You are likely leaving a small fortune on the table every single time a customer swipes their card or clicks the checkout button, and ignore that data. Most business owners view a transaction as the end of a pursuit, the final goal where money changes hands, and the deal is done. In reality, that transaction is the loudest and most honest conversation a customer will ever have with your brand. While marketing surveys are often ignored and social media likes are fickle, payment data provides a cold, hard look at exactly what your customers value and how they intend to behave in the future. Ignoring this information is like trying to navigate a ship in the dark while the GPS is sitting right in front of you.

At ECS Payments, we see merchants struggle to balance aggressive growth with strict security protocols every day. It is easy to get overwhelmed by the sheer volume of numbers moving through your gateway. But we’ve got some exciting news. Every authorization request and settled batch contains the blueprint for your next big win. So, it’s important that you handle this data with extreme care.

Using your data to grow your business effectively is a huge opportunity. But balancing it with adhering to the Payment Card Industry Data Security Standard (PCI DSS) and various privacy laws is imperative. It is the foundation of the trust you build with your audience. When you treat payment data as a protected asset rather than just a byproduct of a sale, you unlock the ability to predict churn before it happens and reward your best shoppers before they look elsewhere.

The Untapped Value of Transaction Data

When a customer chooses to spend their hard-earned money with you, they are giving you a vote of confidence that includes details about their lifestyle, their financial comfort, and their level of commitment to your products. Many merchants make the mistake of looking only at their monthly statements to see the total volume and processing fees. While those are important for your bottom line, the real magic happens when you look beneath the surface at the patterns.

The challenge is that this information is sensitive. As a business owner, you have a massive responsibility to ensure that any analysis you perform remains within safe bounds. Understanding the difference between personally identifiable information (PII) and anonymized behavioral data is important. For example, you don’t need to know a customer’s social security number or their full address to understand their buying habits. By focusing on the “what” and “when” rather than the “who” in a private sense, you can stay compliant with global privacy regulations while still gaining the upper hand in your market.

What Payment Data Can Tell You About Your Customers

When you dive into the specifics of your payment data, you start to see metrics that directly influence your strategy. One of the most telling factors is frequency. How often do you see a specific repeat card? A customer who visits once a week is fundamentally different from one who visits once a quarter. The same generic marketing for both of these customers is a huge loss. By identifying the difference between repeat and high-frequency users, you can tailor your marketing opportunities.

Next, let’s look at ticket size and card type. Customers using premium or corporate cards may have different expectations for service or delivery speed compared to those using standard credit or debit cards. Then there is the timing of transactions. Do your customers tend to shop more on Friday afternoons or Tuesday mornings? Reacting to these findings helps you to staff your customer support or your physical storefront more effectively.

According to a study reported by Forbes, data-driven organizations are 23 times more likely to acquire customers and six times as likely to be profitable year over year compared to those that are not. Using these metrics helps you segment your audience safely. You aren’t looking at private details; you are looking at trends that allow you to serve the customer better.

Connecting Payments to Loyalty

Loyalty is often misunderstood as a simple punch card system where the tenth coffee is free. In the digital age, true loyalty is about relevance. When you use your payment data to inform your rewards programs, you create an experience that feels personal. If your data shows that a segment of your customers consistently buys a specific type of software or a particular brand of apparel, your loyalty outreach should reflect that. Offering a discount on a product they have never expressed interest in is a waste of your resources and their time.

Consider the subscription services industry. This is where Customer Lifetime Value is truly won or lost. By analyzing transaction trends, you can see when a customer’s spending starts to dip or when their payment method is nearing its expiration date. A proactive outreach to update a card before a renewal fails is a form of loyalty service. It shows the customer that you are paying attention and that you value their continued presence. This type of engagement, powered by the technical details of the payment process, keeps the relationship alive without the customer ever experiencing a service interruption.

