Some of the biggest leaks in your business revenue aren’t obvious. They don’t come from slow seasons or high operating costs. They come from something smaller and sneakier: failed payment transactions. Somewhere between clicking “complete purchase” and the bank giving the green light, the transaction fell apart. What most merchants don’t realize is that a single decline doesn’t always mean a lost sale… but only if you understand the difference between soft declines vs. hard declines.

For business owners, understanding “Soft Declines vs. Hard Declines” is the key to recovering revenue, keeping customers loyal, and avoiding the silent leaks that drain profits month after month.

Online Shopping Cart Abandonment is a Huge Problem

Every abandoned transaction takes a toll. U.S. retailers lose around $18 billion every year because customers leave their carts behind. It is not always about shoppers changing their minds or getting distracted. A large part of the problem comes from failed payment attempts.

These are sales that could have been saved if merchants understood what went wrong and how to fix it. That is why knowing the difference between soft declines and hard declines is so important for business owners.

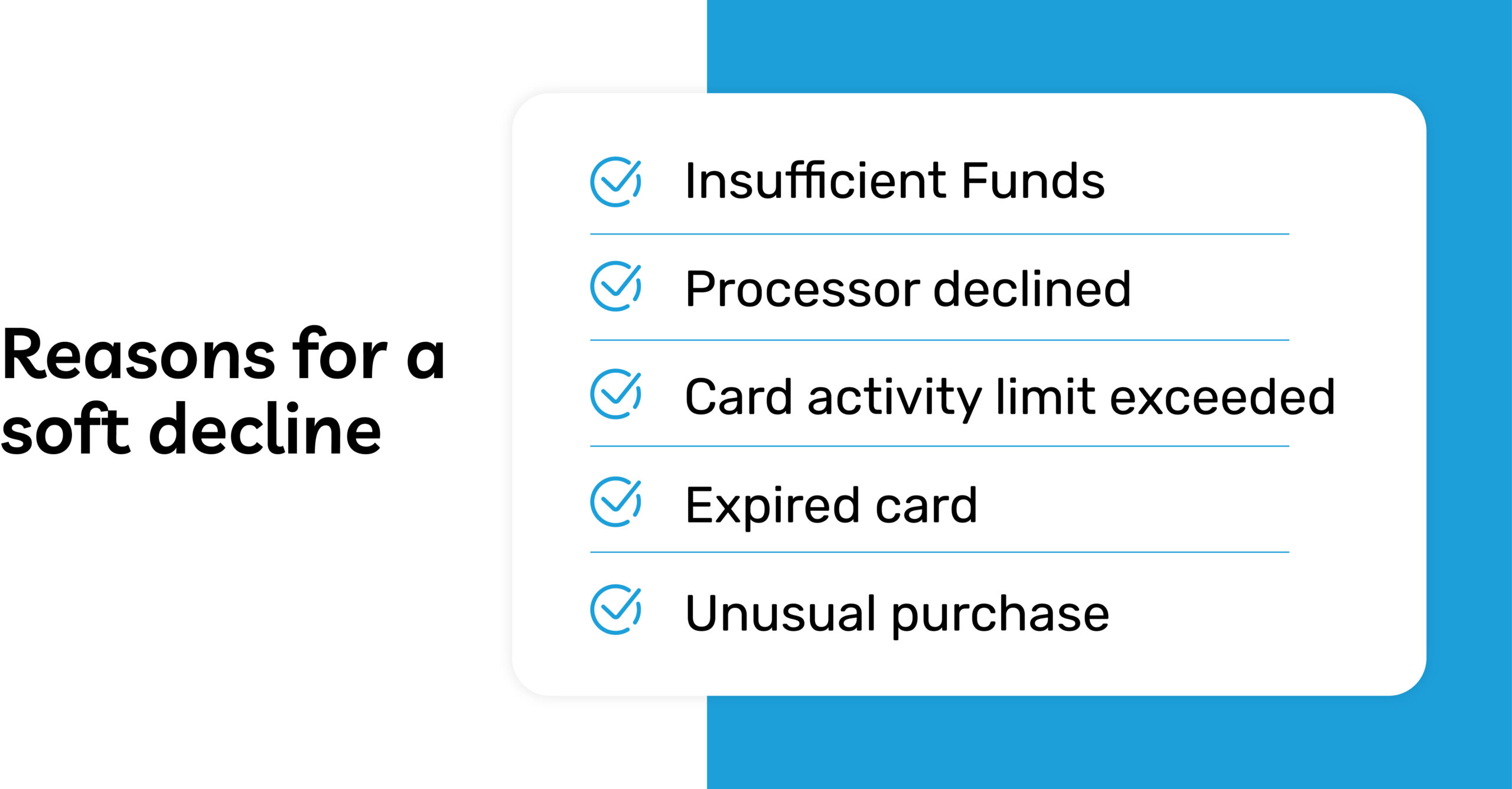

What Is a Soft Decline?

A soft decline is a temporary hiccup in the payment process. It doesn’t always mean the customer lacks funds or that the card is invalid. Often, it’s a situation where the card issuer is essentially saying, “Try again later.”

