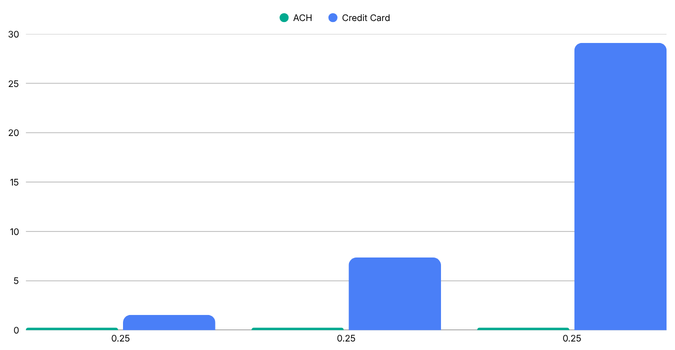

Real-World Example:

Let’s assume:

- ACH fee = $0.25

- Credit card fee = 2.9% + $0.10

$50 donation:

- ACH: $0.25

- Card: $1.55

$250 donation:

- ACH: $0.25

- Card: $7.35

$1,000 donation:

- ACH: $0.25

- Card: $29.10

The larger the donation, the more dramatic the difference in cost becomes. It doesn’t necessarily mean cards are bad. But nonprofits should understand where each payment method creates the most value, whether that’s convenience, creating more donations in an urgent crisis, or smaller fees for larger or recurring payments over time.

Why Offering Both ACH and Credit Card Donations Is the Best Strategy

The play here is pretty simple: use credit cards to get people in the door, and use ACH to keep them there.

Think of credit cards as your frictionless hook. If someone wants to give $25 on their phone during a live event, they aren’t going to dig out their checkbook or look up their routing number; they want to tap a button and be done. But for your heavy hitters or your monthly supporters, you want them on ACH. It stops you from burning money on swipe fees, and you don’t have to worry about their cards expiring next year.

How ECS Payments Helps Nonprofits Accept Donations Efficiently

ACH Payment Solutions

ECS Payments helps nonprofits support both one-time and recurring ACH donations through secure and cost-effective payment workflows.

Credit Card Processing

Organizations can securely accept donations online, in person, and through mobile fundraising initiatives while maintaining a smooth donor experience.

Integrated Donation Management

Managing multiple payment methods becomes much easier when reporting, processing, and payment workflows work together instead of existing in separate systems.

Transparent Pricing

Nonprofits should understand exactly what they’re paying. ECS Payments focuses on transparent pricing structures that help organizations evaluate costs and make informed decisions as fundraising programs grow.

Final Thoughts

So, which one wins? The answer is: both.

ACH wins on low fees and long-term retention. Credit cards win on sheer convenience and quick sign-ups. The most successful non-profits use these two methods together to give donors flexibility.

At ECS Payments, we help non-profits optimize their processing so you can cut down on overhead and put more money directly toward your cause.