Using Decline and Approval Data for Retention

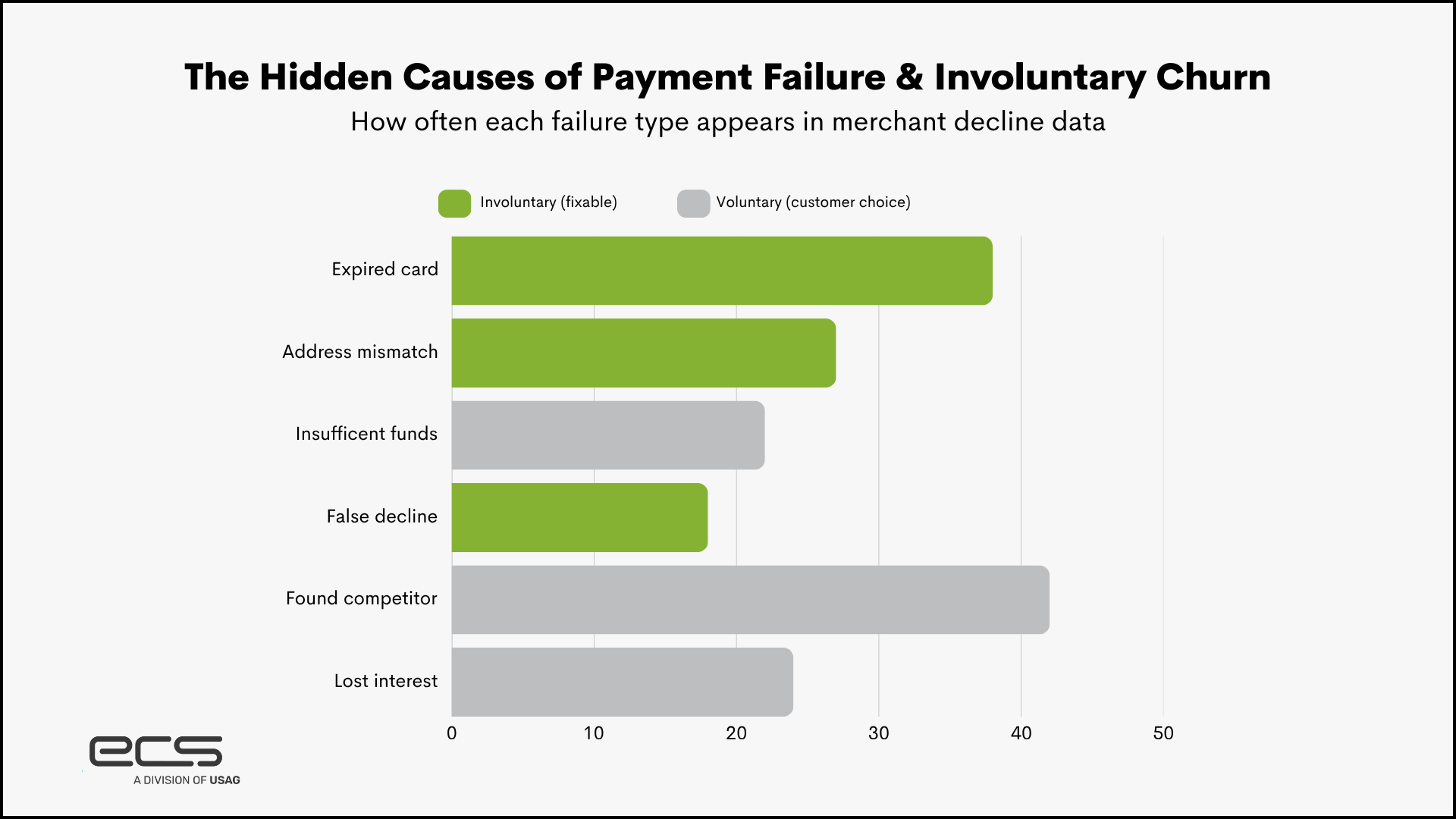

One of the most overlooked aspects of retention is the technical success behind the transaction itself. Customer churn isn’t just the byproduct of finding a different product or service they desire more, one that is more convenient or cost-effective. You also need to look at “involuntary churn.” It’s a silent killer for many businesses. This happens when a legitimate customer wants to pay you, but the transaction fails due to a technical error, an expired card, or a false decline from the issuing bank. If you aren’t monitoring your approval and decline data, you are losing customers who actually want to stay.

Identifying billing-related drop-offs is the first step toward fixing them. If you notice a high rate of declines on a specific day of the month or with a specific card type, it may indicate a need for better routing or a more sophisticated retry logic. According to the U.S. Small Business Administration, retaining an existing customer is far cheaper than acquiring a new one. It can cost five to twenty-five times less, depending on the industry.

At ECS Payments, we provide tools that allow merchants to monitor these authorization success rates in real time. We’ve designed our systems to give you a clear view of why payments might be failing so you can take action. Instead of wondering why a regular customer suddenly disappeared, you can look at the data and realize their card was declined due to a simple address mismatch. Fixing these small technical hurdles is one of the fastest ways to improve your retention rates and ensure your revenue remains predictable.