Some of the most common causes of soft declines include:

- Insufficient funds: The cardholder’s balance may be low at the time of the transaction, but funds could be available later.

- Temporary fraud checks: Banks sometimes flag transactions for review, especially if the purchase seems unusual or involves a high amount.

- Processor timeouts: Technical glitches between the merchant, processor, and bank can interrupt an otherwise valid transaction.

- Exceeded credit limits: If the cardholder is close to their limit, the transaction might be denied until a payment is made.

The key point here is that soft declines can often be retried. Sometimes a second attempt goes through successfully after a few minutes or hours. Merchants who understand this distinction can recover a significant percentage of sales simply by setting up proper retry logic.

What Is a Hard Decline?

Hard declines are a different story altogether. When a transaction is hit with a hard decline, the issuing bank has made it clear that it will not approve the payment under any circumstances with the current card details.

Some of the most frequent causes include:

- Invalid or expired card numbers: Cards expire or get replaced, and old details won’t work.

- Closed accounts: If the account linked to the card has been closed, the transaction will fail.

- Stolen cards reported: When a cardholder reports theft, the bank blocks all transactions to prevent fraud.

- Merchant blocked by issuer: Sometimes the bank itself flags the merchant for reasons related to risk or compliance.

Unlike soft declines, hard declines cannot be retried. If you attempt the same transaction again without updated information, it will fail every time. The only way forward is to ask the customer for a new form of payment.

The Key Differences Between Soft and Hard Declines

To put it plainly, soft declines leave the door open. Hard declines slam it shut.

With a soft decline, there is potential for the transaction to succeed if you retry it at the right time or give the customer a chance to fix the issue. A hard decline, on the other hand, tells you that the problem is permanent until the customer provides a different payment method.

For merchants, understanding this difference shapes your response. It helps you avoid unnecessary retries when the bank has already made a final decision while also preventing lost sales when a simple retry might have saved the transaction.

Why Payment Declines Matter More Than You Think

Some merchants shrug off payment declines as a cost of doing business. But the impact can be bigger than many realize.

Every declined transaction is a potential lost sale. And customers who experience multiple declines often abandon their cart altogether, sometimes for good. The Baymard Institute reports that over 70% of online shoppers abandon their carts before they complete their purchase. Beyond distractions and customers changing their minds, payment issues do play a major factor in those numbers.

Extending past the lost sale, there’s the ripple effect. A customer who runs into repeated payment trouble may assume your checkout system is the problem, even when it isn’t. That can damage your reputation and hurt repeat business.

Handling Soft Declines the Right Way

When a soft decline occurs, the goal is to save the sale without frustrating the customer. The best approach is to have systems in place that automatically retry declined transactions at carefully timed intervals.

It also helps to give customers multiple payment options. Offering ACH payments, or Apple, or Google Pay options, for example, can provide a backup method if a card transaction fails.

Finally, communication matters. Not only the efficiency and swiftness of your communication with the customer, but also the tone. A friendly, personalized message asking the customer to confirm card details or try another method can keep the experience positive and prevent abandoned transactions.

Handling Hard Declines with Care

A hard decline indicates a critical problem. This could be an invalid or expired card number or a fraudulent transaction attempt. Since retries with the same details won’t work, you have to ask the customer for a new form of payment.

When communicating with your customers about a hard decline, it’s important to be polite and helpful. Avoid language that might imply fault on the customer. Provide clear, concise instructions on how to proceed. Offering multiple alternative payment options (e.g., different credit cards, digital wallets, ACH bank transfers) can also help facilitate a successful transaction.

If the card is declined due to fraud, merchants must be even more aware. If the customer truly wants to complete the purchase, they will try another payment method, but if they’re just trying to use stolen card information, they will not attempt to complete the sale.

Merchants should also keep detailed records of declined transactions. This helps prevent fraud, especially when the decline was due to a reported stolen card. Using fraud prevention tools built into your payment processing system adds another layer of protection.

How ECS Payments Helps Merchants Reduce Declines

At ECS Payments, we know that every lost sale matters. That’s why our payment gateway comes equipped with advanced fraud detection tools designed to catch suspicious transactions before they become a problem. Behind the technology, our in-house risk team monitors transactions closely, giving merchants an added layer of protection and confidence.

We also make it easy for businesses to accept a wide range of payment methods. Whether it’s credit or debit cards, ACH payments, or digital wallet transactions, we support multiple options at checkout. Options reduce decline rates and keep the payment process smooth for everyone involved.

Conclusion: Turning Declines Into Opportunities

The difference between soft declines vs. hard declines comes down to one word: potential. Soft declines may be temporary setbacks that can often be resolved, while hard declines require a completely new approach.

Merchants who understand this difference save more sales, keep customers happy, and protect their bottom line.

At ECS Payments, we help businesses do exactly that. With smarter technology, industry expertise, and a commitment to keeping transactions seamless, we turn payment declines from a point of frustration into an opportunity for improvement.

If you’re ready to improve approval rates, reduce customer frustration, and keep revenue flowing, ECS Payments is here to help.