The Practical Framework: Collect, Analyze, Act, Measure

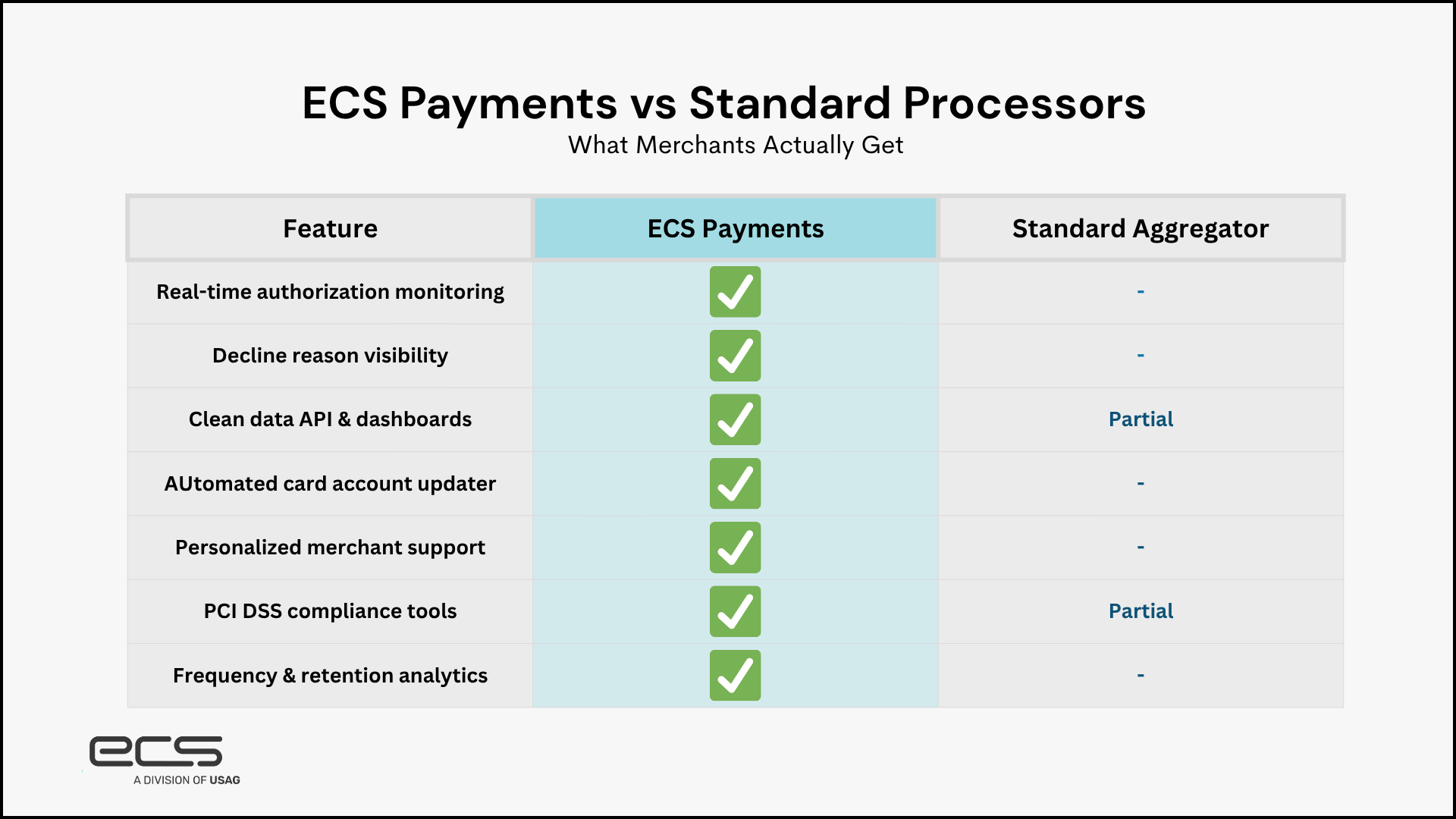

To make this work for your business, you need a repeatable framework. You cannot just look at your data once a year and expect results. The process begins with collection. You have to make sure your gateway pulls the right details without brushing over any PCI compliance regulations. This is exactly why picking a processor is a major strategic move for your business. You need a partner that hands over clean, easy-to-read data through solid APIs and dashboards. Ones that actually make sense when you look at them.

Once you have the data, the analysis phase involves looking for the trends we discussed, such as frequency and timing. The third step is to act. This might mean launching a targeted email campaign for customers who haven’t shopped in thirty days or implementing an automated “account updater” service to handle expired cards. Finally, you must measure the results. Did your Customer Lifetime Value increase after you implemented these changes? By closing the loop, you turn your payment processing from a cost center into a powerful engine for growth.

The Federal Trade Commission emphasizes the importance of transparency in how consumer data is handled. Maintaining clear policies on how you use transaction information to improve service is key to keeping consumer trust.

ECS Payments: Your Partner in Data-Driven Growth

While many companies can move money from point A to point B, ECS Payments stands apart as a dedicated advocate for merchants. A monthly bill for processing fees is no fun, especially when all it does is drain your revenue and offer no support to your growth. The right partner will help you interpret your payment data to build a stronger, more resilient business.

We offer the kind of personalized support that large, faceless aggregators simply cannot match. Our platform is built for the business owner who wants to be in control. We offer a level of transparency and technical sophistication that serves as a superior alternative to standard processors. When you work with us, you are getting a suite of tools designed to help you understand your audience. We focus on high-level security so that you can focus on the insights that drive loyalty and long-term success.

Turning Compliance Into Competitive Advantage

Consumers are increasingly wary of how their information is used. Because of this, transparency is your greatest asset. Using payment data responsibly not only is lawful, but it also helps to improve the customer experience and build a competitive advantage. People stay with businesses that make their lives easier and feel personal. By leveraging the signals already present in your transaction flow, you can deliver that level of service without ever compromising privacy.

Responsible data use builds a bridge between you and your customers. It allows you to move away from guesswork and toward a strategy rooted in reality. Remember, the most valuable information you own is already flowing through your systems. It is time to stop letting it go to waste and start using it to power your growth.